This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Banks commonly rely instead on outdated authentication methods like PINs, passwords, and repetitive verification steps, for even the simplest transactions. The disconnect between everyday smartphone verification and banking authentication is becoming harder to justify as payment technology and regulation advance.

Banks turned to a powerful ally: artificial intelligence. AI didn’t just automate services—it began shaping intimate, context-aware journeys that feel less like banking and more like a personal concierge for your financial life. Banks around the world rolled out AI-powered personalization features in 2024. The result?

TL;DR Online payments rely on API or hosted gateways with encryption and fraud detection, while in-store transactions require POS hardware with EMV chip technology and NFC capabilities. The issuing bank verifies whether the customer has enough funds in their account to complete the transaction.

These services enable you to process credit card payments online, in person, and on the go, and include everything from secure payment gateways to merchant accounts and point of sale (POS) systems. Interchange fees are the base fees charged by card-issuing banks to process a transaction.

This enables rapid scaling of new payment use cases, without duplicating risk exposure. The traditional PAN is steadily becoming obsolete, a trend reflected in the growing use of numberless cards and online tools such as click to pay, which enables one-click transactions without requiring card details. .

Card issuers need for speed exists on several levels, and we at OpenWay see this firsthand, since our Way4 card management software is used by top banks, processors and fintechs around the world. This can be an account opened in Way4 or in the integrated Core Banking System. Indeed, rapid product development remains a top priority.

A payment gateway processes credit card payments for both online and in-person transactions. It collects payment data, secures sensitive information, and connects all parties needed to move money from your customer’s bank to yours. For online retailers, this entire sequence must complete flawlessly during checkout.

In a statement, the company noted that these options work across all purchasing channels, whether online, in-store, or via sales teams. SBSN empowers banks to expand their offerings to small businesses by enabling them to access the small business B2B trade credit market. March has been a busy month for TreviPay.

Automatic data syncing also reduces duplication and AR errors. Your provider may ask you to download a package and run an installer or set up online credentials, so following their instructions is essential. and ACH/eChecks for direct bank transfers. Sage integrations may also support mobile and remote payment processing.

Providing a range of payment methods like credit and debit cards, ACH/eChecks, online payments, and more can promote more timely payments, enhance convenience, and increase customer satisfaction. Offer flexible payment options Offering flexible payment options can significantly improve the customers invoicing and billing experience.

These merchant services are especially beneficial if a company has significant transaction volume, as they address the unique challenges of managing high-risk merchant accounts, handling mobile credit card processing, and navigating complex transaction fees.

The plastic card, by necessity, is giving way to digital cards, and mobile apps are bringing card-not-present transactions, increasingly, to mobile devices. She noted that mobile app use is up double-digit percentages as of April, when the pandemic shifted so much of everyday life online.

Similarly, the continued steady global increase in the use of mobile devices helped fuel the development and release of new tools to security companies, as well as access to richer, deeper user data. Mobile security on the move. But mobile devices offer more than just biometric protection. ” Biometrics coming on big.

Online fraud has become a massive issue, so it’s important to be aware of the impact on consumers as well. For instance, online shopping scams in the U.K. Remember to use a unique password for each of your accounts, particularly important ones — not just bank and brokerage accounts, but PayPal, Gmail and Amazon, everything!

Buying items online has become a regular everyday occurrence. While Pew Research shows 79 percent of Americans shop online, it also found that 82 percent place a high value on factoring reviews into their purchasing decisions. RS: WeGoLook is a mobile technology company that’s changing the way the world works.

Consumers want omnichannel banking access so they can easily switch between in-person branch visits, call center services and mobile apps as needed. They might pop into bank branches near their offices to grab cash, for example, then use mobile apps during their subway rides home to check their account activity.

How can banks deliver unified experiences across multiple channels, with the right amount of friction, to navigate the fine line between fraud reduction and customer experience? To offer customers faster and better originations processes, banks need to automate more – without increasing risk.

TL;DR Payment tokenization (sometimes referred to as credit or debit card tokenization) involves taking sensitive information, such as credit card data or bank account numbers, and protecting it by replacing it with a token. With tokenization, its possible to use mobile wallets to store card information.

No one likes being charged more than once for a transaction — one of the vagaries of living in a technology-fueled world — especially when it comes to commerce and banking. Customers can continue to access their accounts and services via our onlinebanking, mobile app, branches and ATMs.”.

I recently spoke with FICO’s Adam Davies about c ontextual intelligence , a new approach that banks, other financial institutions and telecommunications companies are embracing to prevent fraud and financial crimes. As an example, let’s look at the use of the mobile phone as a verification variable. Adam: Exactly!

But the conversation that needs to happen, said Frank, is one that must consider that “when you look at credit card innovation, it’s not driven by the banks … but by the core processors” such as FIS and Fiserv. A dashboard helps create separate card numbers and one-time-use numbers or merchant-specific ones.

Or mobile wallet payment solutions like Google Pay and Apple Pay. Once the client sets up a payment profile with their banking information, the payment can be automated and paperless. The Federal Trade Commission offers straightforward advice: “don’t give out your bank account number.”

Accounts payable software like Xero are similar to Quickbooks online, and are suited for small businesses. Flow Core competency : end-to-end automated AP management - import, approve and pay invoices in the same platform. It targets mid-sized and large companies and has a price range comparable to Oracle.

Complex approval workflows, duplicate alerts and fraud detection Payment and reconciliation that works like magic. Integration with NetSuite, Quickbooks Online, Xero, and Sage Intacct, Integration with Slack, allowing employees to receive alerts, handle requests, and obtain approvals directly within the Slack interface.

Some popular choices include QuickBooks Online, Hiver, Wave, Kashoo, Bill.com, and Xero. These software solutions offer a range of features that can benefit small businesses, such as automated bill payment, customizable payment reminders, bank integrations, and multi-step approval workflows.

The payment process using ACH transfers involves the payee creating a payment order which is received by the originator bank. The originator bank compiles all the POs and sends them to an ACH for processing. The ACH operator then approves and releases the PO amount to the recipient bank.

The World Bank reports that two-thirds of adults worldwide make or receive a digital payment today, with the share in developing economies growing from 35% in 2014 to 57% in 2021. Bank transfers and digital wallets are more recent developments that have leveraged the rapid expansion in digital data and interconnectivity.

Last week I received new credit cards from US Bank and Capital One, both containing microchips to support EMV terminals, the global standard finally rolling out in the United States over the next few years. US Bank , on the other hand, took a less-comprehensive approach with the mailer, but delivered much more on its website.

Merchants operating in EU markets must ensure that customer-facing platforms, including e-commerce websites, mobile apps, payment terminals, and support channels, are accessible to users with disabilities. The historical assumption that compliance sits solely with banks, acquirers, or payment service providers is no longer tenable.

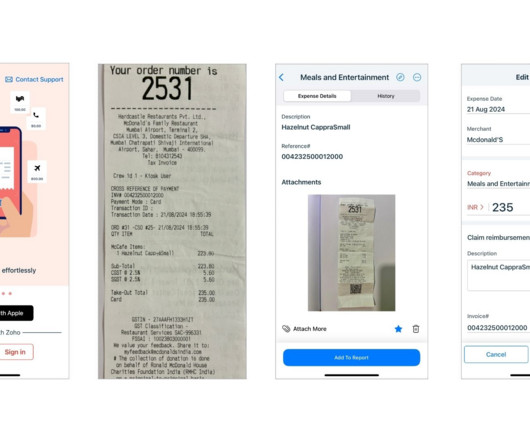

Duplicate Claims Employees submitting the same expense for reimbursement more than once. Lack of Mobile Solutions In today’s digital age, the absence of mobile-friendly solutions for expense submission and tracking can be a significant drawback. For online subscriptions, e-receipts or invoice copies are required.

QuickBooks Online Source QuickBooks Online is a cloud-based accounting software that's become a popular choice among many small to medium-sized businesses. Here’s what customers say about Nanonets. on Capterra and G2. Try Nanonets today. Start your free trial without any credit card details.

Payment portals NetSuite’s payment portal enables businesses to offer a self-service experience where clients can view their billing history, update payment information, and make payments online. Solupay: Solupay is another payment processor that supports credit card processing, ACH payments, and mobile payment solutions.

14-day free trial Quickbooks Online Quickbooks users Android , iOS 3.9 Here are our two best picks: Dext Prepare Receipt App Dext Prepare (formerly known as Receipt Bank) is a robust receipt scanner app that simplifies bookkeeping with advanced features including receipt scanning, expenditure reporting, and analytics.

Regardless of the company, its industry, its customers or location, online fraud remains top of mind. In an interview with PYMNTS, Bradley Wiskirchen, CEO of fraud protection tech firm Kount, detailed the landscape of online fraud, where it is going, and the challenges and opportunities that confront innovative fraud detection.

Invoice distribution: Invoices can then be issued to customers through online portals, email, or other preferred delivery methods without any manual process. Payment processing: Once a customer makes a payment – through credit cards, online portals, or bank transfers – the system processes and records the payments.

Acting as a centralized platform, it retrieves data from the general ledger and compares it with bank statements and invoices, facilitating accurate and swift account reconciliation. Compatible with both Windows and Mac computers, Xero also offers a mobile app for Apple iOS and Google Android devices. Sources: [link] [link] 2.

For online subscriptions, e-receipts or invoice copies are required. Customization to Business Needs: Given TechWave's focus on technology, a higher budget is allocated for software and online tools. The software integrates with accounting systems, allowing for direct processing of reimbursements through payroll or bank transfers.

Typically, credit card reconciliation begins with the collection of credit card statements from various sources, such as banks or financial institutions. Cons: Limited customization options, occasional syncing issues with bank accounts. QuickBooks Online Key Features: Online accounting, expense tracking, bank reconciliation.

This in turn helps build a false identity associated with a mobile number. These are then used to defraud multiple banks with fraudulent accounts, credit cards, and loans. Here are five other ways crooks use subscription fraud to commit crimes against customers and service providers, with advice on how to stop them.

InnovateX used the OCR-based mobile app offered by their expense management software for expense reporting which captures data directly from receipts and populates the same in the expense management system. And with mobile apps, expenses can be managed on the go - from the backseat of a cab or the departure lounge of an airport.

Verify bank accounts Automate approvals Instant vendor notifications Check against blacklists OCR and Machine Learning AI & OCR Technology in AP Automation At the start of the invoice management cycle, documents must be scanned so the data can be captured and entered into the system. Is your business mobile?

Complex approval workflows, duplicate alerts and fraud detection Payment and reconciliation that works like magic. Integration with NetSuite, Quickbooks Online, Xero, and Sage Intacct, Integration with Slack, allowing employees to receive alerts, handle requests, and obtain approvals directly within the Slack interface.

Using AI, every transaction is kept secure through duplication detection, fraud prevention, and payment tracking features. Since 1-click approvals from your mobile phone, email account, or Slack profile are enabled, doing business from anywhere has never been easier. Pros Melio can be used for free to send payments to vendors.

Starter ($49/user/month or $199/month for 5+ users): Processes up to 30 invoices/month - Includes vendor management, standard ERP sync, payment via bank transfer or credit card - Supports up to 10 users 2. Mobile app: Manage expenses, book travel, and submit receipts on the go with Navan's user-friendly mobile app.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content