This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Threat actors then attempt to tap the mPOS against an unsuspecting consumer’s purse, wallet, or pocket to initiate a card-present-transaction on the mPOS. Another variation of this scheme involves the threat actor using previously stolen cards to conduct the fraudulent transactions using the mPOS registered to the created fake merchant.

For businesses like retailers and restaurants, there are 4 levels of PCI compliance, determined primarily by the number of transactions that business processes each month. For serviceproviders, such as credit card processors, there are only 2. PCI compliance only applies to the business or serviceprovider that was validated.

As of June 30, 2021, a new rule on supplementing data security requirements goes into effect for ACH originators that have an annual volume of 6 million transactions or greater. The rule requires the originators (and thirdpartyserviceproviders) to protect bank account information unreadable when it's stored electronically.

In a blog post, Dave blamed the data breach on Waydev, a former third-partyserviceprovider. According to the FinTech, the “malicious party” gained access to user passwords “stored in hashed form using bcrypt , an industry-recognized hashing algorithm.”.

It also enables organizations to take advantage of competition between leading serviceproviders, and to shift a higher volume of transactions or workload to different providers as they lower prices. Choosing the right third-partyserviceproviders can be tactical.

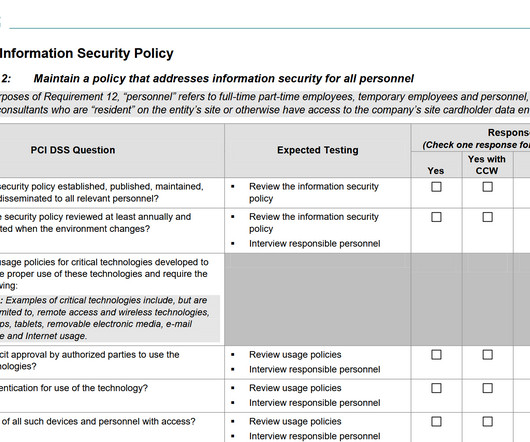

In the world of digital transactions, businesses handling payment cards must demonstrate their data security measures through the Payment Card Industry Self-Assessment Questionnaire (PCI SAQ). Level 1 merchants and serviceproviders, mandated by PCI SSC or customers, must complete a Report on Compliance (RoC), while others use an SAQ.

bank-funded entity that was mandated by the Competition and Markets Authority to provide new ways for customers to share their financial data with non-bank providers, has released an API specification for accounts and transaction information and payments initiation. Open Banking, the U.K.

SAQ Type Businesses it Applies To SAQ-A This SAQ is for businesses that are entirely card-not-present meaning online transactions. It also does not apply to card-not-present transactions that your staff manually keys into your payment system. SAQ C-VT This SAQ is where card-not-present keyed transactions come in.

Although this case is directly related to the Collections industry, it has great significance to the TPPPA members and their customers, as it threatens to link the usage of third-partyserviceproviders to consumer data privacy.

Lior Cohen, senior director of cloud security products and solutions at cybersecurity firm Fortinet , recently told PYMNTS why the digitization initiatives many payment serviceproviders undergo in the name of better customer experience can exacerbate security risks.

Yet both of these strategies require a third-partyserviceprovider to facilitate payment processing, whether funds are coming in via check or ACH. It gets taken somewhere and converted into an electronic transaction — typically ACH — and then moves through the network that way. The Check-To-ACH Migration.

The demand for faster payments is growing as companies look for swift, data-rich ways to transact. Businesses are accustomed to turning to their banks for access to payments services, so financial institutions (FIs) that wish to remain competitive need to be able to meet this need.

Mastercard said in a statement that the incident “has no connection to Mastercard’s payment transaction network … there was an event involving the Specials loyalty platform in Germany managed by a third-party vendor, which resulted in the unauthorized distribution of certain information.”.

The newspaper cited Ripple’s use of blockchain technology and the ability of two small banks, one in Canada and one in Germany, to complete cross-border online transactions in record time as an example of the latest banking innovations. Paym is a service launched in the U.K. There are 3 million users so far.

Speaking with PYMNTS, Adrian Floate , managing director of Australia-based Cirralto , explored some of the emerging payment models that have the potential to combat the pain of late payments and strengthen cash flow on both ends of a B2B transaction. The Rise Of BNPL.

The exchange’s APIs will span product offerings and service offerings such as deposits, foreign currency exchange, insurance and loan offerings — and will also include safe deposit boxes, branch and ATM services that are part of general banking operations.

Compliance with PCI standards is mandatory for any business that handles credit card transactions. Here are five reasons why PDF forms fall short of the stringent requirements for secure credit card transactions. 1. However, when collecting payment card details, PDF forms present significant compliance issues with PCI Standards.

Major risk factors for PayFacs include fraudulent transactions, merchant credit risk, regulatory compliance, and operational risks. Fraudulent transactions Malicious parties are always on the lookout to exploit vulnerabilities online to steal information and money.

But sometimes, the biggest B2B payments and accounts receivable pain points start even before a transaction occurs, according to Rich Wessels, treasurer for transportation management and logistics technology company Transplace. “I Failure to Act.

So rather than a team of financial professionals taking a random sample of corporate transactions and manually searing for anomalies and evidence of fraud, AI tools can analyze every data point and more accurately pinpoint areas of concern. in particular.

Acquired by the global financial technology leader FIS (NYSE:FIS) in 2019, Worldpay stands as the top acquirer on Nasdaq in terms of market capitalization and is also recognized as the largest global acquirer based on general-purpose transaction volume. The FIS group has facilitated over $20 billion in transactions from card to crypto.

Approval Code A code provided by the payment processor to indicate that a transaction has been approved. Authorization The process of verifying that a transaction can be approved and funds are available for the transaction. Average Ticket Size The average dollar amount of each transaction processed by the merchant.

For their end users on either side of the transaction, speed matters, and online commerce may comprise the bulk of a firm’s top line. Where once payments settled in three days, which gave FIs a window in which to “repair” transactions, that window has now closed.

Financial institutions (FIs) can centralize liquidity and cash management and streamline transaction flows for their business customers. Business customers, meanwhile, can more easily reconcile transactions associated with their paying customers and their purpose of payment.

Today, the framework introduced in the early 2000s outlines 12 PCI requirements that merchants must satisfy to process credit card transactions on the card networks. PCI Levels vary by card brand but are generally determined by an organization’s current or projected annual card transaction volume.

Federation of Small Businesses (FSB), research of 1,000 small business owners revealed that fewer than one in seven SMBs are sharing their bank data with third-partyserviceproviders. HSBC also noted that the integrations support heightened visibility into the status of a transaction, both for the sender and beneficiary.

Clark emphasized the importance of third-partyserviceproviders delivering a clearer message to accounts payable departments. One method of driving ePayables adoption is taking a broader view of the transaction life cycle, and stepping back to look at the whole transaction lifecycle from source-to-pay,” Clark said.

” It’s why holistic serviceproviders in the B2B payments space must include support for paper checks, as clunky as the rail may be. In the least, a third-partyserviceprovider can reduce the friction of checks by taking on the printing and mailing for its clients, cutting down on cost and wasted time.

That is, without having to pay the fees or give up customer data to third-partyserviceproviders like PayPal or Visa — information that can be valuable to businesses that want to develop their own loyalty programs, for example.

While providing business clients access to faster payment capabilities is a plus, Berkshire Bank and Finastra pointed to the opportunities of transaction visibility and API integration as key to adding value for corporates. he added, and the current transaction cap of $25,000 could stunt corporate uptake of the tool.

The decentralized-record-keeping technology, which is designed to instill trust in the authenticity of digital transactions, could be used to create efficient solutions for both commercial and residential real estate — from buying property to digitized “smart contracts” to crowd-sourced investments. Imbrex’s platform.

The National Automated Clearing House Association (NACHA) governs the operation of the Automated Clearing House (ACH) network , a centralized system financial institutions use to facilitate electronic payments and transactions across the U.S.

Reports in Coin Desk said Aruba’s ATECH Foundation is collaborating with Switzerland-based Winding Tree to develop a blockchain-based marketplace to facilitate travel booking to the island, an effort to regain some of the lost revenue that ends up with third-partyserviceproviders like online travel agencies and airlines.

BNPL arrangements, which refer to a type of short-term financing that allows consumers to make purchases and pay for them over time, help banks improve customer retention and acquisition, increase transaction volumes, and strengthen their relationships with merchants. billion through over 50 million transactions since its inception.

Many banks have increasingly leveraged and become dependent on third-partyserviceproviders to support key operations within their banks,” the report stated. Over time, consolidation among serviceproviders has resulted in large numbers of banks reliant on a small number of serviceproviders.”.

But with an intermediary FinTech facilitating these transactions, Chanda said his customers are less inclined to delay vendor payments, while the transaction itself is less likely to include errors because the payer has handed off the payment process to a specialist. Checks are, in large part, paid on time,” said Chanda.

While traditionally, banks have controlled the infrastructure, hardware and operating systems for financial services, new entrants may have the agile infrastructure and innovative propositions to personalize to meet individual consumer needs.

The speed of transaction and its fulfillment with no delay shapes customers’ buying experience and encourages them to return to the merchant again and again. It is in the best interest of merchants not only to provide an excellent service but also to use an infrastructure that can expand their business opportunities.

ISOs facilitate payments and provide ongoing support for their clients, which makes them a quality solution for many businesses that don’t want to directly cooperate with a large banking institution. ISOs can offer companies payment processing services as they are partnered with acquiring member banks or payment processors.

File formats vary from bank to bank, requiring data to be transformed, or converted, for successful transaction processing, which can lead to significant lag time.”. A similar conundrum is likely to arise as more jurisdictions embrace new payment systems that support faster cross-border transactions. Tripping Up Cash Management.

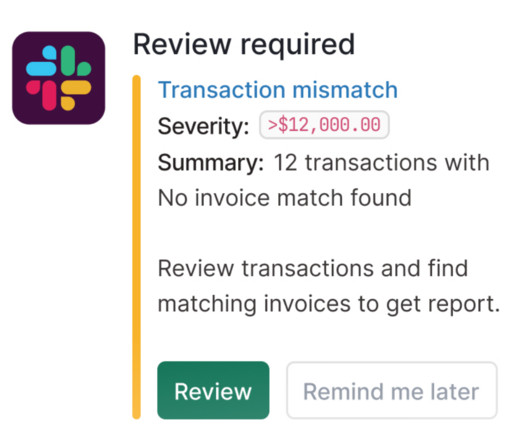

This process typically involves reviewing transactions, invoices, receipts, and other financial documents to verify that they match up with the company's records and budget. By thoroughly reviewing financial transactions and identifying any irregularities or unauthorised expenses, businesses can detect and prevent fraudulent activities.

Plaid’s API provides a powerful and popular tool by which third-partyserviceproviders can gain easy access to a consumer’s bank account — which has all kinds of applicable potential for the card network. In terms of mechanics, the acquisition — which involves a cash payment of $4.9

.” Kirsch says, “Bank’s over-reliance on out-dated networks and thirdpartyserviceproviders is not only commercially counterproductive, it is also a security nightmare.” The transaction settlement occurs instantly through Token if both banks are Token-enabled.

Walmart officials say they are reassessing terms of contracts with third-partyserviceproviders, with an eye toward handling more deliveries in-house and converting part of its inbound highway freight to lower-cost rail shipping.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content