This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

billion cash-and-stock deal for CardWorks, which offers unsecured creditcards among other products, places a high price tag on a traditionally risky product. Ally Financial's recently announced $2.65

Merchants with increasing transaction volumes often partner with creditcard processing solutions specializing in high-volume accounts to manage payments effectively while maintaining operational stability and customer satisfaction. What are high-volume merchant services?

market’s total transaction volume in 2023 was over $10 trillion, encompassing credit and debit card transactions as well as Automated Clearing House (ACH) payments. CreditCard Transaction Volume : Creditcard payments specifically accounted for around $5.6 Creditcards accounted for around $5.6

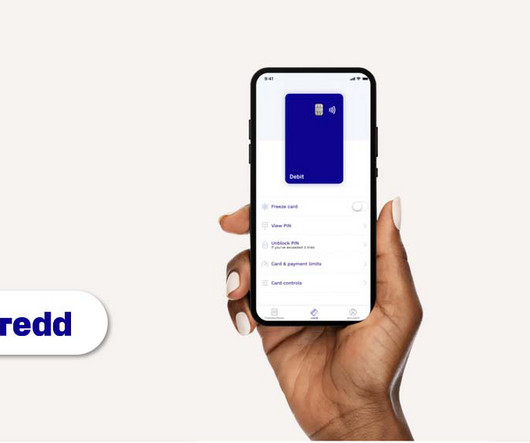

This move is part of Thredd ‘s efforts to strengthen its platform, products, and regional support for fintech firms and programme managers worldwide. Patricia Haynes joins as Senior Vice President of Platform, bringing her expertise in technology operations and riskmanagement from roles at Zopa and LexisNexis Risk Solutions.

While these technologies bring unparalleled convenience and global reach, they also introduce a plethora of risks that can impact the financial stability and reputation of businesses. Identifying and Assessing Risks Understanding the lay of the land is the first step in effective riskmanagement.

In this article, we’ll discuss what SaaS companies looking to become payment facilitators need to know about riskmanagement strategies. PayFacs handle risk assessment, underwriting, settling of funds, compliance, and chargebacks which exposes them to greater potential risks.

The cards, one general-purpose and one private label, will be issued by Synchrony and embedded within the OnePay app. Synchrony named exclusive issuer As part of the arrangement, Synchrony will serve as the exclusive issuer of OnePay creditcards at Walmart.

While online payments have taken off, many consumers still favour creditcards or cash for offline purchases. Notably, a greater share of respondents in metro China, compared to the rest of the Asia Pacific, view digital payments as more secure than creditcards.

Patricia previously served as VP of Technology Operations and Delivery at Zopa, where she led riskmanagement and process improvements, and Senior Director of Software Engineering at LexisNexis Risk Solutions, spearheading AML and compliance technology initiatives.

In a press release, the CFPB said the beta version of the tool encompasses the mortgage, creditcard, auto loan and student loan markets. This critical information will help us identify and act on trends that warn of another crisis or that show credit is too constricted.”.

Payment processors and acquiring banks employ this riskmanagement strategy to safeguard against potential losses associated with a merchant’s transactions. The post Merchant Account Reserves: A Strategic RiskManagement Tool for Banks appeared first on fi911blog. Why Do Acquirers Mandate Account Reserves?

Creditcard transactions have quickly become the lifeblood of eCommerce businesses and storefronts alike. According to Capital One, global creditcard transactions in 2022 reached an estimated 678 billion —an average of 1.86 However, accepting creditcards does come with a flipside; the ongoing sting of creditcard fees.

ID Analytics, a consumer riskmanagement company, announced Wednesday (Oct. 26) new research that revealed over six out of 10 millennials declined for credit are not seen applying again for at least 12 months. A frequently referenced Bankrate.com study reported that 63 percent of millennials do not have a creditcard.

For payment processors and financial institutions, however, understanding BINs is essential for smooth transaction processing, security, and even riskmanagement. A Bank Identification Number, or BIN, is the first six digits of a payment card number, such as a credit, debit, or prepaid card.

These APIs enable your users to accept creditcards, debit cards, ACH, and other payment options without ever leaving your platform. There’s no need to re-enter creditcard data for future purchases when using an integrated payment processing solution – this is true regardless of payment method.

Whether you’re running a small eCommerce shop or managing a high-risk industry venture, understanding merchant underwriting can help you navigate the approval process and maintain a strong partnership with your payment service provider. These tools can provide detailed insights into merchant behavior and risk levels.

The findings of a recent TD Bank survey suggest that targeting millennials for new creditcards will require surgical risk-management as the economy lurches toward an uneven recovery.

But it's not as unusual as my creditcard issuer might think, and that's part of the problem for prevailing identity management strategy. I don't normally buy $300 of pizza.

The rise of online transactions and evolving cybercrime tactics highlight the urgent need for strong identity riskmanagement and monitoring. Identity theft presents significant challenges to businesses, making proactive risk mitigation essential for regulatory compliance, trust, asset protection, and operational integrity.

Christensen will lead the company’s global acquiring and riskmanagement teams, working to grow and manage relationships with processors and banks, as well as overseeing the underwriting and risk functions. He brings 20 years of experience in financial risk, electronic payments and creditcards to the role.

Home Blog FICO UK CreditCards: Are "Established" Accounts in Trouble? The percentage of Established UK creditcard accounts with two missed payments is more than 83 percent higher than all account vintages. The percentage of Established UK creditcard accounts with three missed payments is nearly 94 percent higher.

Surfin began with consumer lending and has since expanded into various financial services, including payments, remittance, creditcard issuance, and wealth management. It has also launched Sufinc, a creditcard service in Mexico in partnership with Visa, which allows customers to make payments globally with no annual commission.

Subprime borrowers, who rely more on creditcards than any other group, are seeing their limits cut the most as banks reduce exposure during the coronavirus pandemic.

Go-to-market plans for international expansion Compliance and riskmanagement , especially in regulated industries Think of us as your outsourced payments strategy teamready to help you make confident decisions as your business evolves.

For much of the last decade, creditcard companies and issuers have fine-tuned security to the point where if any suspicious activity occurs on a cardholder account, that cardholder will receive an alert. That same sort of transaction and behavioral analytics is starting to come into other business sectors and walks of life.

The co-branded creditcard market is witnessing a meteoric rise. The surge is driven by the potential of co-branded creditcards to deliver innovative solutions, unlock new markets, and strengthen customer relationships. Are co-branded creditcards the next big opportunity for banks? Valued at $12.34

Among the biggest debates is how to construct and operate the best card program possible – a decision that served as the foundation for a new PYMNTS interview with Jim Geeslin, head of strategy for Elan Financial Services , an agent creditcard issuer.

While creditcards are the most preferred payment method for up to 40% of Americans , not all payment gateways support every type of creditcard. For example, most payment gateways accept payments from major creditcards like Visa and Mastercard, but only a small percentage accept Discover and American Express.

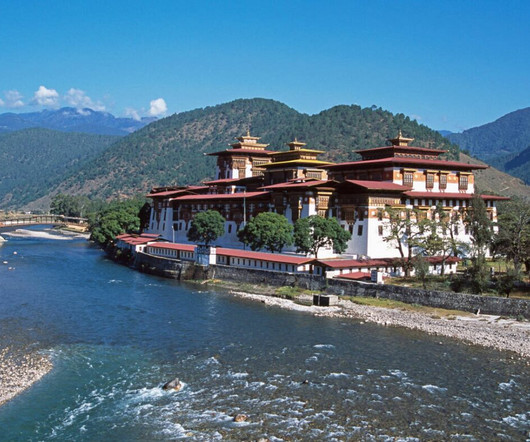

A handicrafts shop manager in Thimphu described the challenges posed by the lack of ATMs, creditcard authorisation systems, and other financial infrastructure catering to international customers.

Making a payment via the ACH network differs from making a payment with a creditcard in that you are sending the money directly from one account to another, instead of charging it to a card you would later be liable to repay. Learn More What are ACH Credit Payments? What are ACH Debit Payments?

“Implementing comprehensive riskmanagement strategies and diversifying technological dependencies are essential steps to mitigate the impact of unforeseen incidents, thereby maintaining the stability and reliability of payment systems. Where do you see it driving innovation?

The creditcard industry in India is booming. crore* creditcards in circulation, a substantial jump from 7.5 But only 5%** of the population has a formal creditcard. This is a huge opportunity for creditcard issuers. Currently, there are 8.5 crore just a year ago.

Shanghai Pudong Development Bank Issued More Than 9 Million New CreditCards Last Year Using FICO Originations. Shanghai Pudong Development Bank (SPDB) CreditCard Center, a creditcard lending pioneer in China, has increased its customer base using originations powered by technology from analytics software firm FICO.

Generational trends show younger users leading the adoption of digital wallets and stored creditcards, while older demographics continue to prefer traditional methods like bank transfers and debit cards, underscoring the need for inclusive payment solutions.

FICO’s latest market report of UK card trends suggests that consumers managed their creditcard debt to keep lines of credit open for the festive season as spend increased month on month. percent Clearly, November was a mixed story when it came to creditcard spend and debt management.

The imposition of restrictions four months prior stemmed from alleged non-compliance with OJK’s supervisory obligations , which include stringent requirements on riskmanagement and good corporate governance.

These requirements apply to any organization that processes, stores or transmits creditcard information. Installing and maintaining a firewall configuration to protect cardholder data. The banks are: Visa Mastercard Discover JCB American Express What are the PCI DSS requirements?

But the signs of financial pressure are also evident with an increase in average balances on accounts with missed payments and growth in card usage on cards – another sign of financial stress. Eight-year high for increasing spend on UK cards. The average spend on UK creditcards increased £23 to £711 in August 2021.

Bank Advanced Receivables brings together the bank’s leading payment and riskmanagement capabilities with Billtrust’s top AR technology to improve the intricate business-to-business (B2B) receivables process. Credit: The platform is designed for a more efficient way of extending credit to buyers.

Such touchless payment options are being used alongside traditional ones like creditcards and checks. Incidentally, there is no one-size-fits-all solution to tackling these risks, as one firm’s best practices may not be as effective for another’s operations.

The signs from our UK Credit Market Report for May suggest that consumers are practicing pragmatic financial management, as well as continuing to make use of savings accrued during the pandemic. There are, however, warning signs in our UK creditcard data of the financial pressure growing for those already in debt.

Our monthly UK Credit Market Report analyzing UK creditcard trends for September 2021 shows the contrasting conditions that have been seen throughout 2021 continue. UK Card average spend falls for third time in 2021. The average spend on UK creditcards in September 2021 decreased £3 to £708. Looking ahead.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content