This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Visa A2A introduces an easy and intuitive experience for consumers, allowing them to easily manage their bills and subscriptions through their bank app. This will effectively provide a similar level of protection typically associated with card payments, so consumers can get their money back if there is an error.

However, this rapid growth brings significant regulatory challenges, primarily in balancing the need for innovation with the imperative of consumerprotection. Consumerprotection is not just a regulatory requirement : it is a fundamental right that must be safeguarded amidst advancing technology.

The FCA’s proposed safeguarding reforms for payments and e-money firms, aiming to enhance consumerprotection and operational compliance. The reforms ensure robust safeguarding practices, bolster consumer trust, and address risks like fund shortfalls during insolvency. Why is it important?

Open industry model, fostering collaboration Visa A2A will be based on an open system available for all eligible banks and other industry partners to join, and introduces standards, rules and a dispute management service to help protectconsumers and further modernise open banking-based payments.

With OJK taking the regulatory reins and the Travel Rule now in force, crypto firms in Indonesia must evolve fast or risk falling behind in global markets, regulatory approval, and user trust. ” What happens after Travel Rule data is exchanged is equally critical.

These changes aim to enhance consumerprotection by ensuring that customer funds are adequately safeguarded. The FCA is introducing phased safeguarding rules, with interim measures strengthening existing regulations and final requirements aligning with the Client Assets (CASS) framework.

The guide simplifies the financial planning journey for consumers, providing easy to understand and implement rules of thumb for individuals at different life stages. This includes advise on spending no more than 15% of their take home salary on insurance protection.

Your guide to the Consumer Financial Protection Bureau's (CFPB) imminent proposals for a new regulatory framework governing “Personal Financial Data Rights” The US will propose a new “Open Banking Rule” this year which will set the foundations for an ecosystem with the potential to become the largest in the world.

It highlights the need for a strategic, proportionate approach to safeguarding that aligns with broader regulatory and consumerprotection goals. Adequacy of consumerprotections A second area where there should be pause for thought is whether the FCA even considers that its proposals offer the best customer protection.

2024 reshaped payments with instant payment mandates, crypto regulations, and enhanced consumerprotection driving innovation and security. In 2024, payments regulation underwent seismic shifts, with reforms spanning fraud prevention, digital innovation, and consumerprotection, collectively redefining the industry’s future.

The objectives of PSD3 and PSR: Strengthening consumerprotection Improved competition in payment Harmonisation of EU-legislation Where do PSD3 and PSR stand now? The revised regulations on strong customer authentication and liability rules are significant. Understanding these changes is key to keeping the UK competitive.

Regulatory clarity and consistent standards are critical for providers offering safe, transparent and responsible financial services and even more important for consumers who expect protections when utilizing financial services including Buy Now Pay Later,” said Phil Goldfeder, Chief Executive Officer of AFC. “We

Jaspreet Kaur Senior consultant, Digital Finance "Consumerprotection and fraud prevention needn’t be at odds with one another; one can, instead, complement the other. Such a model enables firms to proactively stay on top of both their consumerprotection and their fraud risk management obligations."

How the FCA can define and balance acceptable risk in UK payments regulation to support innovation while ensuring financial stability and consumerprotection. Many of the current rules were designed for an earlier generation of financial services and do not reflect the complexity or speed of todays payments ecosystem.

In October 2024, the Consumer Financial Protection Bureau (CFPB) issued its final ruling on section 1033 of the Dodd-Frank Wall Street Reform and ConsumerProtection Act. The verdict has been a significant catalyst for open banking, requiring financial institutions …

Axios reported the investigation is examining Apple’s possible use of deceptive trade practices that may have broken consumerprotection laws. It is important that Apple’s measures do not deny consumers the benefits of new payment technologies, including better choice, quality, innovation and competitive prices.”.

Why an Upgrade is Needed PSD2, implemented in January 2018, was designed to transform the EU payments ecosystem by enhancing competition, boosting innovation, and strengthening consumerprotections. ConsumerProtection with stronger authentication and fraud prevention measures, such as Strong Customer Authentication (SCA).

This guide will walk you through the basics of credit card surcharging in Canada, from legal background and card network rules to disclosure requirements and best practices. In Canada, the answer is yes—but with some rules and responsibilities attached. That’s where surcharging comes in. Can I surcharge in Canada?

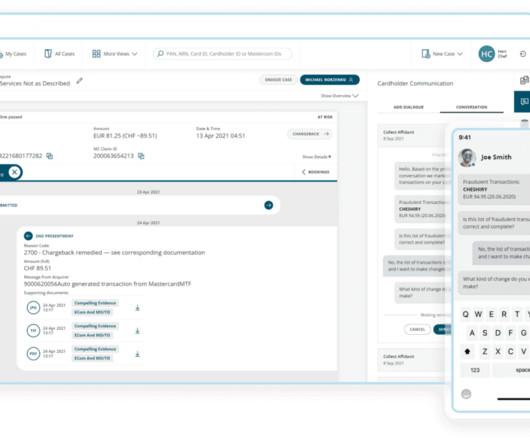

In addition to deflecting claims, the purpose-built chatbot can handle all eligible fraud recovery cases and cardholder disputes related to the consumerprotection framework of international card payment networks. Affidavit PDF documents are created in a fully automated way.

Sponsored [On-Demand Webinar] Navigating the Macro-economy: Opportunities in Multi-currency Settlement Share 1 Related Company Coinbase Channels /cryptocurrency /retail banking /payments Keywords e-commerce stablecoins Comments: (1) Eli Talmor CEO at ID-Bound 9 hours So there is another option for consumers.

But here’s the catch: surcharge rules are a patchwork of federal guidelines, state laws, and card network rules. Not knowing the rules can result in fines, lawsuits, or worse. Getting the rules wrong can expose your business to legal penalties and fines from your payment processor. Some states don’t allow them at all.

“Four of the top five now restrict crypto purchases on credit cards, and with the FCA signalling tighter rules ahead, I’d even expect more banks to follow suit. This sits within the spirit of the Consumer Duty rules, without restricting consumer freedom.”

As the EUs most extensive effort to regulate the crypto market, MiCA seeks to address longstanding issues such as regulatory fragmentation, consumerprotection, and market stability. MiCA, which entered into force in June 2023, introduces a comprehensive regulatory framework for European crypto-assets.

These changes aim to address persistent issues in safeguarding practices and enhance consumerprotection. Why safeguarding matters Safeguarding ensures that funds received by payment and e-money firms are protected. Enhanced rules for safeguarding through insurance or comparable guarantees. What’s next?

“We’re consulting on proposals to make safeguarding rules stronger and clearer for payment and e-money firms so customers get as much of their money back as quickly as possible if the firm goes out of business,” Matthew Long explained. The FCA has asked for all responses to the consultation by 17 December 2024.

The payments processor was accused of abusing the credit-card system and enabling deceptive foreign operators to access it, costing consumers millions of dollars. The settlement comes shortly after the Consumer Financial Protection Bureau withdrew from the civil case amid its ongoing pullback from enforcement activity.

Legislative reform: The EBA recommends that PSD3/PSR clarify the requirements applicable to EMT transfer services, avoiding duplicative regulatory authorisation requirements while ensuring robust consumerprotection and market integrity. What happens before PSD3/PSR applies? Will PSD3/PSR fix the problem? Amend MiCA.

The regulator will have the authority to request information from tech firms and also enforce other Indian laws aimed at consumerprotection and fair competition, the sources said. The sources also told Reuters that social media companies that capitalize on advertising and user data could also be impacted by the new rules. .

Parliament’s Internal Market and ConsumerProtection Committee issued a resolution Thursday (Jan. 23) that will put rules into place to address the challenges of fast-developing artificial intelligence and automated decision-making technology.

Payment processing and data handling rules vary by country, and non-compliance can result in fines or a loss of customer trust. Key regulations include: GDPR (General Data Protection Regulation) : For merchants targeting Europe, GDPR compliance is mandatory, emphasizing data privacy and protection.

One of the key shifts in APP fraud this year involves the introduction of new reimbursement rules , which came into effect in October 2024. New APP reimbursement rules The introduction of new APP fraud reimbursement rules on 7 October 2024 marks a significant step in enhancing consumerprotection. Read More »

As one might expect of a financial product that has so rapidly become so widely popular, the prepaid card industry managed to catch the attention of the Consumer Finance Protection Bureau, which has been considering new regulations for some time that would create “strong federal consumerprotections for prepaid account users.”

Curve , the ultimate digital wallet, has become the first to offer section 75 protection on purchases made through its Wallet. This is a step change in consumerprotection, allowing users to make payments without worrying about losing money if a product is faulty or if theres a problem with the purchase.

The rules behind it come from a mix of card network policies, federal law, and state regulations. So, it’s important to understand these rules and regulations in their entirety. If you run a business – or are someone who pays attention to the line items on your receipts – it helps to know how surcharging rules work.

In parallel with growing market adoption of surcharging, more states have considered and enacted surcharging legislation, often with the stated goal of standardizing surcharging and ensuring consumerprotection. In 2024 alone, more than a dozen state legislatures introduced bills related to surcharging and consumer fees generally.

While deregulatory measures such as revisiting the Open Banking Rule may gain momentum, their implementation faces procedural and legal challenges. For example, while the CFPB mandates data sharing between financial institutions and fintechs, it also warns consumers to approach fintech products with caution.

Between card network rules, signage requirements, and state regulations, there’s a lot to keep track of. This article walks you through what credit card surcharge compliance really means and provides a practical checklist to help your business stay on the right side of the rules. Here are three important rules to be aware of: 1.

The Consumer Financial Protection Bureau (CFPB) announced Thursday (April 25) that it has issued a request for information on its remittance rule, which had faced calls by the Credit Union National Association for revision. The rules excluded a provider that does less than 100 transfers.

The Bureau of Consumer Financial Protection (CFPB) has delayed the Aug. 19, 2019 compliance date for the mandatory underwriting provisions for its short-term, small-dollar (payday) rule, according to various reports. The CFPB is also correcting several errors in the rule. Compliance is being delayed 15 months, to Nov.

Not understanding those rules can lead to compliance issues and overall confusion. State rules vary. State-Level Tax Variations and Compliance Tips Not every state has the same rules for credit card surcharges. Others have no specific rules, but you still need to follow general tax and consumerprotection laws.

As the specifics of the CFPB’s pre-paid card rule are making their way through the ecosystem, the players are starting to come out with their takes on the newest set of financial regulations. Among the opinionators was Green Dot CEO and founder Steve Streit.

They worry that the new rules could encourage fraudulent claims and disproportionately impact smaller players in the digital banking sector. The Payments Association, a trade body, recently sent a letter to the Treasury to express concerns that the new rules would encourage more fraud and drive smaller payment companies out of business.

Open banking Open banking– specifically the recently released Section 1033 of the Dodd-Frank Wall Street Reform and ConsumerProtection Act– was one of the hottest topics of the show. The majority of people on the networking floor I spoke with had not read the entire, 594-page ruling.

The regulatory body is currently taking public comment on the rule. Continuous third-party records access The proposed rule states that if banks rely on non-bank companies to manage custodial deposits and their records, the bank must have continuous, direct access to records held at the third party organization.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content