This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The categories essentially replaced Visas prior CPS interchange program, and apply to different consumercredittransactions. The broadest difference is that Product 1 applies to card-not-present transactions and Product 2 applies to card-present transactions. per transaction Rewards: 2.04% + $0.10

The two categories essentially replaced Visas prior CPS interchange program, and apply to different consumercredittransactions. The broadest difference is that Restaurant 1 applies to card-not-present transactions and Restaurant 2 applies to card-present transactions.

Looking for a Printable creditcard fee sign ? Download PDF × With the prevalence of creditcard use in 2024 comes the often-overlooked detail of physical creditcard surcharge signs, which provide transparency of the fees merchants charge their customers to use creditcard payments to purchase.

We hope Mastercard and Visa will stop punishing charities who accept commercial card payments by removing these onerous fees.” per cent on consumercredittransactions, and 0.3 per cent for consumercreditcardtransactions. For every 100 transaction, up to 0.30

Capital One contends point of sale credittransactions are too risky to support, but competitors believe it's creditcard debt that's falling out of favor with consumers.

percent to customers who use the service to decrease their creditcard debt, according to a report in The Wall Street Journal. The fee would be charged for creditcard payments that are more than $299 a month, and the change will start on March 26. percent fee on creditcard repayments, regardless of the size.

Consumer payment data has become a valuable asset for businesses. Consumer data, primarily gathered from creditcardtransactions, offers information that can help businesses enhance their operations, understand customer behavior, and ultimately increase their profitability.

It also explores the increasing adoption of real-time payments, which many countries are embracing as a more efficient and cost-effective alternative to traditional card payments. It notes that rising card fees costs in the region have significantly impacted merchants’ acceptance costs, prompting regulatory action in various markets.

In technology, especially when it comes to consumer-focused technology, Apple is viewed as a disruptive force. The digital card will be linked to Apple Pay. Apple Card is set to be available starting this summer. The duality of physical and digital cards seems to have sparked at least some mulling from other firms.

Credit union service organization (CUSO) PSCU compared the 19 th week of 2020, which concluded on May 10, to the same timeframe in 2019 to discover the impact of the pandemic on consumer spending and shopping trends. The average debit card purchase amount rose 19.9 percent jump in debit card spend for the week ending May 10.

Namely, it will continue to be a favored payment method among consumers. To get a sense of the update, at least as seen in data from reports tied to the December quarter, the card networks showed pent-up demand to spend – and though cross-border activity was down double digits, there were notable bright spots.

Following last year’s major bank collapses — like First Republic Bank and Silicon Valley Bank in the US , and Credit Suisse in Switzerland — consumer confidence in banks has waned. It concentrates on individual and corporate clients, creditcard services, and small and medium enterprises.

“This year’s holiday shopping season was dramatically different from prior years as the COVID- 19 pandemic continues to impact and shift consumer behavior,” Glynn Frechette , senior vice president, Advisors Plus at PSCU, said in the announcement. 27 in the retail goods space among the organization’s owner credit unions were up 26.2

Today’s stories include a discussion about how India could go from creditcard laggard to having one of the most sophisticated payments systems in the world, the outlook for initial coin offerings (ICOs), a development in augmented reality (AR) retail and news about growth in ACH debit and credittransactions.

The new feature works with firms’ existing debit and credit programs and allows consumers to select up to five historical transactions to move into a BNPL payment plan. based Curve’s Flex feature that allows customers to move transactions into a installment repayment plans. Curve, a U.K.-based

Drilling down into the payments volume, and as shown in supplemental materials from the company, total credittransaction volumes were $1.3 The total transaction count was up 10 percent to 54.8 He also noted that the company had been selected for the Venmo co-branded creditcard. Tap To Pay. “In

creditcard interchange rates for at least a five-year period as part of a legal settlement with merchants. issued consumercredit and commercial credittransactions at U.S. These rules will maintain core consumer protections and transparency, replacing standards that had been updated in 2012.

A merchant account acts as a pathway between your business, your customers, and the issuer and acquiring banks to process electronic transactions like creditcards. This includes creditcard payments, debit cards, and other payment options that require a merchant account to process payments, such as eChecks and ACH.

Visa, the creditcard company, and Interswitch, Africa’s integrated payments and transaction solutions company, announced news on Friday (June 30) that they will partner to accelerate mobile payments adoption across the region. It can also be used to enable consumers who use different mobile phones and services to interact. .

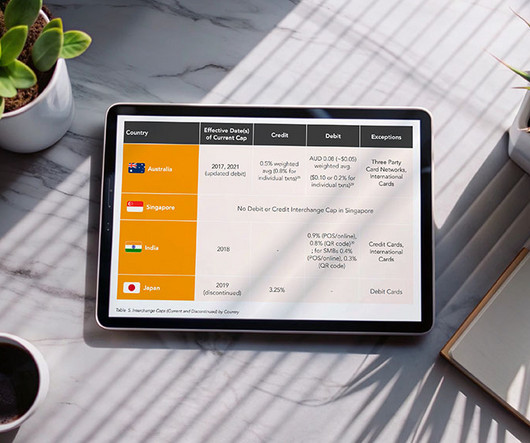

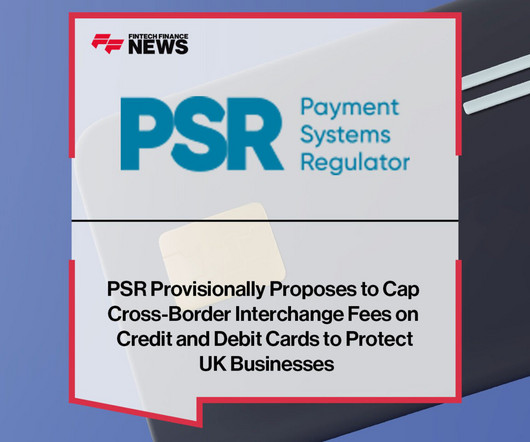

for UK-European Economic Area (EEA) consumer debit transactions and 0.3% for consumercredittransactions (where the transactions are made online[1] at UK businesses) A lasting cap on these interchange fees in the future, once further analysis has been carried out to establish an appropriate level.

And in the latest installment of Data Drivers, statistics show that the recently launched Same Day ACH initiative has got businesses, and consumers, moving to manage cash flow on a daily basis, across a variety of use cases. This is the percentage of payments made through P2P transactions using same-day payments. 13 percent.

for UK-European Economic Area (EEA) consumer debit transactions and 0.3% for consumercredittransactions (where the transactions are made online [1] at UK businesses) A lasting cap on these interchange fees in the future, once further analysis has been carried out to establish an appropriate level.

Strength in global consumer spending — along with double-digit cross-border gains and traction in B2B payments — marked third-quarter Mastercard results released Tuesday (Oct. The company said that gross dollar volume, which is the total dollar volume of transactions processed, reached $1.4 and beyond. billion, up more than 14.7

TILA is a federal law designed to promote the informed use of consumercredit by requiring disclosures about terms and cost. It aims to give consumers a more precise understanding of what they are agreeing to before signing on the dotted line. Standardization lets consumers compare loan terms on equal footing.

Co-branded CreditCards A co-branded creditcard is a cred it card issued by a joint effort between a bank and another non-financial brands or merchants. Consumer Lending Consumer lending refers to the financial category focused on providing individuals and households with loans for various personal needs.

There was a time when data breaches were not a daily part of consumers’ day-to-day lives. Sure, creditcards got stolen or skimmed from time to time — but such occurrences were comparatively rare. The big nervousness that consumers have is related to the downside of the debit plus PIN compromise. “The What happened?

Brad Fauss, CEO of the National Branded Pre-Paid Card Association and MPD CEO Karen Webster dug into the potential for these rules to create the kind of inconsistencies that could very well disadvantage the very consumers that the CFPB intended to protect. Who Uses Prepaid Anyway? So far, so good.

Within that figure, debit payments were up 11 percent in constant dollars to $1 trillion, while credittransactions were up 7 percent to $1.2 Total transactions and processed transactions were both up 11 percent to a respective 53.2 Cards in the field, so to speak, were up 4 percent year on year to 3.4

Visa, reporting fiscal second quarter results on the heels of two major changes in structure and at the helm — the first through the acquisition of Visa Europe and the latter through the two-quarters-old tenure of Al Kelly as CEO — showed growth across all major business lines as consumer spending continued on a robust path.

the company said, total volumes stood at $388 million, up from $378 million a year ago and bifurcated between $199 million in debit transactions and the remainder in credittransactions. economy, marked as it is by low unemployment and relatively strong consumer spending. Within the U.S.,

trillion, as measured on a constant dollar basis — up on consumercredit and higher holiday spending — and where the United States was about 43 percent of that tally. Total processed transactions were up 12 percent to 30.5 billion, and debit and credittransactions were up as well. Revenue was $4.9

If the percentage is high, buyers pay their creditcard vendors on time. A low percentage suggests a pattern of late or nonpayment to vendors for credittransactions. Additionally, AP automation can help businesses keep track of spending, as all transactions will be recorded in one place. Enter Nanonets.

The payment landscape in the United States is intricate, continuously evolving to accommodate innovations and meet the changing demands of consumers. Its primary objectives encompass safeguarding consumers, maintaining financial stability, promoting market integrity, preventing fraud and security breaches, and ensuring legal compliance.

Creditcards were rarely issued to women directly: A woman’s card was generally issued as a rider on her husband’s, and it was nearly impossible for women to secure cards and loans without male consignors. The ECOA changed this by specifically banning it.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content