This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

It applies to any entity that processes, stores, or transmits credit card information making it especially relevant to banks and financial institutions. Compliance ensures robust security practices to prevent breaches and protect sensitive payment card data. Staying up-to-date with PCI-DSS compliance should be a top priority.

The Many Types of Payment Processing Fees Below is a breakdown of the lesser-known or hidden fees that can show up on your monthly statements: Interchange Fees What It Is: The fee paid to the card-issuing bank every time a customer buys something with a credit or debit card. Cost Range: Usually 1.5%3.5% The processor charges a higher rate.

It’s more complex than domestic payments, as it requires a payment infrastructure that supports global payment options and multiple currencies while ensuring security and compliance with foreign regulations. Compliance with International Regulations Expanding internationally also means complying with local regulations in each new market.

Clear Junctions findings stem from a recent poll of 150 senior payment industry executives conducted during its MiCA Masterclass webinar hosted in collaboration with financial services compliance consultancy fscom. 20% report difficulty in understanding compliance requirements during the Grandfathering period.

According to the Bank of England, RTGS settles approximately £500 billion between banks each day—around a quarter of the UK’s annual GDP—in sterling central bank money. Democratised access will foster fintech-bank collaboration, driving innovation. RT2 is substantially expanding direct participation.

Its the gateway to onboarding, compliance, trust, and ultimately, conversion. Now, thanks to open banking and the EUs Instant Payments Regulation (IPR), regulated businesses are rethinking whats possible: real-time transactions, richer customer insight, and smoother experiences, all while staying compliant. Its a strategic shift.

From then on, banks need to be able to process MX messages, which contain much richer and more structured data. A few banks have already transitioned, but many more have yet to make the switch. Non-compliance may result in failed payments, operational inefficiencies, regulatory scrutiny, and reputational damage.

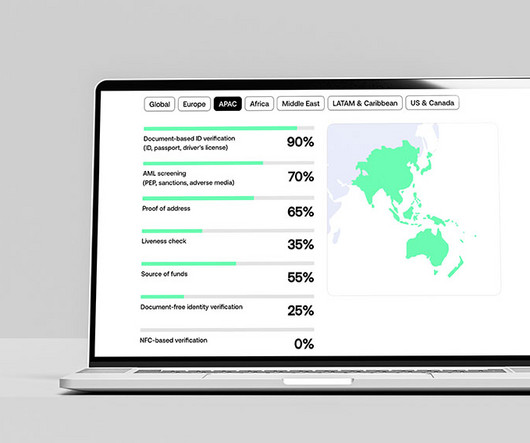

The report, based on Sumsubs internal identity verification and user activity data from 2023 and 2024, along with a survey of over 300 companies across the crypto, banking, payments, and e-commerce sectors, reveals that APAC was the only region to record a decline in crypto fraud in 2024, with fraud rates dropping from 2.6%

This article walks you through what credit card surcharge compliance really means and provides a practical checklist to help your business stay on the right side of the rules. These aren’t just suggestions, they’re critical guardrails that protect your business from non-compliance and ensure transparency with your customers.

From pay-by-bank solutions to futuristic voice-activated payments, 2025 promises to bring significant advancements. Open banking, or pay-by-bank, is another trend to watch. This is driven in part by regulations like the Instant Payment Regulation (IPR), which enforces real-time bank transfers.

Notably, the rise of cryptocurrencies, stablecoins, and Central Bank Digital Currencies (CBDCs) are transforming the digital payments landscape. This uncertainty creates serious compliance challenges, including: Non-compliance risks, with businesses potentially facing fines, legal scrutiny, or even banking restrictions.

Pix, Brazil’s instant payment system developed and managed by the Central Bank, has changed how transactions are made in the country. The new regulations introduce stricter compliance requirements, requiring all payment transactions for sports betting operations to be verified against player-registered bank account details.

This reclassification has significant regulatory and commercial consequences for the EMI sector, potentially raising compliance costs, impacting bank partnerships, and limiting innovation. The rationale centres on several key factors: The speed and scale at which EMIs can onboard customers, Their provision of bank-like services (e.g.

These compliance standards aren’t just check boxes; they are tools that protect your business and build confidence. Most importantly, you’ll see how the right digital payment solution can make compliance simpler and more effective. Why compliance matters in digital payment processing Staying compliant isn’t a choice.

And yet, accepting non-cash forms of payments is more or less required to operate a modern business, at least in the U.S. They include: the merchant, cardholder, card associations, acquiring bank, issuing bank, and payment processor. Acquiring Bank: The business’ (i.e., merchant’s) bank.

Moreover, network tokenisation reduces the regulatory burden by eliminating the need to store sensitive card data, supporting the Payment Card Industry Data Security Standard (PCI DSS) compliance and lowering the risk of data breaches. With FedNow enabling instant payments in the US, speed and reliability become non-negotiable.

Its the bridge between an eCommerce website, its customers, and the bank. Its the third-party service that serves as the link between the payment gateway, acquiring bank, and issuing bank or card network. It works in tandem with the customers bank or credit card provider to verify and authorize the transaction.

Emerging trends such as cross-border payment systems and open banking initiatives are breaking down traditional barriers, fostering greater connectivity and efficiency in Asias financial landscape. The shift toward digitised payments brings heightened concerns about cybersecurity, fraud, and regulatory compliance.

Central bank digital currencies (CBDCs) have rapidly evolved from theoretical concepts into live pilots and national deployments. From Asia to the Caribbean and Europe, central banks are grappling with how to digitise public money while preserving trust, utility, and sovereignty.

Merchant services help small businesses simplify payments, save money with transparent pricing, and secure transactions with fraud protection and PCI compliance. This system guarantees secure data transmission between banks and card networks like Visa, Mastercard, and Discover. They work through a dedicated merchant account.

Through the updated PayRetailers Pix solution, the firm is aiming to help Brazil’s betting operators comply with new regulations that require payments to be processed through bank accounts registered to individual players.

A quiet revolution is underway, and it’s being led by Real-Time Payments (RTP) - systems that enable the instant transfer of funds between bank accounts, 24/7, with settlement occurring within seconds. Many banks still operate on platforms that are fundamentally card-centric. But their relationship is changing.

The merchant underwriting process helps reduce fraud (including chargeback volume), ensures compliance with regulations, and protects financial stability in the payment processing space. Key steps include application review, risk assessment, credit checks, and compliance verification. Learn More What is Merchant Account Underwriting?

Even when a dispute is unsuccessful, the acquiring bank will withhold payment for any chargebacks until the matter is resolved. Add in the fees charged by banks and processors, and even disputes which turn out in your favor can be expensive. EMV Liability Shift Non-Counterfeit Fraud 10.3: The individual codes are: 10.1:

Ensure the gateway offers PCI DSS compliance, encryption, tokenization, and fraud prevention tools to safeguard transactions. In turn, the payment processor ensures a seamless transfer of the information between the merchant, issuing bank, and customer. Learn More What is a Payment Gateway? Qualified transactions have the lowest rate.

Brankas , an open finance platform provider, has partnered with Vietnam-based technology firm Gimasys to deliver open banking solutions for the country’s financial sector. The collaboration aims to help banks and financial institutions comply with new regulations and accelerate their digital transformation efforts. ” Todd D.

Entities and Types of Scams Covered Under the Shared Responsibility Framework The SRF applies to all full banks, major payment service providers (PSPs), and telcos with major roles in safeguarding consumers’ financial and communication activities. Telcos’ Duties Telcos play a key role in securing SMS channels used in digital banking.

A study by the Federal Reserve Bank of San Francisco showed that credit cards account for 31% of all payments, significantly more than cash at 18%, and debit cards at 29%. The company facilitates the transfer of information and funds between the customer’s bank and your business’ bank.

Yet, many businesses struggle with high transaction costs, fragmented infrastructure, and complex compliance. This triggers multiple challenges, including regulatory hurdles, higher MDRs (Merchant Discount Rates), FX volatility, and lower conversions as local payment methods and issuing banks are wary of non-local merchants.

TL;DR Processors act as the middleman between your customer’s card and your bank, but not all are created equal—some offer better service, pricing, and tools than others. Do they help with PCI compliance and dispute management? Let’s get started. Reach out to their support team and ask: Is phone support available 24/7?

These solutions are already widely adopted and focus on enabling technical interoperability between existing mobile wallets, offering fast and integrated payment experiences within their local banking ecosystems. Wero enables instant, account-to-account (A2A) payments without relying on traditional card networks. Here’s How We Enable That.

Interchange and assessment fees are set by card networks and are non-negotiable. Acquiring bank – The merchants bank that receives and disburses the funds. They facilitate transactions by connecting merchants, credit card processors, and banks while establishing rules, regulations, and fees for processing payments.

It collects payment data, secures sensitive information, and connects all parties needed to move money from your customer’s bank to yours. This tokenization keeps the sensitive card information off your servers, reducing the risk of a data breach and easing PCI DSS compliance. This decision is returned instantly.

As traditional banking processes are replaced by more integrated financial solutions, companies across industries are embedding payment processing, lending, insurance, and investment services directly into their platforms. The need for traditional banks to digitise has never been more apparent.

Buna’s compliance program integrates rigorous anti-money laundering (AML), counter-terrorism financing (CTF), and sanctions screening protocols both before and after settlement, offering real-time monitoring and thorough due diligence to safeguard financial transactions.

Acquiring bank This is the merchant bank that allows the business to receive money from card transactions and store these funds. The issuing bank This is the cardholders bank or the financial institution that issued their credit or debit card. Think: Visa, Mastercard, American Express, and Discover.

What began as CSR reporting has grown into real-time green incentives, making ESG a key strategy for both companies and banks. Banks and Fintechs now add sustainability scores to every payment. Some banks even offer higher deposit rates when companies hit diversity or emissions goals. ESG reporting started as a voluntary effort.

When implementing a surcharging program, businesses follow local regulations, ensure legal compliance, determine surcharge percentages and communicate transparently. Credit card networks and issuing banks don’t waive their cut; instead, these costs are shifted from the merchant to the customer.

Today, finance leaders are not only responsible for budgeting and compliance, but also for enabling growth through smart, scalable technology choices. Modern finance teams rely heavily on embedded finance, SaaS fintech software, finance APIs, and cloud-based platforms to run everything from payments to compliance to cash management.

From virtual assistants to risk modeling and hyper-personalized customer experiences, banks are betting big on AI to transform operations, reduce costs, and redefine digital engagement. This global heatmap of AI in banking draws on fresh data, case studies, and market insights to uncover the evolving landscape of AI adoption.

Its become clear that these policies arent optional enhancements, with both networks positioning tokenisation as the non-negotiable standard. Regulatory frameworks will inevitably follow, converting whats currently best practice into compliance requirements. Instead, a complex orchestration occurs between token requesters (e.g.

It highlights new corporate responsibilities, significant penalties for non-compliance, and the businesses need to implement strong fraud prevention measures to protect their financial and reputational standing. What’s next? For companies operating in the UK, understanding the implications of this legislation is critical.

That is including digital wallets, instant bank transfers, and buy-now-pay-later options, particularly tailored for regional preferences. However, Checkout.coms unique positioning enables it to carve out niches where flexibility, global reach, and performance are non-negotiable. Localisation is another key advantage.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content