This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Visa bolsters Asia Pacific product suite Payments giant Visa showcased a range of new products and solutions at Singapore Fintech Festival, revealing plans to roll them out across Asia Pacific. These include: Visa Flexible Credential – This enables a single card product to toggle between payment methods.

Credit cards are a staple in the wallets of consumers today, and they will undoubtedly be a payment method of choice for years to come, particularly as the adoption of mobile and contactless payments continues to grow. Or they could use a mobile credit card terminal if they prefer to collect payments at the table.

year-over-year (YoY), according to the National Bank of Cambodia (NBC). Wing Bank, TrueMoney among most used services for e-commerce payments Findings from the study featured in the Profitence report further underscore the rapid rise of digital payments and digital banking in Cambodia. million transactions in 2023, up 28.7%

And yet, accepting non-cash forms of payments is more or less required to operate a modern business, at least in the U.S. They include: the merchant, cardholder, card associations, acquiring bank, issuing bank, and payment processor. Acquiring Bank: The business’ (i.e., merchant’s) bank.

Like most business owners, your instincts tell you to hop on the bandwagon and launch an online store for your business. From different types of online payment gateways and key features to look for, to tips to help you choose the right payment solution for your business and implement it. This is expected to grow to 22.6%

At the Visa Payments Forum in San Francisco, Visa has unveiled new products which will address the evolving consumer payments demands. The new products and services Visa unveiled will begin to roll out later this year. This year, new ways to ‘tap’ on a mobile device will become an integral part of the Visa experience.

Armenia Population: +2,967,000 Capital, financial hub and largest city: Yerevan Gross domestic product (GDP) per capita: +$8,500 Access to a formal financial account (adults): 52.3 per cent Central Bank of Armenia (CBA) Armenia’s growth has been driven in part by its young, tech-savvy population. per cent holding a credit card.

Accepting payments always comes with processes and fees, particularly when it comes to online or digital payments. TL;DR A payment link enables you to request and accept online payments without having to build a website or checkout page. Payment links are ideal if you don’t process a lot of online sales.

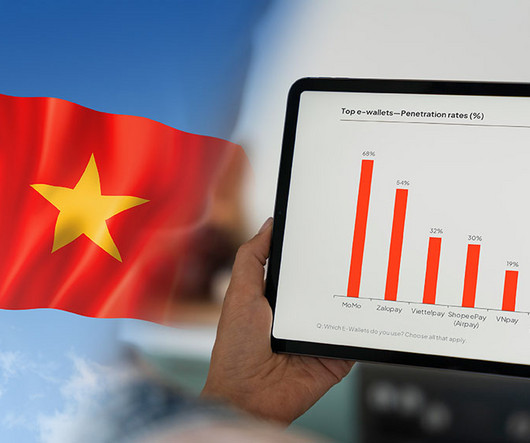

Vietnam’s digital finance landscape is undergoing a notable shift as new players emerge, established ones fade, and traditional banks rise to prominence, a new report by Decision Lab shows. However, by Q4 2023, Moca had slipped out of the top rankings, replaced by mobile apps from traditional banks.

They enable secure, efficient in-store and online payment processing and offer flexible payment options that customers demand today. Merchant services are comprehensive solutionstools, systems, and supportthat allow businesses to process in-person and online payments. custom software for a particular industry or market).

While brick-and-mortar retail isnt going away, todays customers value the convenience of shopping online. That means selling your products and services online allows you to better serve your customers (and reach new ones!) To accept online payments, you need a payment processor and payment gateway.

Are digital first banks in Asia poised to lead a disruptive charge against well-entrenched, established commercial banks? In the traditional banking sphere globally, but especially true in Asia, there is a considerable proportion of unbanked and underbanked populations who lack complete or any access to banking services.

Confronted by shifting factors such as tech advancements, generative AI, high interest rates, increased institutional oversight, and evolving customer expectations — the best banks must adapt their business and operating models in 2024, including in Asia. CHINA #1 China Merchants Bank China Merchants Bank Co.,

PayU GPO , the leading online payment service provider operating in over 40 emerging markets, announces a major step forward in its commitment to Africa, unveiling the launch of Account-to-Account (A2A) payments in Nigeria and the appointment of Ryan Engel as the new Country Manager for South Africa.

With a payment gateway, they simply enter their card details online on your website or app. In turn, the payment processor ensures a seamless transfer of the information between the merchant, issuing bank, and customer. For example, if you operate an online store, you need fast and secure online payment solutions.

TL;DR You get to choose from traditional payment methods like cash and checks, online payment methods like digital wallets and ACH transfers, and emerging payment methods like BNPL services and cryptocurrencies. They let buyers initiate payments by placing their mobile phone near a compatible payment terminal.

Moreover, as super apps and embedded ecosystems gain traction in emerging markets, tokenisation offers a scalable security model that can flex with the complexity of multi-role, multi-wallet environments, notes Venkat Srinivasan, sales & go-to-market, banking and payments products, at Thales.

As an independent software vendor (ISV) or eCommerce platform, these statistics mean that you should focus on function when developing products for your clients. In fact, integrating payment capabilities into products that businesses use to conduct their operations can help SaaS providers address $35 trillion in payments annually.

However, in recent decades, the government has engaged in efforts to diversify the economy to include other agricultural products, as well as non-agricultural sectors such as tourism and natural resources like oil, gas, and gold. Mobile phone usage in Senegal has surpassed 60 per cent this year.

The plastic card, by necessity, is giving way to digital cards, and mobile apps are bringing card-not-present transactions, increasingly, to mobile devices. She noted that mobile app use is up double-digit percentages as of April, when the pandemic shifted so much of everyday life online.

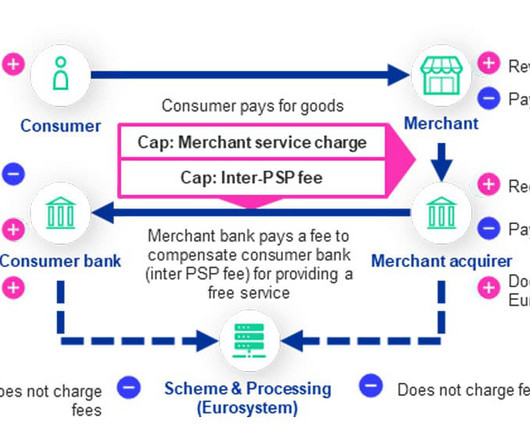

TRANSACTION FEE: A step-by-step overview of the digital euro compensation model Payment service providers will be able to charge merchants a fee for enabling them to accept digital euro transactions, the European Central Bank (ECB) has revealed, but a cap will be placed on the amount that it will be possible for them to charge.

The coronavirus pandemic — which has forced all of us online — is exposing just who in financial services has embraced digitization, and who is truly digital native. We now must bank entirely online, by necessity. And many of us must transact entirely online, by necessity, to get the goods and services we need on a daily basis.

Authorization An authorization is a request to the cardholders bank to approve a charge. Acquirer (Acquiring Bank) The bank or processor that works with the merchant. Issuer (Issuing Bank) The issuing bank is the bank that gave the customer their credit or debit card.

Dwollas clients are now able to leverage Plaids instant account verification and real-time balance check alongside comprehensive pay-by-bank payments through a single vendor and a single API. Fintech myPOS unveils a new strategic partnership with Satispay , an Italian independent mobile payment firm.

The pandemic has exposed the pain points of all verticals when it comes to payments, and especially when it comes to transacting in person, in a tactile environment, with cash, and where banking conduits are limited. Banks have been inching into the space; cash still remains a hallmark. Looking Toward Underserved Markets .

The list, produced by CNBC in collaboration with market research firm Statista, highlights the world’s top 250 fintech companies across eight market categories: payments, wealthtech, business process solutions, neobanking, alternative finance, financial planning, digital assets and banking solutions. billion (US$4.4

Make that leather wallet a mobile one, wielded on smartphones. As we noted in this space earlier in the summer, using apps to bank is markedly being embraced by the younger generation. As spotlighted in the Digital Banking Tracker , the global digital banking market is slated to grow by 16 percent, compounded annually.

It plans to leverage its Islamic finance industry experience via engagement with Connect IFA through events and webinars to raise awareness of its ethical finance products, designed in accordance with Islamic finance principles. Conister Bank Limited has launched an online deposit system for its UK retail customers.

Visa has signed an agreement with Abu Dhabi Islamic Bank (ADIB) to collaborate on an enhanced threat intelligence solution and integrate its advanced cybersecurity capabilities with digital payments. Additional partnerships MiFinity, a global payment services provider, has integrated Apple Pay into its mobile app.

This April, The Fintech Times is focusing on all things embedded finance, the integration of financial services into non-financial products and services. As time passes, consumers are seeing the number of embedded finance offerings increase across the wide range of products and services they use.

“Creating frictionless B2B commerce experiences is critical for driving long-term buyer loyalty for our clients,” TreviPay Chief Product and Technology Officer Dan Zimmerman said. In a statement, the company noted that these options work across all purchasing channels, whether online, in-store, or via sales teams.

UPI is a real-time payment system developed by the National Payments Corporation of India (NPCI) that enables instant money transfers between two bank accounts through a mobile platform. These guidelines enable non-bank entities to enter the payment aggregation business and expand their scope to include the import of services.

As the financial services space focuses on digitizing offerings for their small business customers, much of these efforts are targeting onlinebanking portals accessed via desktop. Today, he explained, small businesses often do the bare minimum to manage finances, despite the rise in FinTech platforms and products available to them.

Quality Engineering is transforming digital banking, enabling seamless innovation, operational continuity, and future-proofing in a rapidly evolving landscape. The global banking industry is currently undergoing widespread change from a regulatory and technology perspective. These large-scale projects are inherently risky.

OpenWay , a provider of digital payments technology to banks, processors, national payment switches, and mobile wallet operators, found that clients are recognising the benefits of AI. To overcome those barriers, Gen AI needs a payment processing platform with powerful data management and a 24/7 online front- and back-office.

Questions like, “What is a bank?”. It’s a fair question today, particularly as we observe the blurring of the lines between traditional banks, Big Tech and FinTechs — and as we contemplate the impact that the blurring of the digital and physical worlds has on consumers’ expectations and customer service paradigms.

At the same time, bank branch closures appear to be accelerating, with small towns across the country losing a combined 14 percent of their banks between 2012 and 2017. Many small businesses, too, are struggling to access the bankproducts they need to survive and thrive, like bank loans and deposit accounts.

This April, The Fintech Times is focusing on all things embedded finance, the integration of financial services into non-financial products and services. “The modularity, interoperability and seamless integration of BaaS have also proven to be powerful drivers of innovation in sectors beyond banking. .

He brings over 30 years experience in financial services with senior roles across global banking, private equity and accounting. He also joins the board of Quantum as director of fintech and banking, helping with its plan to list on the London Stock Exchange in 2026. Radford previously held the CEO role at Revolut UK from 2020 to 2023.

Banks are not just competing for customer engagement and retention — they are also vying for funding and resources as they overhaul their infrastructure and banking tools. The latest Digital Banking Tracker examines how legacy institutions stay competitive with challenger banks. Competition Can Lead to Innovation.

Traditionally, consumers stuck with familiar banks, but there’s now a growing trend of current account switching. The service was introduced as part of a government initiative to increase competition in the banking sector, aiming to reduce the inertia that had kept 75% of account holders with the same bank for years.

However, recent stringent regulations imposed by the Reserve Bank of India (RBI) have significantly impacted the sector, leading many fintech companies to reassess their BNPL strategies. Paytm, for example, is pivoting from its BNPL Postpaid product to focus on higher-ticket personal and merchant loans.

trillion in total assets, JPMorgan Chase is the largest bank in the US. Its retail bank, Chase, spans 61 million American households. Led by Chairman and CEO Jamie Dimon, the bank is undergoing a transformation, moving away from offline legacy systems and into the digital age. Live briefing: Consumer Banks in The Digital Age.

Whether you use Sage 50, Sage 100, Sage Intacct, or another Sage product, syncing a payment gateway with any of these systems can transform how your business accepts and manages credit card and electronic payments. and ACH/eChecks for direct bank transfers. Install the payment gateway The next step is to install the payment gateway.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content