This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Credit data Average FICO scores rose from 688 in 2011 to 718 in 2023, suggesting that those already in the system were improving their credit profiles. But the people who needed help the most — those outside the traditional credit model — weren’t lifted by that rising tide. It’s a portfolio loss.

According to the 2022 Bhutan Living Standards Survey Report, 95 per cent of households own a smartphone, 99.6 Despite its historical lag in technology adoption, recent years have seen significant government efforts to expand ICT and telecommunications infrastructure.

CreditRisk and FICO Score Trends? creditrisk and FICO® Score trends. At the same time, increasing adoption of recent innovations in credit scoring solutions should benefit consumers, leading to greater consumer empowerment opportunities and credit access.

In 2022 consumers will increasingly expect to be able to service all of their requirements, however complex, online. As economic activity rebounds, people are facing elevated levels of inflation with potential increases in interest rates forecast in early 2022, as well as higher energy prices.

Another full year is in the books As 2022 came to a close, the economic environment in the United States is teetering on the edge of a recession. Inflation is easing as funding rates have risen to 15-year highs, but the technology sector is beginning to lay off employees in masses – through 2022 low levels of unemployment kept the U.S.

Both industry and government regulatory bodies, along with investors, are intensively examining the risk management strategies and protocols of enterprises. Across various sectors, boards of directors are increasingly mandated to assess and disclose the effectiveness of risk management processes within their respective organizations.

Covid to Cost-of-Living: Assessing Affordability in Uncertain Times. Wed, 08/10/2022 - 11:55. Affordability Assessments and Unrestrained Lending. But a crucial challenge to existing affordability assessments has been the huge spike in ‘buy now, pay later’ loans (BNPL). The Future of Informed Affordability Assessments.

6 Digital Transformation Trends Highlighted at FICO World 2022. Wed, 06/22/2022 - 12:30. Innovation in digital transformation and emerging trends were firmly front-of-mind this year at FICO World 2022. Over the longer term, ESG and climate risk evaluations may become an integral element of creditrisk and the automation process.

Home Blog FICO Top 5 Scores Posts of 2022: Steady FICO Score, BNPL and Alternative Data 2022 marked the first year in over a decade the average FICO Score did not increase, while the industry’s attention remained on topics such as alternative data and BNPL. million previously “unscorable” consumer files.

There is also evidence in the US that BNPL users tend to have a riskier credit profile than those of traditional consumer credit products. The BNPL platform then assesses their creditworthiness through a soft credit check. Adjusted operating margin stood at 12% during the period compared to -5% during Q3 2022.

Using remote sensing technologies on farmland, the bank assessescreditrisk based on crop growth and various factors. This approach ensures that even farmers in remote areas can access credit. Within a short period, it quickly gained over 500,000 customers, with a focus on helping customers save on everyday spending.

Home Blog FICO Top 5 Customer Development Posts of 2022: Digital Banking and Pricing Opti The most popular posts in our Customer Development category dealt with digital banking, optimizing credit line increases, loan pricing and machine learning for creditrisk models.

Fri, 06/03/2022 - 12:24. Thu, 10/20/2022 - 15:00. How can lenders build, manage, and secure credit portfolios in today’s uncertain market environment? A panel of creditrisk experts discussed this question at length during a FICO® World 2022 session entitled “Resilient Credit Lifecycle Strategies are the New Norm.” .

Fri, 06/03/2022 - 12:24. Thu, 10/20/2022 - 15:00. How can lenders build, manage, and secure credit portfolios in today’s uncertain market environment? A panel of creditrisk experts discussed this question at length during a FICO® World 2022 session entitled “Resilient Credit Lifecycle Strategies are the New Norm.” .

In October 2022 , the FHFA validated and approved FICO® Score 10 T for use by Fannie Mae and Freddie Mac, two government-sponsored enterprises that guarantee most of the mortgages in the US. The updated model reflects the evolving credit landscape and credit behavior to help better inform a higher level of consumer creditrisk prediction.

Even in the most favourable economic conditions, borrowers with low credit scores have historically been more likely to fall behind on their payments for car loans, personal loans, and credit cards. Without proper filtering, lenders run the risk of approving high-risk borrowers, which can lead to increased loan defaults and losses.

How Merchant Fees Are Made Up The unavoidable basics of credit card processing fees are interchange rates and assessment fees. Interchange Fees Although interchange fees go toward paying the issuing banks, the major credit card networks — Visa, Mastercard, and the likes — control the interchange rates.

And while some of our clients’ business lines benefit from the very latest innovations, others such as mortgage continue to find that older versions of the FICO® Score – even some that were first developed decades ago – meet their needs for creditriskassessment. That’s because FICO® Scores are built to last. Ethan has a B.S.

The company demoed one of its solutions, UnBias , at FinovateFall 2022, and won a Best of Show award for its presentation. Among the company’s other solutions are CreditRiskAssessment and Fraud Detection.

Tue, 07/19/2022 - 16:11. Mon, 10/10/2022 - 15:00. We all know that having a higher credit score helps a consumer gain access to credit and get better terms from a lender. A low FICO score for a consumer can have the perverse effect of preventing them from having access to a second chance through manual underwriting.

Saudi Credit Bureau Delivers Access To Loans For Millions with Score. Fri, 09/09/2022 - 03:42. Thu, 09/15/2022 - 06:00. We have been on a journey in Saudi since 2011, to grow lending and increase financial inclusion through the adoption of advanced riskassessment tools,” said Swaied Alzahrani, CEO of SIMAH.

The FICO® Score is the lingua franca, or common language, for the credit scoring industry. It serves as a broad-based, independent standard measure of creditrisk. The FICO® Score model is based on data in an individual’s credit report, housed by the three primary U.S. CRAs offering free weekly credit reports to all U.S.

14% said the financial outlook for their company was very strong, and another 50% assessed the outlook as strong. Just over 40% of respondents said that volatility in the securitization market in 2023 would be higher than 2022, and another 36% believe it will be about the same. Leading Secondary Market Participants Weigh In

How data sharing can improve creditrisk decisioning. Mon, 10/17/2022 - 07:00. . The launch of the Open Finance Framework by Bangko Sentral ng Pilipinas (BSP) in 2021 was a big step forward in driving financial inclusion for millions of Filipinos across the market who still do not have access to credit. FICO Admin.

In 2022, data showed that bank customers still frequently utilised branches for various services. High mortgage rates and inflation pose a risk of stressed customers defaulting on their mortgages, potentially causing government interventions.

.” Empower was founded in 2016 and uses its technology to underwrite consumers using real-time cash flow, other nontraditional data, and machine learning to assesscreditrisk. The company offers lines of credit, which are issued by FinWise Bank, and no-interest cash advances.

Mon, 07/18/2022 - 18:40. FICO® Score models, developed using advanced computational methods, including insights from ML, are designed to provide lenders with explainable reason codes to share with consumers for their credit decisions. . The use of Machine Learning must be balanced with deep domain expertise in creditrisk modeling.

billion in 2022 to over $250 billion by 2032, fueled by the relentless pace of digital transactions. billion in 2022 to $252.7 Experian ( www.experian.com ): Offers creditriskassessment tools and fraud detection services, leveraging extensive consumer and business data.

Em Conversa looks to uncover what the future of fintech could look like in the region, following a $2.1billion valuation in 2022. Since 2022, a lot has changed so we decided to revisit some of our earliest features to see to what extent the market has stayed the same and how much it has evolved.

Finding a way to score millions without credit history. Círculo de Crédito , the fastest-growing credit bureau in Mexico, has used unique creditrisk scores from FICO to boost financial inclusion in Mexico and help an additional 20 million citizens access credit.

FICO ® Resilience Index (FRI) augments the FICO Score with an additional dimension of creditrisk insight. Wed, 08/03/2022 - 15:35. In addition, homeowners are beginning to struggle to pay their mortgages, with foreclosure filings increasing by 153% in the first six months of 2022 compared to the same period last year.

According to Polaris Market Research , the global BNPL market is projected to expand from $6.24billion in 2022 to $80.52billion by 2032. “Aside from a competitive market creating pressure on terms and expensive customer acquisition, there is a major risk management challenge.

If you are a Risk Manager, you should be reviewing lending strategies to ensure customers are receiving the right treatment across the lifecycle and getting the help that is needed if debts cannot be fulfilled. Leanne Marshall Leanne Marshall is a Senior Strategy Consultant with FICO Advisors for North American CreditRisk Lifecycle Practice.

Other expenditure blind spots, such as Buy Now Pay Later, can be removed through the use of digital income and expenditure assessments or Open Banking data. The value of emerging, non-traditional data sources should not be overlooked.

Trust acquired 100,000 customers in just ten days after it launched in September 2022 and exceeded 450,000, equivalent to 9 percent of the Singapore market, within just five months. We combine risk management fundamentals with data science and customer segmentation to help us arrive at optimum risk outcomes,” said Lohia. “We

Plenty still have siloed data across marketing, creditrisk, customer management, fraud, compliance, and collections operations. Importantly, when assessing whether a product represents fair value, market rates and prices for comparable products can be considered. Peter Lemon. See all Posts. chevron_left Blog Home.

Wed, 11/30/2022 - 16:00. Graph 1 : Quarterly credit card debt in the United States from 1st quarter 2010 to 2nd quarter 2022 ($ Billion) . Further complicating a fair assessment was government sponsored stimulus packages, which veiled factual customer affordability. FICO Admin. Thu, 08/22/2019 - 12:37. by Cyril Cherian.

Fri, 09/30/2022 - 15:00. For example, drivers who consistently brake harshly, accelerate excessively, drive over the speed limit and use their phones while driving present a higher risk of future traffic collisions and will therefore receive a lower score. . FICO Admin. Tue, 07/02/2019 - 20:36. by Can Arkali. expand_less Back To Top.

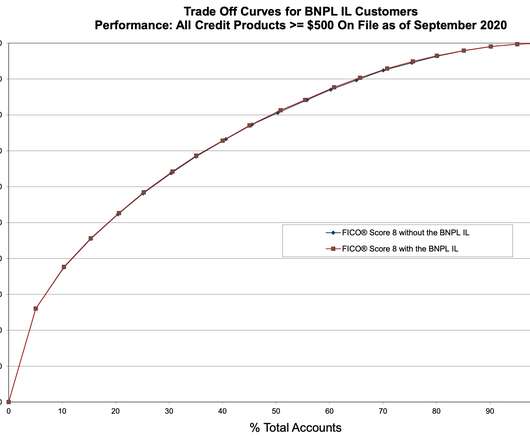

Key findings from FICO research on consumer credit files with recently opened Buy Now, Pay Later loans. Mon, 06/20/2022 - 15:00. market: BNPL reporting approach: How a BNPL lender reports these accounts to a credit bureau can materially influence the impact these loans ultimately have on the FICO® Score. Tue, 03/23/2021 - 22:16.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content