This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

When young Russians apply for their first creditcard at Sovcombank, they go through a fun, interactive survey that starts with the question, “How do you feel today?” What they’re doing is participating in a new type of psychometric credit scoring that could expand credit in markets worldwide.

Accepting creditcard transactions is no longer a decision of whether to but rather how to. With cashless now BEING king, credit and debit cards are the primary method for your customers to make payments. of consumer payments came through card payments. Card Network (e.g., Pre-pandemic, 62.3%

Which works better for modeling creditrisk: traditional scorecards or artificial intelligence and machine learning? Take, for example, our new credit decisioning solution, FICO Origination Manager Essentials – Small Business. It’s designed to help lenders make faster origination decisions without increasing risk.

A handicrafts shop manager in Thimphu described the challenges posed by the lack of ATMs, creditcard authorisation systems, and other financial infrastructure catering to international customers.

LexisNexis Risk Solution, a data and analytics company that helps loaners assess the risk of small business lending to borrowers, is teaming up with Cortera to add its trade credit analytics capabilities into the mix. ”

The deal will help Empower expand into the creditcard market. Empower also announced it closed the acquisition of Philippines-based consumer credit and lending fintech Cashalo. Empower , a fintech helping to extend credit to underserved consumers, announced plans to acquire underserved creditcard provider Petal.

CreditRisk and FICO Score Trends? creditrisk and FICO® Score trends. At the same time, increasing adoption of recent innovations in credit scoring solutions should benefit consumers, leading to greater consumer empowerment opportunities and credit access.

. Which works better for modeling creditrisk: traditional scorecards or artificial intelligence and machine learning? Take, for example, our new credit decisioning solution, FICO Origination Solution, Powered by FICO Platform. It’s designed to help lenders make faster origination decisions without increasing risk.

Lenders are looking for new ways to connect with the estimated 3 billion people worldwide who fall outside the credit mainstream. These “credit invisibles” don’t have creditcards, bank accounts or credit history — so how can a lender assess their risk? EFL has seen a circa. appeared first on FICO.

This score can be used by an enterprise to understand its cyber risk and shore up defense gaps. The FICO Enterprise Security Score can also be used as an assessment tool by third parties such as cyber insurance providers and potential business partners. A score that quantifies cyber risk.

The new-age credit stack can do this efficiently with smarter underwriting capabilities, integrated data collection mechanisms and ability to automate workflows in the process. Improved Risk Management To assesscreditrisk accurately, new-age credit stack incorporates advanced algorithms and real-time analytics.

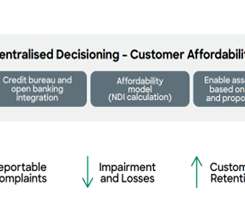

Covid to Cost-of-Living: Assessing Affordability in Uncertain Times. Affordability Assessments and Unrestrained Lending. Triggered in part by the US housing market collapse and an unprecedented number of loan defaults, the crisis uncovered a shocking level of unrestrained lending and excessive risk taking. by Matt Cox.

CreditCard Growth - Response Rates Up, Costs Down. China Minsheng Bank CreditCard Center has used FICO® Blaze Advisor® decision rules management system to help grow its business by creating an intelligent, automated marketing system that delivers targeted offers, which have seen a 10 to 15 percent jump in response rates.

How are advances in artificial intelligence and machine learning changing creditriskassessment? This led to a new scorecard and index that rank-orders affordability risk and complements traditional creditrisk scores. Join me at this session on Thursday, April 19, 10:15-11:15.

It is key to risk management functions, which entail assessing the likelihood that any given transaction could be fraudulent or present a creditrisk. Bank of America (BoA) is one notable success story in the field of analytical riskassessment.

PayFacs handle riskassessment, underwriting, settling of funds, compliance, and chargebacks which exposes them to greater potential risks. Major risk factors for PayFacs include fraudulent transactions, merchant creditrisk, regulatory compliance, and operational risks.

The FICO® Score is the lingua franca, or common language, for the credit scoring industry. It serves as a broad-based, independent standard measure of creditrisk. The FICO® Score model is based on data in an individual’s credit report, housed by the three primary U.S. consumer reporting agencies (CRAs).

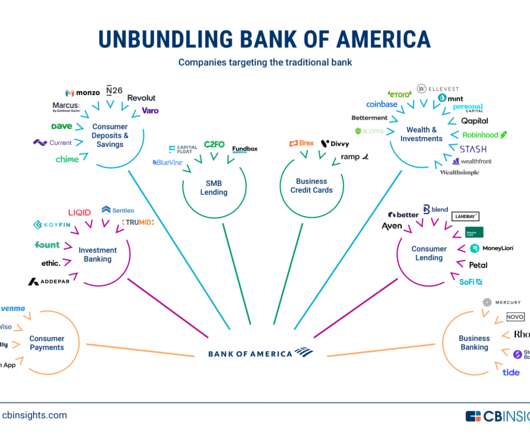

Below, we take a look at how tech companies are unbundling Bank of America’s front office, from consumer deposits and payments to equity research and business creditcards. . However, both brands have expanded to additional products, such as Venmo’s creditcard and Cash App’s stock investing offering. . Consumer payments.

(Photo by Çağlar Oskay on Unsplash ) Balance automates the entire invoice-to-cash cycle behind the scenes, handling onboarding, riskassessment, billing, collections, and cash application. Marketplace OS: Tools for online marketplaces to manage payments, financing options for buyers, and payouts to vendors.

The opportunity is also gigantic, Cheng told Webster, given that the country has some 800 million working adults, with less than half of them in possession of a creditcard. X Financial offerings include a balance-transfer creditcard product and an unsecured, high-credit-limit loan product.

Companies like Stripe and Adyen are captivating merchants with cutting-edge payment solutions beyond basic creditcard processing. By understanding their merchant clients’ cash flow patterns, sales volumes, and overall financial health, banks are better equipped to assesscreditrisk and offer tailored financing solutions.

But it occurred to them that their solution was useful outside of HR — and that many of the things that made someone a good hire of over time could also make them a good creditrisk over time, if the artificial intelligence (AI) model they were using to screen with were modified to that task.

A more predictive credit score means more predictable cash flows which are, in turn, more attractive to investors for all types of securitized assets (e.g., mortgages, auto loans, creditcards, etc.) The validation results for FICO Score 10 T demonstrate improved creditrisk prediction for this segment of the population.

That means the big opportunity for X Financial comes from the 400 million or so Chinese consumers who have creditcards, but are hampered by limits that are too low. X Financial’s offerings include a balance transfer creditcard product and an unsecured, high-credit-limit loan product.

Affirm uses proprietary technology to verify identity and assesscreditrisk in seconds by utilizing more sources of information than conventional FICO models, enabling it to provide financing to a broader set of consumers.

Banks can choose to assess a fee immediately (the current state) or within a defined period of time (i.e. Proportional fee assessment can charge a fee that would increase at designated transaction amounts. Naturally, your investor panel will pepper you with questions ranging from credit-risk concerns to revenue generation.

These fees are incurred by merchants for each transaction and are paid to the card-issuing banks as compensation for handling the creditrisk and processing the payment. Pass-through fees are essential for merchants since they directly impact overall creditcard processing costs. Who charges pass-through fees?

“Irrespective of whether it’s a creditcard, a personal loan from a bank, or a BNPL service, there will always be people who can’t manage their money or run into financial difficulties – or those who have no intention of repaying money borrowed. However, this assumption isn’t accurate.

These consumers are also more likely to have traditional credit products like credit and retail cards, personal loans, and student loans, but have lower liquidity and savings compared to non-BNPL borrowers. The BNPL platform then assesses their creditworthiness through a soft credit check.

Even in the most favourable economic conditions, borrowers with low credit scores have historically been more likely to fall behind on their payments for car loans, personal loans, and creditcards. Filtering customers based on income and savings, in addition to credit scores, can be a stronger predictor of mortgage risk.

These in-depth insights can help lenders expertly manage creditrisk in these uncertain times, while continuing to make competitive credit offers to consumers. .

Enhancing CreditAssessment for Existing Customers. LIFECARD, a creditcard company with more than 5.7 million accounts, is the first lender in Japan to adopt the FICO® Score to enhance its creditassessment for existing customers. Scoring Innovation in the Japanese Market.

FICO was an ideal fit for the FCRA world, and has been the dominant credit scoring model in the United States for over four-and-a-half decades as a result. Without a reasonable FICO score, home buying (with mortgages) auto-loans, creditcards and even simple checking accounts all become out of reach for consumers.

The complaints vary in their specifics, but all revolve around a basic premise: The old credit-scoring models are too backward-looking in a world where real-time data is available — and they are insufficient to the task of properly assessingrisk. Aire, though, is a credit-assessment platform intended to fill in that extra data.

FICO Scorable Population Shows Significant Improvement in Key Credit Metrics Over Past Decade. 1] “Risk in Bankcard Originations on the Rise”, [link]. by Ethan Dornhelm.

Trends in the macro environment are seen throughout the creditcard industry Rising prices, increases in the cost of securing and carrying debt, and the fear of higher unemployment rates are trickling through to consumer behavior on creditcards. Creditcard lenders are not only dealing with higher loss forecasts in 2023.

There has been much discussion and several studies over the years regarding the potential value of leveraging rental data in assessing consumer creditrisk. Which raises the question: Should rental data be widely reported to the three primary consumer credit agencies (CRAs)?

Every time a FICO Score is updated it incorporates unique features, leverages new risk prediction technology, and reflects more recent consumer credit behaviors. The FICO® Score was introduced to lenders over 30 years ago and has since become the best-known and most widely used credit score.

This trend holds true beyond just creditcard balances illustrated in the chart above; medical debt is about one-fifth of average auto loans, as another example. But our study revealed a different story: Generally, medical collections amounts are much less than other forms of debt.

Ethan Dornhelm wrote: The FICO® Score is the lingua franca, or common language, for the credit scoring industry. It serves as a broad-based, independent standard measure of creditrisk. A payment history of at least 6 months is necessary to derive a consistently predictive and reliable credit score.

Trust Bank is setting a precedent for financial services by onboarding an individual and delivering a creditcard to them digitally on their phone within four minutes, creating a seamless digital onboarding process for new customers. FICO Platform helps us to deliver that edge.”

Increasing of the fed funding rates leads to higher interest rates when seeking new credit or carrying balances on creditcards. For example, the average interest rate on creditcards accruing interest in Q4 2022 was 20.40% compared to 16.44% in Q4 2021 (Source: Federal Reserve G.19 19 report on Consumer Credit).

The secondary market requires all of the participants to effectively model creditrisk and prepayments. The FICO® Score is an important input into the default and prepay models, which form the core analysis in support of the To Be Announced (TBA) and creditrisk transfer markets. When a 700 Isn’t a 700.

In our top post, Vice President and General Manager of Scores, Sally Taylor explained the new FICO Resilience Index, designed to provide lenders with a more precise assessment of consumer creditrisk and consumers with demonstrated talent for weathering economic storms greater access to credit.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content