This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

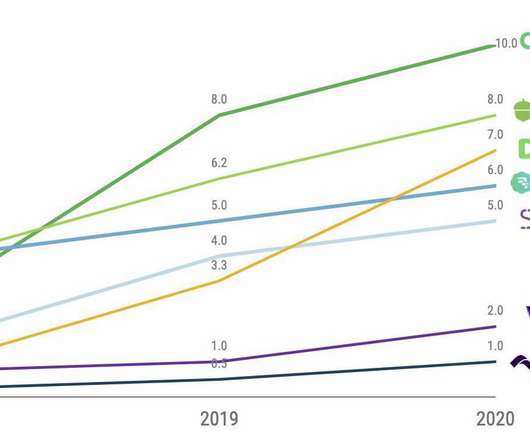

billion Bolttech, launched in 2020, combines innovative technology with insurance expertise to partner with top insurers and businesses worldwide. It provides access to game credits, gift codes, and vouchers using familiar local payment methods such as mobile carrier billing and e-wallets. bolttech Valuation: $2.1 Coda Valuation: $2.5

This market includes a range of services and technologies that facilitate the acceptance, authorization, and settlement of payments across various channels, including online, in-store, and mobile. They require secure systems like point-of-sale (POS) terminals , online checkout gateways, or mobile payment solutions to process payments.

Indigenous Banking (Shroffs and Mahajans): Long before modern banks, India had a thriving indigenous banking system. These banks introduced formal ledger-based accounting and cheque payments. This expanded the reach of formal banking to rural areas. This introduced standardization and divisibility.

Both power a substantial share of online commerce, yet they’ve taken different paths to the top. In other words, Adyen is the rare fintech operating at bank-like profit levels, while Stripe proved its business model can scale financially. Stripe launched in 2010 , targeting developers and small online businesses with easy-to-use APIs.

Digital-First Banking. Banks will need to seriously revamp their in-branch experiences to accommodate the new normal as customers are growing used to the unparalleled convenience and speed that mobilebanking has to offer. The year-over-year increase in cross-border online sales was even more dramatic in other regions.

Are digital first banks in Asia poised to lead a disruptive charge against well-entrenched, established commercial banks? In the traditional banking sphere globally, but especially true in Asia, there is a considerable proportion of unbanked and underbanked populations who lack complete or any access to banking services.

In the last five years, Sri Lanka’s economy has struggled greatly. Not all doom and gloom: fintech is on the horizon Despite the outbreak of the pandemic, in 2020 the Central Bank of Sri Lanka (CBSL) launched its regulatory sandbox in an effort to boost its fintech sector and innovation.

of India (NPCI) that facilitates inter-bank transactions, has propelled the growth of online payments, the Financial Times (FT) reported. UPI was established by the central bank and is owned by a group of local lenders. billion, bringing bank accounts to hundreds of millions of residents for the first time.

The ownership economy is going full throttle. Lest you think the change has been all about streaming media, about home delivery of meals and meal kits, of staying in … AutoNation’s results herald a pivot toward an age of personal mobility. The Individual Mobility Shift . They want a place to go to complete the transaction.”.

Over the past 75 years, South Korea’s economy has boomed, undergoing rapid industrialisation with a growth rate of seven per cent annually, according to the International Monetary Fund. Having earned its spot as one of the Four Asian Tigers, we explore what is propelling South Korea’s economy and fintech ecosystem.

The COVID-19 pandemic has reshaped industries and economies worldwide. in 2020, reaching $4.28 Cash Usage Decline : The World Bank reported that cash usage in advanced economies declined by nearly 50% during the pandemic, with consumers opting for digital and contactless payment methods instead. billion in 2019.

But she added that merchants are coming back online with business models that are somewhat different than what came before. They may want to order online and pick up curbside. SMBs can accommodate that with a host of methods: mobile wallets, contactless cards, QR codes, paying in-store via a mobile app, etc.

The meteoric ascent of Brazilian neobank Nubank has sent shockwaves through the Latin American banking industry. As digital banks in the Asia Pacific (APAC) region aim to replicate this success, there are valuable lessons to be learned from the unconventional Nubank approach to banking.

economy hard, but few areas were hit harder than small businesses. In spite of their small size, they play a critical role in both their local and national economies. economy when everything is really clicking — which it hasn’t been for the last several months,” he said. “On COVID-19 has hit the U.S. The Bumpy Road Ahead.

As businesses and consumers become more comfortable using credit cards online, the proportion of US commerce that takes place online has steadily increased over the last 20 years. Specifically, the Collisons aimed to more seamlessly connect online businesses and payment processors, allowing more businesses to accept online payments.

The COVID-19 pandemic has prompted traditional banks to take fresh looks at their digital initiatives and has given digital-only banks the opportunity to learn about the advantages and hurdles of serving customers primarily through online and mobile channels. Building Trust Between Banks and Consumers Online.

In the past few years, the burgeoning popularity of digital banks has only underscored the severity of these problems, with upstarts like Chime and SoFi offering cheaper, faster, and more convenient banking experiences. . get the state of challenger banks report. First name. First name. Company Name. Phone number. Source: PwC.

Confronted by shifting factors such as tech advancements, generative AI, high interest rates, increased institutional oversight, and evolving customer expectations — the best banks must adapt their business and operating models in 2024, including in Asia. CHINA #1 China Merchants Bank China Merchants Bank Co.,

The prospect of restarting the economy of bringing all manner of everyday life in the U.S. back to some semblance of “normal” has challenges — and opportunities for banks, especially community banks and credit unions. Call it a way to be physical even while being virtual. Reinventing The ATM.

Scott noted that fewer credit union mergers happened in 2020, largely due to the pandemic. But he said the pandemic is “a catalyst for accelerating digital offerings” — and for transforming the very nature of in-person banking, even though boosting brick-and-mortar efforts might seem counterintuitive in the pandemic’s wake.

Summary of Statistics in this Article In the United States, contactless payments accounted for 34% of all debit card transactions in 2023, a significant increase from 19% in 2020. According to Visa, tokenized transactions accounted for 85% of all mobile debit transactions in North America in 2023.

To bring digital transformation to banks, and to help them bring their assets to the “digital-first” consumer, look to the platform. That’s a challenge, as banks have traditionally plied their trade through face-to-face interactions. It’s really about extending out the capability of your card to the commerce ecosystem,” he said.

The government ban happened when Lagos, the government hub of Africa’s largest economy, banned motorbike passenger service in January, according to director of marketing Osagie Alonge , Bloomberg reported. OPay was formed a year earlier than that, in 2018, as a way for mobile customers to send and receive money.

The COVID-19 pandemic has bolstered mobile payments in India and primed them to overtake card payments in the not-too-distant, S&P Global Market Intelligence said this week in its 2020 India Mobile Payments Market Report. But S&P found that there’s an awful lot of ground left for mobile payments to capture.

The COVID-19 pandemic has bolstered mobile payments in India and primed them to overtake card payments in the not-too-distant, S&P Global Market Intelligence said this week in its 2020 India Mobile Payments Market Report. But S&P found that there’s an awful lot of ground left for mobile payments to capture.

Since the rise of M-Pesa in 2007, mobile money wallets have become prevalent across Africa. And while that addition to the market has made many things possible for consumers in formerly cash-locked economies, there has been a persistent problem of limitations for users once they want to transact outside their home environment.

Mobile card apps went from nifty to necessary when the darkest imaginings of last March had people picturing COVID-19 on every surface, suspended in every breath. PYMNTS’ July 2020 Building a Better App Playbook , done in collaboration with Ondot , focuses on the rise of credit and debit usage amid the pandemic’s backdrop. percent.

Shorten the timeframe a bit, and it gets (just a bit) easier to see what may be rushing toward us – or what we may be rushing toward — in terms of innovation in-store, online and across all manner of channels. In fact, a time capsule sealed today, with a prediction of what Dec.

The ongoing pandemic has pushed more consumers online to carry out their shopping and banking, with fraudsters following suit. Bad actors have moved to take advantage of the rush to digital payments — particularly those made with debit cards — leaving banks and financial institutions (FIs) racing to keep them off their platforms.

Payments giant Mastercard has launched its new ‘Open Banking for Account Opening’ programme for select US debit and prepaid products, hoping to streamline and secure account opening. In a recent study, Insider Intelligence found that Gen Z mobilebanking adoption continues to rise by 12.4 million in 2020 to 47.8

Open banking has been picking up steam in Latin America for more than two years. Brazilian lawmakers have been developing open banking plans since 2019, for example, outlining rough guidelines to be enacted late this year. It also analyzes how the pandemic is affecting the future of open banking in. the region.

The PYMNTS/Visa How We Will Pay Study; 2020 Edition tells us that home is no longer merely where the heart is. Habits are hard things to change, but 2020 has been a year that has seen consumers unusually receptive to not only experimenting with new ways to transact, but to actually modifying the day-in, day-out details of how they live.

Financial Hub Casablanca (Ranked globally 56th) Key Economic Development Strategy Maroc Digital 2020 Economic, financial services and fintech overview: According to the 2017 World Bank s Global Findex Report, only 29 per cent of adults had a bank account.

Today Mastercard announced the Open Banking for Account Opening program, providing a foundational set of open banking products as a core benefit to Mastercard consumer and small business debit issuers as well as consumer prepaid issuers in the U.S. million in 2020 to hit 47.8 year over year, from 20.7 million by 2026.

QR codes had made some inroads here and there, and yet did not become the go-to repositories of data and information – scannable, naturally, across mobile devices – that some had predicted. The QR code is shorthand for the “quick response” barcode that was first designed in 1994, and which initially surfaced in Japan.

De Abreu highlighted these prospects in a recent interview with Fintech News Singapore, emphasizing the growing importance of emerging markets, including LatAm and Africa, for the global gaming industry, fueled by rising smartphone penetration, increasing digital payments and the booming popularity of mobile gaming.

Removing that friction with experiences that enable customers to avoid age-old annoyances and homeowners to make extra income is intriguing to members of the sharing economy, according to Tim Wootton, CEO of shared parking marketplace Rover Parking. Keeping pace with parking payments and innovation.

And you can see it in the hustle by retailers and brands large and small to pivot their businesses and business models — and the disclaimers on just about every retail site starting a week or more ago that orders placed online might not make it in time for Christmas. 23-25, 2020. Take PayPal, for example. percent of all retail sales.

Cambodia is leveraging fintech innovations and strategic reforms to boost economic growth, financial inclusion and international partnerships, positioning itself as a key player in the Southeast Asian digital economy. Cambodia’s economy is projected to grow by 5.8 Cambodia has also ventured into central bank digital currencies (CBDCs).

In late June, the Monetary Authority of Singapore (MAS) sent a ripple through the global financial services ecosystem with the announcement of its intention to issue five digital bank licenses to eligible applicants. Oversea-Chinese Banking Corp. and United Overseas Bank Ltd. billion ($1.1 Grab + Singtel .

The role of trust in the digital economy has become more visible and important, and it’s pretty much a given that few online or mobile-focused companies will scale and succeed without winning the trust of consumers and other participants in their specific ecosystems. The Role Of Trust.

The year’s third quarter is over, so it’s prime time to check into the economy. Part of that effort, of course, includes examining the state of the foundation of the economy: small businesses. 15% of SMEs get rejected for a bank loan in Canada , found the CFIB in a new report.

The first quarter of 2020 should have been business as usual — especially for the payments processors and financial services technology companies — the firms that keep commerce humming across offline and online channels. Merchants, too, enjoyed the tailwinds of a strong economy and sanguine consumer mindset. Setting The Stage.

It also provides another sign that that cash is, generally at least, slowly losing its dominance as a payment method in all types of economies. Mobile Fuel. Launched in India in 2017, PayPal has formed partnerships with local online merchants such as BookMyShow, MakeMyTrip, Yatra, Goibibo, FreshMenu and Box8. That’s not all.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content