This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

One of the biggest challenges for crypto adoption has been its usecases. For many, it has simply been viewed as a volatile investment, but what if it could be used to make everyday purchases? To that end, Rezolve aims to use Tethers technology to empower businesses and consumers worldwide in a market valued at $30trillion.

Prevalence Encryption is ubiquitous. There are more and more platforms and integrations with different technologies that we’re seeing every day. Soon we may see standards for tokenization in everyday use. Tokens, on the other hand, do not depend on the sensitive data to be created.

Against that backdrop of moving away from paper payments, and toward ubiquitous real-time payments, TCH’s Waterhouse said there’s probably not a usecase “that’s going to tip the scale here.” But he pointed to a usecase that might be a bit under the radar. So that is certainly an aspiration.

“As real-time payments become ubiquitous in Kuwait, consumers have gravitated toward secure, real-time payment methods, reshaping habits around convenience and efficiency while reducing reliance on cash.

You’ve got to unwire the whole enterprise — both its technology stack and its culture.”. But PSCU’s Fagan said making those upgraded experiences truly ubiquitous will be a longer, more-complicated effort. “If The digital solutions have been ubiquitous. That’s a 2.75 to three, because that part is much more complex.

.” To imagine a world where robots do all the physical work, one simply needs to look at the most ambitious and technology-laden factories of today. For example, the Dongguan City, China-based phone part maker Changying Precision Technology Company has created an unmanned factory. So, what does the future of factories hold?

Doubt plagues any disruptive technology. But with federal officials now pressing for faster payments technologies to get off the ground, time is running out for the nay-sayers to be convinced. “There is a lot of talk around usecases and specific benefits for corporate, insurance and other types of disbursements,” he said.

McCarthy said what’s becoming apparent is that for perhaps the first time, technology like artificial intelligence (AI) and sophisticated data modeling are catching up to the problems. And with the technology available today — and innovations already on the table — it’s well past time to start building something much better.

And in retail , our technology powers embedded lending at the point of sale—enabling instant credit decisions and personalized repayment options that drive conversion and loyalty. These usecases all build on AdviceRobo’s core strengths: behavioral data science , explainable AI and api-based scalable infrastructure.

In just a matter of days, the payments industry will see a significant — and ubiquitous — change in the way payments are sent and received. While both Same Day ACH and real-time payment initiatives have unique functionality and innovative usecases serving distinct end-user needs, collectively, these initiatives will give U.S.

Ingo Money exists to make digital push payments just as ubiquitous and a whole lot less friction-filled for consumers and businesses. So we get to apply that same technology stack to authenticate that consumer when a company says to send money to that person,” Edwards told Webster.

In payments, to gain technology, reach and new usecases (and, sometimes, all of the above at once), the debate has always boiled down to “build or buy.” Usecases extend across online marketplaces, gig economy payroll payments , cross-border remittances, loan payouts and insurance disbursements, to name a few.”.

Tokenisation unlocks a plethora of use-cases and benefits, such as helping turn everyday technology, like phones and cars, into commerce devices. Mastercard is bringing together key solutions to reduce threats and make online commerce not only ubiquitous: 1. Consumers will experience faster and safer checkouts.

He said the technology is a “new era in commerce. Apple’s Homepod, Google’s Home and Amazon’s Echo are the most rapid-selling segment of consumer technology since mobile phones, according to eMarketer. As artificial intelligence becomes more and more ubiquitous, Gauthier says the move toward shopping by voice in inevitable.

Though the technologies still haven’t reached a level of mainstream usage or acceptance, that hasn’t slowed down the number of companies and sectors looking to utilize VR/AR to transform customer experiences. Matt Ozvat, head of developer integrations at Vantiv , and Josh Mather, technology evangelist at Vantiv, whose Vantiv O.N.E.

But in the decade since bitcoin’s debut, technologies have evolved in the payments ecosystem that are helping set the stage for cryptos to become more widely adopted. He pointed to the JPM Coin as a key advance in how cryptos might be used to reduce friction inherent in the financial services ecosystem. The Difference A Decade Makes .

This lack of consumer demand needs to be addressed if open banking technology can reach its full potential. “To accelerate increased adoption of open banking, there needs to be a compelling user experience and expansion of usecases. For that vision to become a reality, open banking payments need to be truly ubiquitous.

As he told PYMNTS, “5G is going to stimulate usecases that require not just speed but low latency, and which are data-driven.”. And as he said, 5G is largely being built atop 4G technology as carriers have been “densifying” their LTE networks, which helps save on costs.

That’s the talk track now from the Fed , which a week ago today announced its plans to build and operate a new set of real-time rails, using accelerated access to employer paychecks as its launch usecase. Ironically, perhaps, the ACH network’s first direct deposit usecase was the U.S.

Results from the survey indicated that bill pay ranked as one of the top three usecases for both FIs and businesses with nearly 60% of respondents indicating it as a top priority. Given these findings, the FPC and Glenbrook positioned bill pay as the subject for a second round of qualitative research.

Likewise, Circle will provide Binance with the necessary technology, liquidity and other tools for Binance users to benefit from the trust and innovation that Circle has built for USDC. USDC has been recognised as one of the most powerful utilities for money on the internet, and it is only set to grow as it is further adopted worldwide.

It has pulled ahead of its EU neighbors in developing real-time payments technology and in recruiting banks to adopt it. It has clarified the banking processes, but RTP is hardly ubiquitous within Italy, much less across the Eurozone. To get a sense of the present state — and future — of instant payments, look to Italy.

We believe that bitcoin has the potential to be a more ubiquitous currency in the future,” said Amrita Ahuja, chief financial officer of Square. This speaks more to an investment strategy (asset diversification, for example), we contend, than as a pivot toward using cryptos in the service of commerce.

The vacuum created by the absence of a ubiquitous real-time or instant payments scheme has been filled in by private sector innovation, perhaps readily evident in offerings like Zelle and Venmo. The move to instant payments will take time, Kohli said, as FIs and corporates will have to undo and reconfigure previous technology integrations.

As part of its ongoing mission to understand, influence, and drive the industry toward a ubiquitous faster payments system, the FPC conducted the survey of payments system stakeholders to gauge their views on a variety of topics related to faster payments in the United States. Contact: Elizabeth Grice U.S.

23, the industry welcomed the rollout of ubiquitous faster payments to every consumer and business in the U.S. NACHA is continuing to look at tokenization and better understand the implications on all parties, looking at the investment in the technology, the advantages and reduced risks it provides. via all banks and credit unions.

Consumers like their cards, their rewards and their ubiquitous acceptance. Yet Cagney’s view is that merchants using this blockchain-underpinned system will have the money to encourage consumers to switch. The IRS is also contending with inter-departmental communications and challenges of having everyone work from home.

You can also schedule a demo to learn more about our AP usecases! The growth in technology has seen the process of invoice processing move through three major phases. This template is unique to each usecase, organisation and mostly for each different kind of invoice. Want to automate invoice processing ?

As you know, we’ve been looking at blockchain for quite a while, understanding the technology standards, doing pilots with banks and filing a number of patents. That nervousness is not entirely misplaced, Lambert noted, because cryptocurrencies and blockchain technology are innovative and extremely new.

The partnership continues Mastercard’s role as the exclusive instant payments software provider for TCH’s RTP network, enabling both companies to integrate new instant payment usecases across a range of payment flows. Instant payments became a reality in the U.S. for the RTP network and around the world.

Financial institutions are constantly on the hunt for an edge when it comes to mobile banking and other innovations, and that’s playing out with new, emerging 5G mobile network technology. As that mobile technology gets closer to mainstream introduction, the potential 5G ecosystem for FinTech and mobile banking is gaining clarity.

As Karen Webster noted in an interview with Acuant CEO Yossi Zekri, although technology (and even usecases) are still evolving when it comes to digital identity, some basic “best practices” can be identified and embraced. “If In the end, the transaction is a process marked by frictionless behavior and individual control.

Less than two months after its implementation, Same Day ACH, the ubiquitous faster payments initiative for the payments industry in the United States, is showing a significant impact on the market, but it still has plenty to learn from those across the pond. In October alone, the ACH Network processed nearly $5 billion in 3.8

AI pioneers like Google and Amazon, who have adopted these new technologies to create a growing competitive advantage, have already witnessed bottom-line benefits from their AI strategies. Within AI there are multiple technologies and segmentations, with machine learning (ML) being one of the largest and fastest growing.

But there is still a long ways to go, and in the several years since the Faster Payments initiative first began, it’s also morphed to evolve along with the technology available. Naturally, one of the first usecases to come to mind for real-time payments is P2P payments. to launch their own faster payments efforts.

One such innovator recognized the vast commerce potential that could be unlocked if new technologies were used to move money and messaging between people in near real-time. Reid, who had successfully used an early version of the telegraph in battle and saw its potential for much, much more, including commerce. The year was 1837.

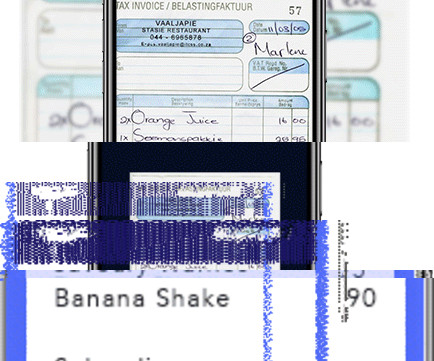

However, keeping track of data in a way that enables secure storage, efficient access and analysis, compliance with regulations and — ultimately — its profitable use is quite another topic. Those two extremes come together in a rising technology called multi-variant tokenization. Retail UseCase.

How can we look to this rapidly growing business for new usecases for instant payments? stakeholders should be supporting and identify the challenges in building out the API features that are required for ubiquitous access. What will this look like in the coming years?

Supermarkets are home to some of retail’s major and ongoing technological advances — and 2018 stands as a big year for grocery innovation. A year from now, that “access will be ubiquitous,” he said, and providing access to digital currency will eventually “become table stakes.” That doesn’t mean they can’t be about innovation.

Documents are ubiquitous in business and serve as the foundation for data, information, and knowledge. However, with the rapid advancement of technology, document processing now refers to the use of automated tools that can process documents with little to no human intervention.

banking industry, as well as the inconsistencies in digitization, make the path toward ubiquitous Open Banking even more uncertain. Sam Bobley, co-founder and CEO of data digitization technology firm Ocrolus , recently spoke with PYMNTS about what the financial services industry can do today to prepare for the Open Banking future. “We

Technology underpins everything these days. Ever more so this is the case with payments and specifically the conduits that get payments from party A to party B. From an ACH networks standpoint, noted Estep, innovation may be “skinny,” but operations are ubiquitous, connecting all the bank accounts in the United States.

The usecase, then, was the ability to enable smartphones to be more accessible for the visually impaired. And there is a wide range of usecases very suitable to visual recognition technology. “As Apart from a technological issue, however, Rizzoli noted that the bigger challenge was actually psychological.

Twelve years later, however, mobile banking has become ubiquitous across much of the global financial ecosystem. He recently told PYMNTS that banks’ solutions must offer everything for which consumers are looking, and they must actively innovate to support new usecases. Digital transformation for the future.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content