This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This is where PCIDSS (Payment Card Industry Data Security Standard) compliance becomes essential for Australian businesses. In todays article, we are going to learn how PCIDSS compliance protects businesses from data breaches. Regular monitoring and testing of networks: Performing routine security assessments.

This is where the Payment Card Industry Data Security Standard (PCIDSS) comes into play, serving as a crucial framework for safeguarding sensitive information and protecting both businesses and consumers from the ever-present threat of cybercrime. This assessment will help determine the scope of the compliance efforts.

PCIDSS is a set of requirements that is applied to every small and large organization that accepts, stores, processes, or transmits cardholder data. In particular, PCIDSS for SaaS companies is essential, as these platforms frequently handle sensitive customer information and must adhere to the latest security standards.

PCIDSS is a set of requirements that is applied to every small and large organization that accepts, stores, processes, or transmits cardholder data. In particular, PCIDSS for SaaS companies is essential, as these platforms frequently handle sensitive customer information and must adhere to the latest security standards.

The Payment Card Industry Data Security Standard (PCIDSS) compliance 4.0 offers essential guidelines and a framework to safeguard cardholders’ data and mitigate any potential data breaches that may occur in banks. In this blog, we will understand PCIDSS compliance 4.0

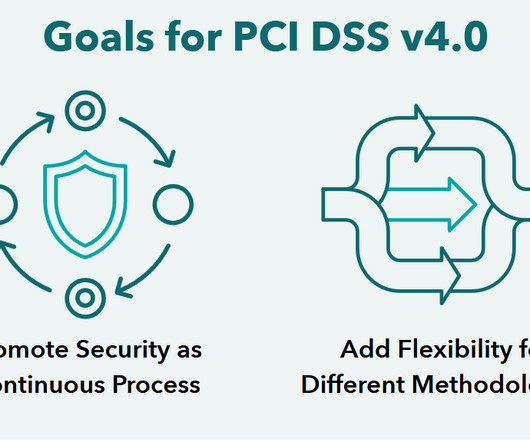

You can also check out the PCI at a glance infographic for a quick overview. For simplicity, I will just refer to PCIDSS standards as PCI for the rest of this article. What is PCI again? In the past, Ive written about how to achieve and maintain PCI compliance. Timeline PCI version 4.0

The PCIDSS Checklist is a crucial first step in securing your business. It’s a tool that helps businesses ensure they’re meeting all the requirements of the Payment Card Industry Data Security Standard (PCIDSS). To get started on your journey towards PCIDSS compliance, we recommend visiting the PCIDSS v4.0

Organization that are certified by CREST goes thorough assessments of their methodologies, quality assurance processes, and data security measures, offering assurance to clients seeking reliable and trustworthy security services. PCI QSA, QPA, and SSFA Certifications : Demonstrating expertise in payment security compliance.

Welcome back to our series on PCIDSS Requirement Changes from v3.2.1 These measures help mitigate vulnerabilities that hackers could exploit. PCIDSS v3.2.1 PCIDSS v4.0 c: Confirm that software applications comply with PCIDSS. - In PCIDSS v4.0, In PCIDSS v4.0,

The Payment Card Industry Data Security Standard (PCI-DSS) is a set of global standards developed to safeguard cardholder data. Staying up-to-date with PCI-DSS compliance should be a top priority. This guide will break down what you need to know about PCI-DSS compliance. PCI-DSS version 4.0,

The merchant underwriting process is a critical step that payment processors and financial institutions use to assess the risk associated with onboarding new businesses. Key steps include application review, risk assessment, credit checks, and compliance verification. Learn More What is Merchant Account Underwriting?

Sends leverages AI to mitigate risks, comply with FCA, PSD2, and PCIDSS, and enhance client experience with secure and innovative services. Strict compliance with FCA, PSD2, and PCIDSS protects consumers and combats financial crime, but implementation demands resources and adaptation.

Promoting Accountability: Encouraging financial institutions to take responsibility for securing their local environments and ensuring compliance through independent SWIFT CSP assessments. Test the IRP periodically to ensure its effectiveness in mitigating cyber incidents. Conduct regular vulnerability scans and penetration tests.

Identifying and Assessing Risks Understanding the lay of the land is the first step in effective risk management. Conducting a thorough risk assessment tailored to the specific nature of the business is essential. Conducting a thorough risk assessment tailored to the specific nature of the business is essential.

What is SWIFT CSP The SWIFT CSP, launched in 2016, is designed to mitigate cybersecurity risks and enhance the overall security of financial institutions. Adopt a Risk-Based Approach Conduct regular risk assessments to identify vulnerabilities and address them proactively. Plan for Incident Response and Information Sharing 7.1

TL;DR PCI compliance is essential because it helps prevent data breaches, ultimately cultivating customer trust. There are 12 requirements under PCIDSS, divided into six major categories. What is PCI Compliance? PCIDSS stands for “Payment Card Industry Data Security Standards.”

Promoting Accountability: Encouraging financial institutions to take responsibility for securing their local environments and ensuring compliance through independent SWIFT CSP assessments. Test the IRP periodically to ensure its effectiveness in mitigating cyber incidents. Conduct regular vulnerability scans and penetration tests.

TL;DR The PCIDSS determines security protocols and sets the standards for payment security. How to Comply with Payment Security Standards The Payment Card Industry Data Security Standards, or PCIDSS , are the North Star for payment processing security. Q: How do I ensure online payment security?

SaaS companies must adhere to industry standards such as PCIDSS to ensure customer transactions are safe. How to mitigate this risk: Before committing to a provider, carefully review contract terms to ensure flexibility.

A GDPR-compliant password policy should enforce unique passwords for each account to mitigate the risk of credential stuffing attacks. These may include: SOC1/SOC2: Service organization control reports that assess controls related to financial reporting and data security. PCI PIN and PCIDSS: Standards for securing payment card data.

Enter the Payment Card Industry Data Security Standard (PCIDSS): a comprehensive framework that sets forth stringent rules and regulations to ensure the secure handling, processing, and transmission of cardholder information. As we approach the highly anticipated release of PCIDSS 4.0 a notable change is on the horizon.

It provides merchants with an overview of their payment activity and helps assess overall business performance. By analyzing AOV alongside transaction volume, merchants can assess the effectiveness of marketing campaigns, pricing strategies, and upselling techniques.

Encryption and transfer of payment information The payment gateway that underpins your checkout page will now encrypt the customers payment details as stipulated by industry data security regulations like PCIDSS (Payment Card Industry Data Security Standard) before transferring the data to your payment processor.

To mitigate this, perform additional QA in controlled production settings, or use gateways that offer advanced testing tools and staging environments closer to live conditions. Fraud detection systems might not be active in the sandbox, leading to a false sense of security.

At the same time, robust AI data governance is necessary to ensure that AI models use high-quality training data in an explainable manner to mitigate bias, excessive false positives, and unintended risks. Our solutions comply with PCI-DSS, ISO 27001, and SOC2 standards to ensure security and privacy.

These fees typically include interchange fees, which go to the card-issuing bank, assessment fees charged by the card networks, and payment processor fees for handling the transaction. The total cost varies based on factors like the type of card used, the transaction method, and the merchants industry.

Common risk management strategies for PayFacs include proper merchant vetting and onboarding, transaction monitoring and fraud prevention, chargeback mitigation, KYC/AML compliance, and data breach prevention. You should also have contingency plans or initiatives in place to mitigate the impact of a risk.

6 common challenges in invoicing and billing Understanding various invoicing and billing challenges will allow your business to proactively mitigate these issues to maintain positive financial health and reputation. Regulatory compliance: Invoicing and billing compliance means adhering to legal and financial regulations.

To properly evaluate payment gateway providers, merchants should conduct thorough research, participate in demos and trials, assess vendor reputation, and review customer support options for each. During this time, you can assess the gateways features, user interface, and security measures.

It manages payments and transactions with the bank for a number of smaller merchants, streamlining the process, decreasing the workload, and mitigating risk. Only you can assess which option is the right one for your business. How it works: A payment facilitator acts as a payment aggregator partner to smaller merchants.

A risk assessment follows, evaluating the merchants profile through credit checks and performance analysis, leading to application approval or rejection based on these findings. Compliance monitoring ensures adherence to regulations like PCIDSS and AML laws. Request a demo today to explore our MMS solution and its capabilities!

High-Risk Classification: A Core Concern Regulators and card schemes classify businesses based on perceived risk, assessing the likelihood of chargebacks, fraud, and other liabilities. Open dialogues can address potential concerns and highlight the companys commitment to mitigating risks.

Security and Compliance in Merchant Processing Any business that accepts credit and debit card payments must be compliant with the Payment Card Industry Data Security Standards (PCIDSS). The PCIDSS contains twelve stringent requirements that protect both the merchant and the customer from data breaches and identity theft.

A loan origination system is a software solution that automates the entire loan process for lenders, right from lead generation and customer onboarding to credit assessment and transfer to the loan management system. What is a Loan Origination System?

Credit card fees, including interchange, assessment, and payment processor fees, impact businesses on a per-transaction or recurring basis. Assessment fees An assessment fee is imposed by payment networks in exchange for processing credit card payments. PCI compliance fees. 2% of the total transaction value.

Merchant underwriting requires a thorough assessment of a business’s potential financial risks to ensure safe and secure transactions. Risk assessment: After gathering the necessary information, a risk assessment is conducted to evaluate a business’s risk profile.

Assessment Fees: Charged by card networks (e.g., PCI Compliance Fees: Fees for maintaining compliance with Payment Card Industry Data Security Standards (PCIDSS). Non-Compliance with PCI Standards: Payment Card Industry Data Security Standards (PCIDSS) compliance is mandatory for businesses handling card transactions.

SMBs also fall victim to cyber criminals, as many lack the resources and knowledge to set up threat mitigation strategies, leaving them vulnerable to attacks. Compliance with Industry Standards Your business should comply with industry bare minimums like Payment Card Industry Data Security Standard (PCIDSS).

Look for a gateway that includes PCI compliance, fraud detection tools, chargeback mitigation strategies, and AI-driven risk analysis to protect transactions and user data. Solution with Segpay: Built-In Compliance Tools Segpay is a fully PCIDSS Level 1-compliant payment processor, ensuring secure transactions.

Reduced manual data entry and errors Embedded Sage payments also reduce the necessity for manual data entry, thus mitigating the risk of human error and freeing up valuable resources. To make choose the best embedded payment processing solution, you should: Start by assessing your payment needs. Consider integration capabilities.

Merchants typically encounter three primary types of fees: interchange fees paid to the card issuers, assessment fees paid to credit card networks, and various payment processor fees that cover the services provided by merchant services providers. Still, merchants should be aware of other potential charges that may apply.

Ensure the selected payment gateway complies with the Payment Card Industry Data Security Standards (PCIDSS) to protect your customers’ payment information. The system’s efficiency mitigates late and missed payments, contributing to a steady and predictable cash flow.

Conduct credit risk assessments: Credit risk assessments involve analyzing factors such as the client’s financial stability, payment history, and credit score. Thoroughly evaluating the creditworthiness of potential clients will allow your company to identify and mitigate the risk of non-payment or late payment.

By running multiple test transactions, businesses can examine real-time data updates, assess the user experience, and ensure customer card data is handled securely. Within Microsoft Dynamics 365, several data security measures must be taken to ensure compliance with industry regulations, such as the PCIDSS Standards.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content