This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

These circumstances have brought to the fore what has long been a central concern for lenders: assessing and managing creditrisk. This vital task is complicated even in normal times due to the multitude of financial risk factors in play at any given time. percent employ it for creditunderwriting.

Bloomberg customers will now be able to use the news site's terminal to look at Credit Benchmark 's creditrisk data, which comes from risk views of the world's largest financial institutions, according to a press release. They can also assess ongoing credit quality.

Today in B2B, Bloomberg broadens its creditrisk data pool, and two ERP solutions secure B2B payments integrations. Bloomberg To Incorporate CreditRisk Data. The release stated firms have more often been looking for data to validate their own internal counterparty and creditriskassessment.

Alternative lending companies are one of the strongest examples of how leveraging rich financial transaction data can be used to go beyond traditional creditriskassessments, says Finsync's Eddie Davis.

The machine learning study compared results from a Ford Credit scoring model with a machine learning model developed by ZestFinance using its underwriting platform to do deeper analysis of applicant data. Although these consumers may have steady jobs, their creditworthiness is heavily based on credit history.

Inaccurate and slow creditriskassessment for [small- to medium-sized business (SMB)] commercial loan requests is one of the major reasons that over 50 [percent] of loans are currently declined by financial institutions (FIs),” said Roger Vincent, chief innovation officer at Trade Ledger.

Home Credit , a global non-bank consumer lender, has successfully reduced its creditrisk while maintaining loan volumes and keeping approval rates steady by incorporating the FICO® Score X Data to optimize its loan process in China. They are one of our most sophisticated clients in terms of advanced analytics.”. by FICO.

By leveraging line-by-line transaction data, Recap’s creditrisk engine can assess a merchant and return a funding offer in under two minutes without any further underwriting requirements such as a credit check on the owner or management accounts or business bank statements.

“By analysing big data and rapidly assessingrisks, AI empowers financial companies to make well-informed decisions. However, a significant revolution lies ahead – the personalisation of services based on individual user assessments. “Finally, AI is reducing risk in the embedded insurance space.

Equipment finance company CapX Partners has announced an integration of Moody’s Analytics technology to strengthen its underwriting and risk mitigation capabilities. “Assessing the creditworthiness of small businesses in a cost-effective manner is one of a lender’s most challenging tasks,” he said.

CreditRisk and FICO Score Trends? creditrisk and FICO® Score trends. At the same time, increasing adoption of recent innovations in credit scoring solutions should benefit consumers, leading to greater consumer empowerment opportunities and credit access.

By leveraging line-by-line transaction data, Recap’s creditrisk engine can assess a merchant and return a funding offer in under two minutes without any further underwriting requirements such as a credit check on the owner or management accounts or business bank statements.

FICO Scores Are Not Fixed Estimates of CreditRisk. The FICO ® Score is designed to rank-order the likelihood that a borrower will repay their loan(s), with higher scoring borrowers representing lower risk, and lower scoring borrowers representing higher risk. So are FICO ® Scores “artificially inflated”?

PayFacs handle riskassessment, underwriting, settling of funds, compliance, and chargebacks which exposes them to greater potential risks. Major risk factors for PayFacs include fraudulent transactions, merchant creditrisk, regulatory compliance, and operational risks.

MoneyLion has teamed up with Nova Credit to integrate cash flow underwriting into its decisioning engine, enabling credit issuers on its platform to access more comprehensive data for evaluating consumers’ financial health.

invoice insurance provider Nimbla is teaming up with the creditriskassessment firm Wiserfunding , according to a report in Crowdfund Insider on Friday (May 29). The partnership is a result of the launch of the FinTech task force Innovate Finance , which took place in March, the report said.

But it occurred to them that their solution was useful outside of HR — and that many of the things that made someone a good hire of over time could also make them a good creditrisk over time, if the artificial intelligence (AI) model they were using to screen with were modified to that task.

Some of the top thought leaders in banking, finance, artificial intelligence, machine learning, and creditrisk came together in San Francisco to discuss the key trends and innovations in our industry. A key driver of successful financial inclusion is the ability for lenders to effectively gauge the risk of an underserved consumer.

In some instances, this helps them offer consumers new credit opportunities, and in other cases it might illuminate risk,” noted Paul DeSaulniers, Experian’s senior director of Risk Scoring and Trended/Alternative Data and Attributes. Lenders’ primary goal is to assess a consumer’s stability, ability and willingness to pay.

The debt funding was led by BHI, ConnectOne Bank, IDB Bank, Viola Credit and a large insurance company. Lendbuzz’s financing model, which is powered by machine learning and proprietary algorithms, allows it to better assess the creditworthiness of consumers with limited U.S.

The new-age credit stack can do this efficiently with smarter underwriting capabilities, integrated data collection mechanisms and ability to automate workflows in the process. Improved Risk Management To assesscreditrisk accurately, new-age credit stack incorporates advanced algorithms and real-time analytics.

I had the pleasure of speaking on a panel at ABS East yesterday, entitled “Traditional vs Non-Traditional Underwriting, Does Machine Learning Teach Us Anything New?”. The panel primarily focused on the opportunities and challenges associated with the use of Machine Learning (ML) in creditunderwriting.

A low FICO score for a consumer can have the perverse effect of preventing them from having access to a second chance through manual underwriting. We all know that having a higher credit score helps a consumer gain access to credit and get better terms from a lender. JessicaButalla@fico.com. Tue, 07/19/2022 - 16:11.

The updated model reflects the evolving credit landscape and credit behavior to help better inform a higher level of consumer creditrisk prediction. The validation results for FICO Score 10 T demonstrate improved creditrisk prediction for this segment of the population.

Having announced a partnership with Dun & Bradstreet , Velotrade is expanding the pool of data from which it draws to underwrite financing. The first and most obvious risk is creditrisk, or the risk that a business will fail to repay financing.

While access to credit is crucial for many people and companies, lenders must also protect themselves from the risk of default and ensure that they can remain financially solvent in the long run. Without proper filtering, lenders run the risk of approving high-risk borrowers, which can lead to increased loan defaults and losses.

Morgan’s financial strength and Slope’s innovative approach to creditriskassessment and monitoring. The fact that they not only use AI for initial underwriting, but also for the ongoing risk monitoring of the portfolio, is what really attracted us to Slope. The partnership brings together J.P.

The BNPL platform then assesses their creditworthiness through a soft credit check. Once the platform approves the credit line, it pays the merchant the full amount of the goods purchased, thus taking on the customer’s creditrisk. million) in Q3 2023 compared with a loss of SEK 2.1

To better help marginalized consumers access the credit they need, the company doesn’t require them to have a credit score to qualify for the card. Instead, Petal leverages users’ open banking data as underwriting data to offer them credit and help them establish a credit history. credit card market.

Its biggest plan, reports said, is to use QuadMetrics’ capabilities in predictive analytics and riskassessment strategy to create an “enterprise security score” for business customers. FICO said it hopes to provide a tool to underwrite companies’ cybersecurity levels.

A press release issued this week said that BNB Bank, a community bank operating across the New York and Long Island metropolitan area, will integrate PayNet technology to enhance its underwriting process for small business loans. In another statement, BNB Bank EVP and Chief Lending Officer Kevin L.

The complaints vary in their specifics, but all revolve around a basic premise: The old credit-scoring models are too backward-looking in a world where real-time data is available — and they are insufficient to the task of properly assessingrisk. Aire, though, is a credit-assessment platform intended to fill in that extra data.

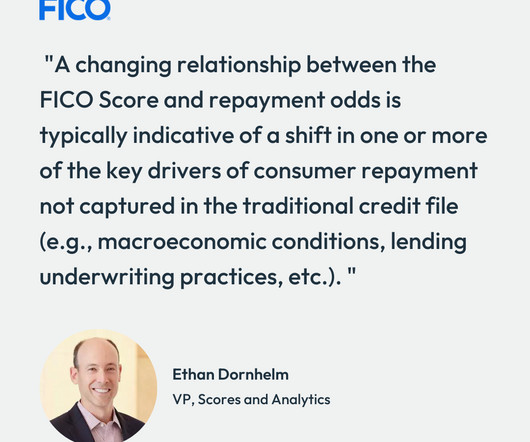

What the FICO Score is not designed to do is provide a specific, fixed estimate of creditrisk; we know from tracking the scores over three-plus decades that the relationship between the FICO Score and consumers’ likelihood of loan repayment can and does shift over time and across economic and financial cycles.

There has been much discussion and several studies over the years regarding the potential value of leveraging rental data in assessing consumer creditrisk. Which raises the question: Should rental data be widely reported to the three primary consumer credit agencies (CRAs)? Does Rental Data Make Thin Files Fatter?

FICO is strengthening its position in the corporate underwriting space with a new solution for SME lenders. The company said Wednesday (April 5) that it is rolling out its Origination Manager Essentials solution for mid-market banks and credit unions. ” .

That means the big opportunity for X Financial comes from the 400 million or so Chinese consumers who have credit cards, but are hampered by limits that are too low. Those limits remain low because China is relatively undeveloped when it comes to credit bureaus and assessingcreditrisk, which makes lenders cautious and consumers frustrated.

Adjaoute said doing this goes far beyond what FIs can offer through manual, paper-based underwriting processes, which can keep applicants waiting for a month or longer. Evaluating creditrisk isn’t just about keeping fraudsters from getting loans under illegitimate identities. When Less Isn’t More.

At the center of many of these discussions is the issue of ACH underwriting, which sees FIs establish how long it takes for funds to actually settle into an account. The company’s stability, ability to cover insufficient funds and chargebacks are taken into account.

Primarily, Reckon provides small and medium-sized enterprises with cloud accounting solutions, but now, it’s utilizing the data it has about small businesses to its advantage by partnering with alternative lending company Prospa to underwrite loans to its SME users. “This is transforming the creditrisk analysis process. .

The “innovation” VantageScore claims can score more people is simply the weakening of credit score criteria. The minimum criteria needed to produce the FICO Score aren’t arbitrary — they are the result of decades of research into riskassessment. Delinquencies and collections. Inactive/stale.

One of those collaborators is CRiskCo, a creditrisk management company that deploys Big Data analytics to provide a business credit score to lenders and trade finance providers. Together, the businesses are going straight to the trading partners to protect a supplier against the risk of non-payment.

Commercial Lending ETA members are continuously working to expand access to credit by developing and deploying new online financing products tailored to the diverse needs of small businesses.

FICO Scores, of course, play an important role in the risk management and transparency that powers the secondary market. Now VantageScore is claiming that its score can be used instead in GSE underwriting (and by extension, securitization), as a one-to-one replacement for the FICO Score. Could a clean swap-out work?

Developed by FICO in partnership with LexisNexis Risk Solutions and Equifax, this innovative credit score utilizes alternative data—data not included in the traditional credit bureau file. The inclusion of this alternative data leads to a more reliable estimate of consumer creditrisk and helps score more than 26.5

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content