This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Moreover, when Gen AI proposes enhancements to a product, risk rule, or customer service scenario, Way4 can implement these requests instantly. Instead of hard coding, Gen AI can configure new payment offerings using flexible parameters. Read more about OpenWay’s Gen AI digital payments usecases here.

When those rules were introduced, the intended aim was to drive competition in the retail banking market and make it easier for consumers to switch accounts. Instead, what the UK’s Open Banking rules have unleashed is a whole range of innovation from third-party providers tapping into customer banking data that they have consented to share.

In this article, we cover the developments between Agentic AI in fintech and possible usecases, giving a glimpse into how financial services could look like in the near future. What is Agentic AI?

Each ID-Pal Once profile is built from already-verified identity data, but critically, this information is re-validated against an organisation’s own risk rules, without requiring the end user to repeat the submission process. This ensures ongoing compliance while minimising user friction.

The report outlines several potential usecases for spendable benefits cards, such as use in employee-engagement platforms, reward and recognition platforms, traditional HR platforms and new employee-centric super apps. Employees tap their way to much more personalised and relevant benefits.

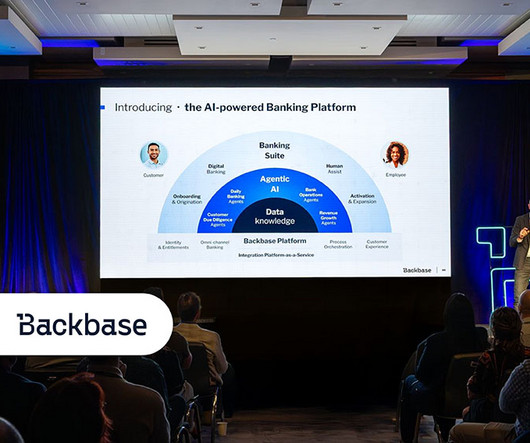

To help banks implement the platform, Backbase also introduced the AI Factory, a delivery model that embeds its experts within client teams to develop usecases and bridge the industrys AI talent gap. Its not a wait-and-see – its here, now, and its rewriting the rules of the industry. AI waits for no bank.

The security of such payments rests entirely on the devices, hence the use of secure elements in the experiment. The difficulties lie in the assumption that, however secure they may be, one cannot rule out a breach of secure elements in the future. This distinction has real-world implications.

This enables rapid scaling of new payment usecases, without duplicating risk exposure. This enables payment systems to manage both on-chain and off-chain identity events, supporting high-assurance usecases such as digital ID-linked payments or KYC-compliant wallet onboarding.

At EBizCharge, we help businesses implement surcharge programs that reduce costs without violating card network rules or state laws. Common UseCases: Frequently used in service-based industries where margins are thin. Used by merchants who want to keep prices competitive without absorbing card processing costs.

Bahrain, the first country in the Middle East to introduce open banking, launched its open banking framework (OBF) in October 2020, following the initial set of rules released in December 2018. The new amendments are set to bring legal entities in line with the existing open banking framework.

Examples of Geolocation Technology Used for Fraud Prevention Here are a few common usecases for geolocation technology as a fraud prevention asset: IP Geolocation IP geolocation uses the IP address of a device to determine its location.

Popular usecases include: Specialised calculations: Oradian’s specialised calculations allow institutions to set product-specific rules, such as automatically applying late fees when accounts exceed a set threshold, which streamlines adaptation to new market conditions without manual recalculations.

The number of adults using Open Banking in the UK represents around 10% of the adult population. The adoption of account data services has lagged behind Open Banking payments, whilst the number of Open Banking usecases is limited and it has not yet entered daily or weekly usage for most consumers and businesses.

UseCases and Impact U.S. banks are applying AI in a range of usecases. On the risk and operations side, common uses include fraud detection, anti-money-laundering pattern detection, credit risk scoring and trading optimization. UseCases and Early Benefits UK banks mirror global trends in AI usecases.

A convenience fee is charged for using an alternative payment method, like an online portal. Everyday usecases include manufacturers invoicing large credit card payments, SaaS companies billing subscriptions, and wholesalers offering card payments with clear surcharge terms. For B2B transactions, disclosure is crucial.

The Monetary Authority of Singapore (MAS) keeps the market secure through rules that protect investors while encouraging growth. While B itcoin, introduced in 2009, is the most well-known cryptocurrency, there are thousands of cryptocurrencies with various usecases today. What are Cryptocurrency Exchanges?

What started as simple, rule-based programs has evolved into smart conversational agents powered by advanced technologies. Todays chatbots use natural language processing (NLP) and machine learning (ML) to engage in human-like conversations and handle complex queries seamlessly. Key Features Pre-built workflows for fintech usecases.

Using the sandbox and Mastercards latest A2A payments technology, banks will be able to test new flows, including retail and digital assets, across person to person, person to merchant, and business to business usecases. We use cookies to help us to deliver our services. Please read our Privacy Policy.

A convenience fee is charged for using an alternative payment method, like an online portal. Everyday usecases include manufacturers invoicing large credit card payments, SaaS companies billing subscriptions, and wholesalers offering card payments with clear surcharge terms. For B2B transactions, disclosure is crucial.

From here, the agent transforms such data using natural language inputs. Once the data is processed, the agent applies relevant accounting assumptions based on historical patterns and your departments specific rules to contextualize the content. Now that you understand what agents are, its time to look at their usecases.

To meet this demand, SEON’s AML suite delivers granular, real-time monitoring alerts that reduce false positives and improve detection accuracy across both fraud and AML usecases. “We already use SEON as a key part of how we manage fraud risk at Casumo ,” said Sebastian Brant , director of CEX at online casino Casumo.

Voices from the industry Virtual IBAN regulations are evolving as regulators tighten AML compliance, data protection, and cross-border payment rules. Data shows that vIBANs are primarily used by large financial firms, with minimal adoption among small businesses and individual consumers.

Each type of fee has its own usecases and legal implications. Surcharges are specifically tied to credit card use and are usually a fixed percentage. Federal Overview Surcharging is legal at the federal level in the United States but businesses must follow rules set by credit card networks like Visa and Mastercard.

Compliance and Legality Before you roll out a surcharge program, you need to understand the rules that govern how it must be implemented. You need to check state laws and card network rules. State Laws: Check your state’s rules. You’ll need to verify if your state allows surcharging and comply with credit card network rules.

Fraudsters, using forged or altered information, have long been exploiting traditional address verification methods, such as utility bills or other proof of address documents.In ” The post iDenfy Files Patent for Address Verification Solution That Mixes Physical and Digital Techniques appeared first on The Fintech Times.

The study sheds light on how various factors, including usecases, benefits, and industry challenges, are shaping the future of instant payments. However, enablers also identified strong tailwinds such as usecase-driven approaches and expanding rules and standards, which will help accelerate adoption.

“The European Commission has made commitments offered by Apple legally binding under EU antitrust rules,” the official announcement says. To explicitly acknowledge that HCE developers are not prevented from combining the HCE payment function with other NFC functionalities or usecases.

Together, these new rules will enable Europe to push forward into Open Finance – the next stage of Open Banking. Their impact will be augmented and enhanced by a third set of rules, the Financial Data Access (FIDA) framework. It allowed for the emergence of various usecases and innovative solutions to address customer needs.

Against that backdrop of moving away from paper payments, and toward ubiquitous real-time payments, TCH’s Waterhouse said there’s probably not a usecase “that’s going to tip the scale here.” But he pointed to a usecase that might be a bit under the radar. So that is certainly an aspiration. Interoperability In Focus .

The second phase of sandbox testing went further, exploring more complex usecases, using Swift’s solution to connect and orchestrate transactions across simulated digital trade and tokenised asset and FX networks, alongside CBDCs for payments. More than 750 transactions were carried out over the course of the experiments.

Many of the current rules were designed for an earlier generation of financial services and do not reflect the complexity or speed of todays payments ecosystem. A formal process for reviewing and updating outdated rules could help reduce unnecessary compliance burdens.

In short, the global pandemic has ushered in rising usage — and usecases — for TCH’s RTP ® network, and Whisler doesn’t see that slowing down anytime soon. One such rule currently being internally and externally assessed is the $100,000 daily transfer limit, which she anticipates will be raised. Limits And Fees.

For all practical concerns, they might have their own rules, or worse none at all. Set up an export workflow to Google Drive and define your file renaming rules. Check out Nanonets for similar usecases. Find out how Nanonets' usecases can apply to your product. Nanonets can handle it all.

The report notes that several institutions have already started exploring the use of gen AI in risk management, citing regulatory compliance, financial crime, credit risk, modeling and data analytics, cyber risk and climate risk as emerging usecases. The tech can also draft model documentation and validation reports.

What’s happening: Fintechs leveraging AI are finding that they need to adapt (and quickly) in order to comply with the new rules while continuing to create and develop new, AI-centric products. Where you’ll see it: FinovateEurope is sure to be packed with fresh AI usecases and regulatory guidance.

Nacha’s Smarter Faster Payments conference highlighted the progress that is now being made to expand use-cases and benefits. New fraud monitoring rules require a proactive approach Finally, as expected, real-time fraud prevention remains a key consideration. We use cookies to help us to deliver our services.

She also referenced a broader issue of regulatory inertia: The previous government had plans to revoke the Payment Services Regulations and embed them into FCA rules. For scale-ups like us, weve built regulatory muscle over the yearsour teams understand governance, conduct rules, and operational resilience.

But it can be just as painful, following all the rules and the hundred-page credit agreement so that you don’t get penalized by Goldman for breaking a covenant or two. …I And then staying in compliance and operations won’t require a team of analysts and accountants working on-end to comply with Goldman’s or JP Morgan’s rule set.

Through a robust set of APIs covering payments, accounts, mandates, CRM, cards, loans and open banking usecases, NBO’s platform empowers businesses and developers to streamline operations and drive automation. We use cookies to help us to deliver our services. You may change your preferences at our Cookie Centre.

states (though not all), and there are specific rules governing its disclosure and calculation. While the term ‘customer processing fee’ may be used informally to describe this added charge, the actual method used and how it’s labeled matter both legally and practically. It’s legal in most U.S.

Potential usecases and reality, however, are two different things. The actual use of AI in the banking sector has been quite limited, while older legacy systems have remained prevalent, such as business rules management system (BRMS). To learn more about the emerging usecases of AI in banking, download the report.

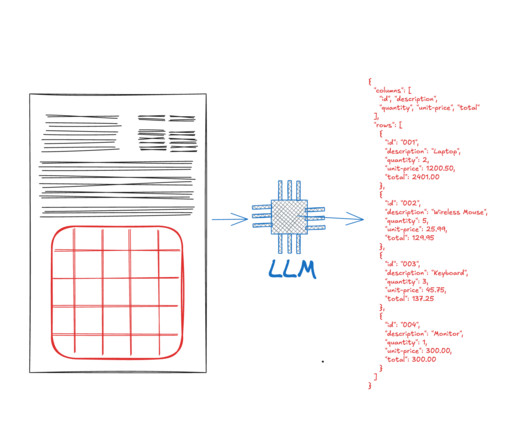

Applications of Table Extraction Table extraction has wide-ranging applications across various industries, here are a few examples of use-cases where converting unstructured tabular data into actionable insights is key: Financial Analysis : Table extraction is used to process financial reports, balance sheets, and income statements.

For every positive usecase, there are multiple ways humans can use the technology for nefarious purposes. This will impact how banks and fintechs use AI for customer interactions, underwriting, and fraud detection. This could benefit both fintechs and banks for support in testing and launching their new AI usecases.

Fraudsters are continuously finding new sophisticated ways of leveraging AI to carry out cyber threats, with traditional fraud prevention methods, which rely on fixed rules and human intervention, being no longer sufficient to detect and mitigate the complex and evolving tactics used by fraudsters.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content