This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This involves: Merchant onboarding: Collecting business details and verifying accounts so your users can start accepting payments. Payouts and reporting: Ensuring funds reach the merchants bank account and offering tools to track and manage transactions. Payment processing: Authorizing and settling transactions in real time.

In this article, we’ll cover what Canadian merchants need to know as they scale their businesses internationally to USA and beyond, with a focus on key considerations, challenges, and bestpractices to optimize payment processing and boost customer satisfaction worldwide.

The new proposal will allegedly strengthen FDIC-insured depository institutions’ (IDI) recordkeeping for custodial deposit accounts with transactional features. AFCs letter recommends that the FDIC withdraw the Proposed Rule and engage with industry leaders to promote bestpractices and leverage existing regulatory frameworks.

Transformation is a necessity that is hitting accounting teams worldwide. With 99% of accountants already experiencing some level of burnout and the talent shortage only intensifying that pressure adding more stress without support can quickly push them to their breaking point. But this can also lead to the status quo SALY mindset.

A study by the Federal Reserve Bank of San Francisco showed that credit cards account for 31% of all payments, significantly more than cash at 18%, and debit cards at 29%. When the funds get to your business’ bank, the bank will remove any associated fees and credit your account with the balance.

Payment Service Providers must strengthen due diligence, monitoring, and collaboration with regulators to address these risks. Financial regulators are intensifying scrutiny, highlighting gaps that PSPs must urgently address. What’s next? Previous slide Next slide What are vIBANs?

Generative AI also addresses training challenges for AI models. Moreover, synthetic data can address issues of data bias, as generative AI can create more balanced datasets that reflect a broader range of scenarios. Likewise, AI-generated speech samples enhance voice recognition, distinguishing genuine users from impersonators.

Bestpractices: Use a clear, recognizable business name and billing descriptor. To stay in good standing: Respond to disputes promptly Use pre-transaction fraud tools (3DS2, address verification, etc.) Being upfront with your provider helps you avoid unexpected holds or account freezes.

The Sage 100 system provides comprehensive tools for accounting, financial management, inventory control, manufacturing, and distribution. Additionally, Sage 100 integrations provide automated reconciliation, ensuring that transactions are accurately matched to invoices and recorded in accounts receivable (AR) without manual effort.

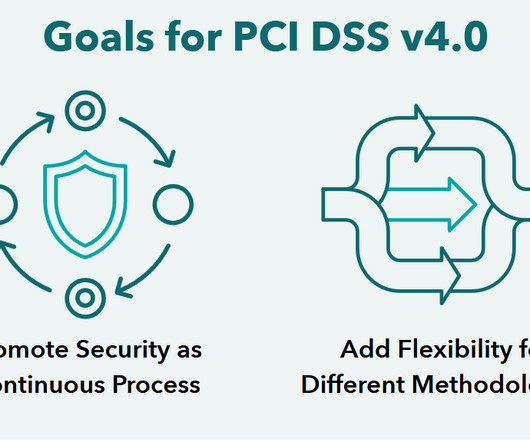

4.0 , was released on March 31, 2022, introducing enhanced security measures to address evolving cyber threats. million accounts were leaked witnessing a 388% increase in compromised user accounts. Maintaining an information security policy: Establishing a documented security strategy. The latest version PCI DSS v.4.0

Learn More What is Merchant Account Underwriting? Merchant account underwriting is the evaluation process payment processors use to assess whether a business meets the criteria for accepting credit card payments. The primary purpose of merchant account underwriting is to mitigate risks for payment processors and credit card networks.

This article outlines how to structure your chargeback management team, define roles, implement processes, select the right software, and adhere to bestpractices. Operational challenges: A high chargeback ratio could lead to higher processing fees or the loss of your merchant account.

The trend towards sustainability and especially the movement of consumers towards a sustainable lifestyle is one that the payments industry has addressed—somewhat. We highlight some practical strategies for card issuers seeking to innovate in the sustainability space and reach consumers who care about the impact of their choices.

These synthetic identities often use valid Social Security numbers belonging to children or individuals without credit histories, combined with fictitious names and addresses. However, digital banking expansion spreads risk nationwide as physical presence becomes less important for account opening.

Data breaches involving bank account details not only damage reputations and erode customer trust but can also expose organisations to direct financial loss, fraud recovery efforts, and regulatory scrutiny. Tokenisation replaces sensitive bank account information with a secure, randomised token — a placeholder with no exploitable value.

Medius , a leading provider of Accounts Payable (AP) automation and spend management solutions, has successfully renewed its ISO certifications, reaffirming its commitment to security, quality, and compliance excellence.

This legislation represents a significant shift in corporate accountability, aiming to strengthen the UKs legal framework against financial crime. Compliance requires proactive fraud risk assessment, the implementation of preventive procedures, and a culture of accountability.

The Financial Conduct Authority (FCA) has recently published its findings on how firms are using the National Fraud Database (NFD) and money mule account detection tools to combat financial crime. The review highlights both positive practices and key areas where firms must improve to effectively disrupt money mule networks.

However, as James Lichau , financial services co-leader at BPM , the accounting service provider, said, firms must be vigilant and watch over AI services so they don’t get outsmarted by ever-developing fraud tactics. “This is particularly true in the financial sector, where trust and accountability are paramount.

The process replaces your 16-digit primary account number and other sensitive data with a secure, unique digital identifier that functions exclusively within controlled environments. Regulatory frameworks will inevitably follow, converting whats currently bestpractice into compliance requirements.

Questions address both immediate challenges (transaction fees, fraud prevention, cart abandonment) and forward-looking opportunities (emerging payment methods, international expansion, technology adoption). The methodology combines quantitative analysis of operational metrics with qualitative assessment of strategic priorities.

Myths get in the way of implementing bestpractices. Take proactive steps: review their credit report, check in with their suppliers and banks, and consider a site visit if the account is significant. Many overdue accounts stem from mistakes in the sales, fulfillment, or billing process.

The aim is to enhance the protection of cryptographic key exchanges and address future cybersecurity risks that may be posed by quantum computing. MAS then published an information paper sharing bestpractices on how financial institutions can manage and ensure proper oversight when developing, testing, and using GenAI and AI models.

Improved customer experience: By addressing the reasons behind cart abandonment, merchants can enhance their overall customer experience and build trust with their shoppers. Provide guest checkout options Not all customers want to create an account or go through a registration process before making a purchase.

If counterfeit bills are deposited, banks may debit the business’s account, resulting in direct financial losses. Accounting and Reconciliation: Managing cash requires meticulous record-keeping and reconciliation, which is time-consuming and prone to errors. This speed improves customer satisfaction and operational efficiency.

Understanding these differences is essential for addressing common challenges, such as manual errors, delayed invoices, and poor payment tracking, as they can strain customer relationships, limit payment flexibility, and lead to compliance issues. Implementing an organized system, such as invoice templates or accounting software, can help.

This article explores how ISV partnerships can drive growth, key considerations when selecting an ISV partner, and bestpractices for successful collaborations TL;DR ISV partnerships help businesses access new customer segments and industries. Third-party security audits to ensure bestpractices are followed.

These fees cover the costs associated with securely transmitting payment data, verifying the transaction, and settling funds into the merchant’s account. Educate customers: Provide educational materials, customer support, or FAQs online or in-store that address common questions or misconceptions about surcharging.

Youll need to document your reviews, including any identified risks and what changes youve made (if any) to address those risks. Assigned Roles To drive accountability, youll need to assign a designated person or role to each PCI requirement. Stronger Password Rules The example above is a real new requirement for the Defined Approach.

Bonus Tip: Look for integrated payment solutions that are easily able to integrate with your related systems like your accounting software, point of sale system (POS system), CRM system, and other software. Request documentation on their security policies, fraud prevention measures, and incident response procedures to minimize risks.

A properly managed Accounts Receivables (AR) portfolio is essential to maintain the liquidity your company needs to sustain its business and grow. This requires efficient and effective collection practices, a well-trained staff, and some degree of process automation. First, Some Basics Address Emails Strategically.

Compliance is King: Navigating the Regulatory Minefield: Regulations like GDPR (General Data Protection Regulation), CCPA (California Consumer Privacy Act), HIPAA (Health Insurance Portability and Accountability Act), LGPD (Lei Geral de Proteção de Dados - Brazil) , and industry-specific mandates demand robust data privacy and security measures.

Staying ahead of how these factors influence businesses requires continuous learning and the adoption of bestpractices. Lead efforts to address operational and process issues affecting accounts receivable (AR) results and profitability. Managing a staff today is much different than just a few years ago.

The move will likely see HSBC come under increased scrutiny and accountability for hitting its net zero targets, but is this the best approach for the UK bank to take? “We weren’t comfortable with the lack of ambition and the recent watering down of accountability,” explained a spokesperson for the bank.

Communicate Goals and Results to Everyone Effective communication of goals and results is essential for driving alignment, accountability, and motivation within the organization. T ransparency fosters accountability and drives operational excellence within the organization, as teams are held accountable for delivering on their commitments.

These commonly breached records include: Personal Information Names, addresses, phone numbers, Social Security numbers, driver’s license details, passport numbers, patient healthcare records, insurance policy information, financial statements, etc. But some data types see higher breach rates than others.

TL;DR Recurring payments refer to a financial arrangement where a customer authorizes a business to charge their account at regular intervals for products or services. Recurring payments are a financial arrangement where a customer authorizes a business to charge their account at regular intervals for products or services.

An efficient accounts receivable (AR) process is essential to maintaining any company’s financial health, as it represents the money customers owe for goods or services provided on credit. What is accounts receivable (AR)? Why is the accounts receivable process important?

By the end of this guide, you’ll have `a clear overview of its operational framework, strategic benefits, bestpractices, and advanced strategies to maximize this powerful, rapidly rising payment tool. TL;DR Recurring billing is a powerful solution to streamline processes and enhance revenue generation and customer engagement.

For instance, an attacker might send an email that appears to be from a trusted video communication platform, prompting you to click on a link to verify your account or update credentials. Choose platforms that provide regular security updates and patches to address emerging vulnerabilities.

The close is one of the most critical periods in every company’s monthly (and yearly) schedule, so delays or inefficiencies can be particularly frustrating and pile pressure on accounting teams. In this article, we will look at bestpractices for enhancing your close and how automated software tools can help you reduce completion times.

Petty Cash Reconciliation: What is It, BestPractices, and Automation Petty cash, also referred to as a small cash fund, is a fixed amount of money reserved for minor expenses in a business. This report serves as a formal record of the reconciliation process and provides transparency and accountability.

In its latest bank security investigation, researches tested banking website and app security across four key criteria – login procedures, security bestpractice, account management and navigation and logout, which were amalgamated to give a total score and revealed a variety of concerns.

Sensitive or confidential data can include customer data records, bank account numbers, Social Security numbers, healthcare information, intellectual property, etc. Using this knowledge to create and update your procedures to address new threats is essential. Threat actors employ various methods and techniques to execute data breaches.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content