This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

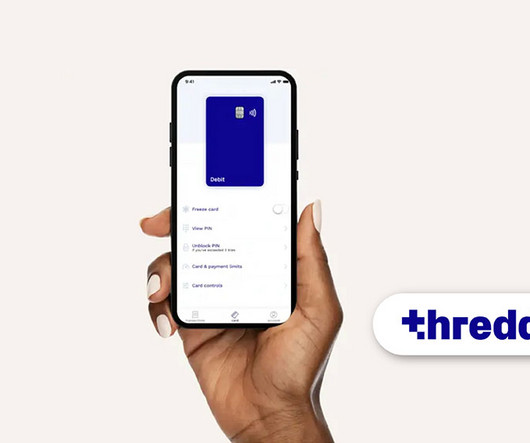

myTU , a fully automated, AI-native, and cloud-first digital bank, announced today the launch of Google Pay for its customers. This new feature enables both individuals and businesses to add their debit cards to Google Wallet, making payments more convenient and secure.

Credit cards are a staple in the wallets of consumers today, and they will undoubtedly be a payment method of choice for years to come, particularly as the adoption of mobile and contactlesspayments continues to grow. In fact, ResearchAndMarkets.com forecasts the global credit cardpayment market to grow to $762.16

As PYMNTS found in a recent consumer study, 40 percent of individuals are doing more of their daily retail and transactions online, partly because, well, there’s no other way to do it. Merchants, he said, “need to make sure they not only accept credit cards but also contactlesspayments.”. As Good noted, four in 10 U.S.

As digital wallets reshape finance and big tech challenges traditional banks, who will control the future of money? CEO Linda Yaccarino framed the move as a leap forward, but the real story is bigger: tech giants are no longer just facilitating payments, theyre actively reshaping the financial industry. What are digital wallets?

As 2024 draws to a close, it’s been an eventful year for the payments industry, marked by rapid innovation, unexpected challenges, and evolving consumer expectations. Experts at Aevi , the in-person payment orchestration firm, share their key takeaways, lessons learned, and perspectives on the trends shaping the future of paytech.

It’s a tale of a cultural shift, governments and innovators working in tandem, and millions leapfrogging traditional banking to embrace a mobile-first approach to finance. With global digital wallet payments projected to reach US$19.6 Here, smartphones aren’t just for calls and texts – they’re becoming the new face of money.

When Visa launched a contactlesspayments pilot with New York’s Mass Transit Authority (MTA) seven months ago, the company started small, and with modest goals. This “public pilot” made contactlesspayments available on a few train lines, and only at 16 stations, including Grand Central Station and Union Station.

That left FIs scrambling to “rapidly figure out how to get that same emotional and engagement outcome when the possibility of face-to-face is virtually nonexistent,” Randy Piatt , head of product solutions at card technology firm Ondot Systems , told PYMNTS in a recent conversation. Simple: Start with the cards.

After years of pushing to a fully digital payments landscape that will in theory see a cashless economy in the (reasonably) near future, it could all come tumbling down after a series of technical issues that has seen major retailers unable to process card or contactlesspayments and once again relying on notes and coins.

Fernando Souza , vice president at payments platform CyberSource , a Visa solution, told PYMNTS in a recent conversation that such fears have public transit systems around the world looking at moving to EMV contactlesspayments and away from cash, paper tickets and closed-loop, card-based systems.

The days of consumers at the local coffee shop or retailer queuing up the register, inserting cards and punching in PINs are likely in the rearview mirror. The rise of contactlesspayments is being driven by, and in turn is also driving a pivot away from, hardware – specifically the dedicated terminals at checkout – and toward SoftPOS.

Driven by COVID-19 fears and stampeding online, consumers overwhelmed many businesses in 2020 that were unprepared for drastic, sudden eCommerce volume. The COVID-19 pandemic has pushed more consumers to make their day-to-day transactions online. especially when it comes to enabling seamless payment experiences.”.

For SMBs, what’s in the cards … are more card readers. To that end, the banking giant J.P. Morgan is focused on enabling payments for the millions of small businesses that are the lifeblood of Main Streets across the U.S. – Morgan seems to be banking on speed as a selling point to gain traction with smaller firms.

In this 2024 report, we’ll explore how payment methods have evolved in the Canadian market, focusing particularly on the shift towards digital, contactlesspayments , and mobile along with other 2024 trends. Digital banks, sometimes called Neobanks, push consumers into digital banking and digital payments.

The COVID-19 pandemic has bolstered mobilepayments in India and primed them to overtake cardpayments in the not-too-distant, S&P Global Market Intelligence said this week in its 2020 India MobilePayments Market Report. Instead, they’re now seeking entirely contactlesspayments in a COVID-19 world.

The COVID-19 pandemic has bolstered mobilepayments in India and primed them to overtake cardpayments in the not-too-distant, S&P Global Market Intelligence said this week in its 2020 India MobilePayments Market Report. Instead, they’re now seeking entirely contactlesspayments in a COVID-19 world.

If there was a defining trend for payments in 2020, or a trend that gained the most traction compared to 2019, it was buy now, pay later (BNPL). Millennials have shown remarkable interest in these solutions, which allow consumers to finance purchases with specific terms when they check out online. Contactless.

Since the first plastic credit card was issued by American Express in 1959 , payment tech progress has been growing exponentially. Magnetic stripe payments enjoyed a 30-year reign between the ’70s and ’90s. EMV chip card technology had a good two decades or so, beginning in the mid-’90s.

While COVID-19 may be a driving force behind more members becoming accustomed to bankingonline and utilizing new solutions for transactions, it is expected that they will continue to operate in these new channels and with these new products moving forward,” said Denise Stevens, senior vice president, chief product officer at PSCU.

The CX must also be speedy and seamless, and for the merchants themselves, digital in a way that helps them make their own “money management” efforts more efficient as they digitize their own banking and accounting activities. The trend, after all, is toward contactless transactions. “It Looking Ahead.

Sure, activities like shopping online, getting food delivered, catching a cab or finding a gig are some of the most front-and-center examples. A study from Juniper Research found that mobile ticketing is becoming mainstream in sports, with users predicted to spend $23 billion via mobile in 2023, up from $14 billion in 2019.

For instance, Taylor said one of her bank’s clients runs regional bike shops that have seen business boom to such an extent that “they can’t keep the bikes or the equipment on the shelves.”. But she added that merchants are coming back online with business models that are somewhat different than what came before.

In today’s global economy in 2024, the financial transactions has evolved into a dynamic ecosystem, where a multitude of players work together to facilitate fast and secure payment processing. The payment processing ecosystem is vast and multifaceted, with a staggering array of statistics underscoring its significance.

Consumers around the globe have moved their purchasing online during the pandemic, and those in the Middle East and North Africa (MENA) region are no exception. The region’s financial institutions (FIs) and merchants have needed to work swiftly to support unprecedented levels of digital payment and shopping growth.

Brick-and-mortar branches shuttered as social distancing measures were enforced, and customers subsequently turned to mobile apps or websites to fulfill their banking needs rather than risking in-person visits. Online account openings have increased 14.5 Confronting Digital Banking Reality.

The banking industry is undergoing a sea change in the new decade, with online and mobilebanking growing ever more popular among customers, and challenger banks and FinTechs disrupt the market with new technologies. Developments From Around The World Of Digital-first Banking.

If Amazon can get you lower-debt payments or give you a bank account, you’ll buy more stuff on Amazon.”. Based on our findings, it’s hard to claim that Amazon is building the next-generation bank. This report is a collection of everything we know about Amazon’s foray into banking, financial services, and fintech.

And you can see it in the hustle by retailers and brands large and small to pivot their businesses and business models — and the disclaimers on just about every retail site starting a week or more ago that orders placed online might not make it in time for Christmas. One hundred and ten (110) million U.S. consumers — 47.2 percent of the U.S.

Some governments believe that contactlesspayments are a relatively safe alternative to cash and traditional credit cards because they spare merchants from handling bills and customers from tapping through POS interfaces. Irish consumers are also spending less, according to the Bank of Ireland.

As PYMNTS noted in the Pandenomics report in early October, “the biggest change of all will likely be the share of consumers shopping for groceries online. percent of consumers who have shifted to grocery shopping online plan to maintain at least some and possibly all of their new digital shopping habits, meaning only 14.7

Metro authorities in India are planning to launch automatic fare collection (AFC) gates that will work with the country’s National Common MobilityCard (NCMC) that was introduced in March by the Ministry of Finance , according to reports on Thursday (Jan. Right now, the smart card lets commuters skip the lines to buy metro tickets.

That’s when there is generally another point of frustration and friction: checking out after the dental work, perhaps giving over a paymentcard and signing up for another appointment. Omnichannel is a word that has been bouncing around payments and commerce for some 20 years. The credit goes to omnichannel.

In today’s top payments news, illegal activity involving cryptocurrency is at a record high, U.S. airlines are cancelling all flights to and from mainland China due to the coronavirus outbreak and Starbucks reported 17 percent mobile order growth in its Q1 2020 earnings report. BMO On Taking A Digital-First Approach To Retail Banking.

In regions where open banking and other electronic payments pilots are becoming common, such as the Middle East-North Africa (MENA) region, pandemic-era payments are all about privacy, security and trust, particularly in B2B transactions. Privacy Protection In The Spotlight. under the GDPR. under the GDPR.

In a year that saw the word "scamdemic" coined, scams such as authorised pushpayment fraud were top of mind, along with various other fraud schemes. This is not only the case for application fraud — where automation is used to create and submit hundreds if not thousands of applications — but also for card fraud. FICO Admin.

When you think about financial technology, it is easy to think about solutions which are making payments faster, easier and more accessible. Having already explored the biggest upcoming trends in the world of paytech, it is clear that progress in payments becomes drastically different depending on which region of the world you look at.

Some question whether the card-payment network operator will be able to overcome the struggle to “remain relevant” in a market that is quickly changing — and where consumers may soon be leaving card-based payments behind entirely. UnionPay is facing an increasingly competitive and complicated world these days.

From the wearables hype to the in-car payments fad, the past few years have seen many payment methods rise and many fall. The success of any specific payment method is strongly affected by macroeconomic factors, consumers’ perceptions, and technology. Take debit cards.

Apparently, a mixture of technical difficulties, tepid consumer interest and bank resistance has forced something of a stumble out of the gate for the team over at Apple. “We want to move as quickly as possible; we push it as quickly as possible.” According to figures, Apple Pay usage netted out at around $10.9

As infection and mortality rates rose and consumers became more concerned about their health and the health of others, it’s not hard to understand why their interest in contactlesspayments – tepid at best in a pre-pandemic world – skyrocketed overnight. PayPal’s Global Push. in August, and Pay in 3 in the U.K.

All of which are true, Byrne said, so long as one has pounds in their pocket – because many of the merchants in markets don’t take cards, and will politely direct customers to the nearest ATM when they try to pay with one. For a long time, the foundational problem for SMB and digital payments in the U.K.

As consumers become used to, and increasingly embrace, life lived digitally, financial institutions (FIs) of all sizes must prepare for seismic shifts in how customers access financial services, communicate with their FIs and make payments. Dusting Off What’s On The Shelf.

In the intricate landscape of payment processing, merchants encounter a myriad of options, each playing a pivotal role in the facilitation of financial transactions. The Definition of a Payment Processor A payment processor is a financial service provider that facilitates transactions between a seller (merchant) and a customer.

A statement that sounds like exactly what you’d expect to hear from the leader of the largest payments network in the world. Competition, Scharf believes, is what will keep every player in payments – large and small – focused on what’s really important – making payments the enabler for commerce in a variety of new end points.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content