This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In 2024, consumer spending on in-app purchases and subscriptions hit $150billion globally, according to digital economy data provider, Sensor Tower. In its latest research, the firm uncovers how consumer spending on apps has evolved in the past year. Interestingly, consumers are not spending this money in the gaming sector.

Consumers’ banking habits have changed radically since the pandemic was first declared in March. Not only are many account holders visiting brick-and-mortar branches less often than they did before the pandemic, but many are also more reliant on digital banking channels — particularly mobilebanking apps — than they have ever been.

In keeping with its constant dedication to providing cutting-edge services to its customers, National Bank of Kuwait (NBK) announced introducing a new service that allows customers to confirm payment transactions online through the NBK MobileBanking App, making itself as the first provider of this service in Kuwait.

With smartphone theft on the rise across the UK, fintech and mobile security platform, Nuke From Orbit , is launching a nationwide campaign to combat this growing crisis. Our goal is to empower people with simple, effective ways to protect their mobile devices and create new habits that secure their personal data as we kick off the new year.

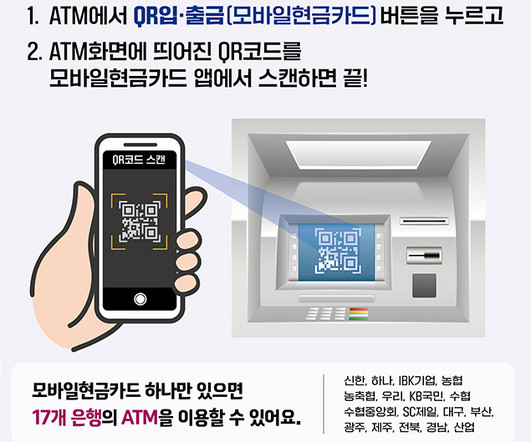

SCAN: Availability is being expanded from NFC on Android phones to QR Codes on all smartphones Consumers in Korea can now make cash withdrawals and deposits at ATMs by scanning a QR code with their Apple or Android smartphone rather than needing to use a physical bank card.

Rampant data breaches have left consumers on edge about digital fraud. In fact, recent PYMNTS research shows that most consumers believe they can do a better job of identifying and protecting themselves against fraud than their FIs, with 71.2 Despite widespread demand for greater mobilebanking authentication controls, only 39.9

Since the onset of the pandemic, banking activities like opening new accounts and applying for loans are now being done virtually to socially distance and help curb the spread of the virus. This means consumers are turning more to digital tools, but unlocking and embracing the potential benefits of these tools has not been easy.

Consumers have come to expect specific services and features from their banks. New research conducted by PYMNTS, however, reveals that banks and other financial institutions (FIs) appear to be lagging in terms of meeting these expectations. consumers on their mobilebanking app usage patterns. In fact, 80.8

TD Bank wants to help its customers spend a little less money — and has thus launched a transaction tracking app that uses the time-tested “green means go, red means stop” method of cueing human habits that traffic lights have perfected. TD MySpend combines spending from different deposit and credit card accounts only at TD Bank.

Smartphones have become a ubiquitous part of life for consumers around the globe. They use their mobile devices for everything from checking the weather to posting on social media to pulling up real-time maps and using them to navigate to new destinations. The report surveyed 2,141 U.S.

American consumers have fallen for mobilebanking apps, but up to now, most businesses were not seemingly showing apps the same love. With the number of mobilebanking customers now outnumbering those who bank at branches for the first time, consumers have warmly embraced banking via mobile apps.

Consumers were forced to swiftly adapt to a world where their primary way to interact with businesses or banks became digital-first, with the pandemic seemingly increasing the number of consumers turning to digital tools to conduct their financial activities. Developments From Around The World of Digital-First Banking.

How to bring mobilebanking to the realm of the spoken word – beyond the mere recitation of account data, beyond call and response? Banking is, of course, about more than account balances. Banking is, of course, about more than account balances. Thus, upon download, users are guided through the process.

When I read about people infecting their Android phones with Gugi ––a Trojan malware that steals user credentials when consumers log into mobilebanking apps––by clicking on a link in a random text message, it’s clear to me that mobile phone users are in need of some security hygiene lessons. Why mobile hygiene matters.

Anti-fraud efforts can seem like word salad with exotic ingredients being tossed around: strong consumer authentication ( SCA ), two-factor authentication (2FA), the second Payment Services Directive (PSD2) … you get the idea. Ask consumers what they want, however, and the acronyms vanish like a metaphor for things that vanish.

According to recently released research from the American Bankers Association, mobilebanking is becoming increasingly popular among consumers of young ages. USAA was not the only digital banking platform to debut new services and innovations recently. About The Tracker. About The Tracker.

According to Brad Fauss, president and CEO of the Network Branded Prepaid Card Association, the recently released regulations on prepaid cards from the Consumer Finance Protection Board could be another instance of good intentions gone wrong. Around the Digital Banking world. Could this be a case of good intentions gone awry?

At a time when 80 percent of apps ask for (and are usually given) users’ geolocation data, the fact that most mobilebanking applications still don’t is unacceptable, GeoGuard CEO David Briggs told Karen Webster in an interview. Two-thirds of all banking apps don't ask for location at all,” Briggs said. A Rude Awakening.

Nine years after the introduction of the iPhone to the market — and the subsequent great mobile leap forward — the verdict is pretty much in on mobilebanking applications: Consumers like it, verging on loving it, and are eager for more of it. Consumers want the latest mobile capabilities.

65 percent: Share of German customers who use one or more mobilebanking apps. 55 percent: Estimated portion of consumers who will use bank branches by 2024. 63 percent: Share of mobile device users who have downloaded at least one financial app. 75 percent: U.S.

When you talk to the co-founder and CEO of a mobile-first digital bank account offering, you are likely to hear that millennials, to put it lightly, are not fond of big banks. And that’s where digital banking options like Chime (a mobile-first digital bank account, for those of you playing at home) enter the picture.

Business to business (B2B) application programming interfaces (APIs) are helping smooth the flow of data between companies, including businesses and their financial services software as well as between banks and their corporate clients. The value of the technology is evidenced by the vast number of APIs that businesses use and consume.

Digital identity solutions are becoming more and more commonplace, especially as consumers grow increasingly aware of the weaknesses of authentication methods like passwords. For more on these and other digital identity news items, download this month’s Tracker.

Download the free report for a data-driven look. Personal & Consumer Lending. Personal & Consumer Lending. Personal & Consumer Lending. Personal & Consumer Lending. Personal & Consumer Lending. Personal & Consumer Lending. Personal & Consumer Lending. Activehours.

In search of added convenience and simplicity, banking customers are migrating to online and mobilebanking interfaces, leaving in-person visits to brick-and-mortar branches behind. Westpac , one of Australia’s “Big Four” FIs, for one, is rolling out new omnichannel banking offerings. About the Tracker.

Neural Payments’ innovative platform enables bank customers to transfer money from their account to anyone, regardless of whether the recipient’s institution utilizes Neural Payments and without the need to download a third-party app or register a new card. Recipients can claim their payment within seconds after funds are sent. “A

Mobilebanking apps are designed to make digital banking more convenient for customers, yet 21.7 percent of consumers who use these apps are dissatisfied with them. Our research shows that consumers’ biggest issues with banking apps is their concern over how easy it is to make mistakes with them.

Consumers’ migration to using contactless payment methods more often for their speed and convenience was only accelerated during the onset of the pandemic last year. Fagan said CUs have seen deposit balances rise, a sign that consumers have been careful about building savings, reducing debt and compiling barriers against financial shocks.

More consumers are turning to the omnichannel offerings of banks and credit unions (CUs) as they follow stay-at-home mandates, and cybercriminals are eager to launch attacks that make use of these channels. To find more about these and the rest of the latest headlines, download the Playbook.

Online and mobilebanking interfaces have become must-have features for financial institutions in the digital age. Fifty-five percent of Americans have a full-service banking app on their phone, and 16 percent check these apps at least once per day. How Wells Fargo Works to Meet Evolving Expectations .

As the report states, “We … find that a significant share of consumers are willing to bank with the institutions — financial or otherwise — that offer them the best spending and money management tools.”. Mobile Cards: Make or Break? The highest interest is among “bridge millennials” whose card spend averages $40,000 annually.

Consumers, businesses and financial institutions (FIs) cannot wait to bid adieu to 2020, which has been one of the most trying years in recent memory. Credit unions were not immune to the dramatic shift in consumers’ banking preferences when the pandemic began. To get the full story, download the Tracker.

Online account openings increased by more than 200 percent in April, while all mobilebanking traffic rose by 85 percent. This shift to digital banking is also unlikely to slow once the pandemic recedes, as only 40 percent of bank customers expect to return to bank branches regularly after the crisis ends.

In 2019, 77% of US consumers were using at least one type of digital payment system. What has grown more significantly is the number of electronic payments and alternative payment methods consumers now use. The adoption of digital payment systems in the US has grown, with 78% of consumers using at least one type by the end of 2020.

Banking startup N26 has announced that its mobilebanking app is now available to customers across the United States, following the completion of a beta program that lasted two months, according to a release. Once it is downloaded, people can apply for an account and a Visa debit card.

of all mobile threats detected included mobilebanking Trojans, highlighting the prevalence of these targeted attacks. So, when a mobile app is downloaded or launched, SecIron is able to compare the app’s signature to the signatures in its database. A 2023 report by Kaspersky found that 40.8%

Consumers cooped up at home by the pandemic have, in many cases, reoriented their entire lives around digital — and in some cases even learned to love the new ways of doing things far more than they liked the old ones. The consumer is shifting to virtual and digital in almost all walks of life,” he said. “We

“ Zelle is one of the fastest-growing consumer financial brands in history, and we are proud of our momentum, especially this quarter, as we signed more than 40 financial institutions to our network through partnerships with our processors — CO-OP, FIS, Fiserv and Jack Henry & Associates.

The appeal, Britt said, coincides with other retail tendencies that attract digital consumers. There are plenty of reasons for millennials to be unhappy with traditional banking, he said, noting that the relationship between big banks and consumers, as it currently stands, is in deep disrepair. The other part?

Despite the influx of mobilebanking and payment options, plastic card use, and a focus on financial infrastructure, cash remains heavily cemented in the Middle Eastern and African economies. In 2016, Middle Eastern consumers made $0.9 Key Findings From The Latest Index. percent of Saudi Arabia’s GDP. trillion in cash payments.

The business model is akin to mobilebanking services seen in other parts of the world, such as M-PESA, which in a nutshell leverage mobile devices to facilitate the flow of money, rather than relying on banks or wallets that are in turn issued by third parties. Apps — And Agents, Too .

App-based personal bank Jiko, set to debut in 2018, says its efficient structure allows for providing 0.5 Meanwhile, mobilebank Zero says bypassing physical locations allows for a 1 to 3 percent cash back on all spending. TO DOWNLOAD THE NOVEMBER EDITION OF THE PYMNTS DIGITAL BANKING TRACKER , CLICK THE BUTTON BELOW. .

If looking for evidence that we live in an increasingly digital world, one need not look much further than the veritable explosion in online and mobilebanking in the last half decade. consumers since, as of this week, they won the ability to gamble more — SCOTUS said the states are free to embrace sports betting.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content