This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Examples include flash crashes in algorithmic trading, biased lending decisions affecting vulnerable populations, and incorrect risk assessments that could destabilise a financial institution. “Failures in the financial industry are expensive and generate low trust with consumers.

Consumers are demanding more. Today’s users expect a seamless, secure, and intelligent digital companion that helps them navigate broader aspects of their lives, from managing budgets and accessing credit to booking travel or even taking care of their health.

Key Findings Blurred Boundaries: 54% of SMBs used both business and personal credit cards in the past year; the figure rises to 61% in large cities. Card Usage Patterns: SMBs have about three active cards on average, mirroring consumer behavior. Retailers tap the highest share; personal/consumer services, the lowest.

PayPal’s BNPL solution, Pay in 4, incorporates sophisticated fraud prevention technology and machine learning models to assess creditworthiness quickly. Among other things, Sezzle is using machine learning for customer risk assessment and to offer tailored financing options.

If the goal of the Q2C cycle is to create a smooth path from invoice to cash, broken credit workflows are the potholes that slow the journey—and sometimes derail it altogether. Manual data collection : Chasing documents, verifying references, and running credit checks consumes valuable time. Different data.

Amazon Pay Later offers several benefits, including an instant decision on the creditlimit, no processing or cancellation fees, and no charges for early repayment. Additionally, users can easily monitor their spending, repayments, and creditlimit through a dedicated dashboard. Users must also be at least 21 years old.

New loan requirements are being put into place, such as boosting income verification, lowering available credit on new cards and going after consumers with higher creditlimits. American Express has already started reeling in credit offers to smaller firms, according to the sources.

Banks offer creditlimits to borrowers that would seem punitively low in much of the Western world, so there is a pent-up demand for online alternatives. The opportunity is also gigantic, Cheng told Webster, given that the country has some 800 million working adults, with less than half of them in possession of a credit card.

PeopleFund CEO Joey Kim has said that personal and consumer loans comprise about 25 percent of the loans on platform. That means the big opportunity for X Financial comes from the 400 million or so Chinese consumers who have credit cards, but are hampered by limits that are too low.

Years later, Sehgal took the concept and applied it to Try.com, which, as the name suggests, allows consumers to try clothes from eCommerce retailers online at home. To use Try.com, consumers can sign up through Google Chrome or by downloading an iOS app. The problem that it seeks to solve? Prime customers.

Zed’s innovative offering will include a no-fee credit card with features such as no hidden charges for international use, zero-interest on purchases for up to 31 days, and an advanced app with real-time transaction monitoring and security features like card freezing and unlimited virtual cards for secure online transactions.

Participants and Influencers throughout the mortgage ecosystem have been told by the three main US credit bureaus through their jointly owned and controlled credit scoring firm, VantageScore, that the VantageScore can enable millions more consumers to gain access to a mortgage. million of whom will qualify for mortgage credit.

The Commission took a black letter interpretation of the NCCP Act calling on banks to take greater steps to assess customer’s suitability and capacity for credit. Consumers looking to undertake their own search for credit will be drawn to lenders with a strong online presence and a seamless digital fulfilment process.

Build Credit “On-Ramps” One of Nubank’s most impactful initiatives has been its credit “on-ramp” program, which helps customers with little or no credit history build their creditworthiness over time. Digital banks in the APAC region should take a similar approach to innovation as Nubank.

The system got a major boost in the 1970s with the passage of The Fair Credit Reporting Act , which officially regulated what information would be collected as well as created rules that made credit reports something consumers had a legal right to both see and dispute. But is FICO keeping pace with modern financial services?

Enhancing CreditAssessment for Existing Customers. LIFECARD, a credit card company with more than 5.7 million accounts, is the first lender in Japan to adopt the FICO® Score to enhance its creditassessment for existing customers. Using the FICO Score, we can do this in a responsible and profitable manner.”.

Leading Turkish retail bank wins FICO ® Decisions Award for AI, machine learning & optimization using FICO decision optimization technology for creditlimits. However, credit loss is also affected by the assigned limits. Therefore, limit assignment is an area that we believed that would benefit from optimization.”.

Many CUs’ credit innovation plans ground to a halt when the health crisis began, however. consumers filed for jobless benefits between January and July, and even those who have remained employed are significantly altering their spending. More than 40 million U.S. expenditures to decline by $2.7 billion between January and April.

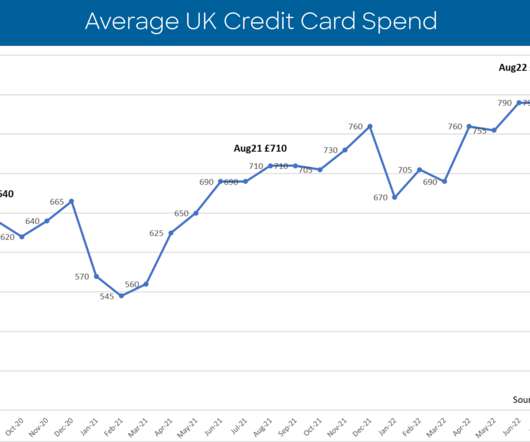

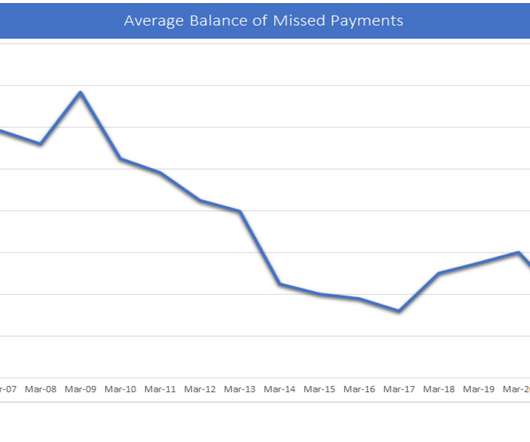

The Veteran average amount overlimit may not initially appear as a potential red flag, but when you consider that, at £5,749, average creditlimits for this segment are at their highest since at least January 2002, there are possibly some very high balance overlimit accounts that can roll into delinquency.

FICO’s report of UK card risk trends for summer 2022 (June-August) paints a picture of inconsistent consumer behaviour and market patterns which will be challenging for lenders to manage as the cost-of-living crisis impacts financial spending and consumer finances. UK Cards Report: Credit Card Payments Yet To Show Signs Of Distress.

Credit scoring is widely used in South Africa to determine the risk of credit applicants — using this kind of objective, precise measure of risk lets banks, retailers and other organizations lend with more confidence, which in turn means more people get approved for credit. About the Empirica Score.

Yelo, positioned as a neobank in the country, offers consumers a banking solution, but with the latest funding the company said it will look to introduce banking and other financial services for startups and small businesses. Yelo also plans to expand its team and invest in product development and sales, reports said.

Previously, international customers had to obtain and translate their credit reports before the application process, which was often time-consuming and potentially costly. “Improving inclusivity means rethinking outdated regulations— particularly in the consumercredit market.

Gold Loan Management System Gold loan management system streamlines the management of gold-backed loans, helping lenders enhance efficiency, ensure compliance, and optimize risk assessment. Core Capabilities of Finflux by M2P Advanced Appraiser Module : Ensures precise gold valuation with reliable and accurate assessments.

Many lenders in markets outside the US use FICO® Scores to assess the risk of consumers applying for loan, but don’t continue to monitor those consumers’ risk using the FICO Score. This regular monitoring also enables FICO analysts to identify any developing credit risk trends occurring in the Russian market.

Known internally as “Brain” (Bradesco Inteligência de Negócios / Bradesco Intelligence in Business), the decision management project has reduced the time taken to put projects into production and introduced more consumers into digital solutions, increasing digital transactions by more than 60 percent during the COVID19 lockdowns.

The multiple lockdowns from the end of March 2020 through 2021 drastically reduced consumers’ ability to spend. The average balance decreased in the first lockdown by £100 between March and June 2020 and FICO data has shown that consumers were able to pay off more of their outstanding balances overall. See all Posts. Related posts.

Even with access to credit products, the financially strained – the aforementioned consumer with less than $1,000 in the bank who suddenly has a medical emergency to the tune of $2,500, for example – find it tough going. million of those consumers revolve those balances, which have grown by 7 percent year over year.

Engage Them, Teach Them, Feed Their TikTok Obsession While many consumers are digitally savvy, they’re not necessarily financially savvy. This is something that banks should be involved with – but when Americans consumers were asked, “What is crucial to the future of your financial success?” only 1% of them mentioned banks.

Instead, Amazon has taken the core components of a modern banking experience and tweaked them to suit Amazon customers (both merchants and consumers). The partnership is significant because of its potential to put Amazon’s Quick Payment button in front of millions of consumers and boost distribution with merchants.

Consequently, issuers become limited in the differentiated product experiences they can offer to consumers. To attract new age consumers, issuers end up building custom middleware applications that offer functionalities that the legacy credit card systems lack.

’s biggest P2P lending market for consumers, announced a return to profitability earlier this month, and is currently pursuing plans to acquire a banking license that would open up deposits as a potential source of low-cost, high-stability funding. “We Zopa, the U.K.’s Concerns About Hidden Risk. And public response from the U.K.

That is our mantra for FICO’s Score a Better Future program because we want to empower consumers to reach their financial goals. As such, we have put together a list below of the top 10 credit scoring topics and/or questions that surfaced (along with answers) in the program. Want to learn more about credit scores? No worries!

And because the majority of credit bureaus rely on Companies House data to assess SMBs, there is a “significant gap in which a company’s position may change dramatically, and that change will not be reflected in their credit score.”. At best, information from Companies House, the U.K.’s s registrar of companies, is outdated.

Order validation and approval: The captured order details are validated based on predefined criteria such as pricing, discounts, inventory availability, and customer creditlimits. Analyze Time-consuming manual data review. Conduct periodic audits and risk assessments of automated order processing systems.

Limited integration options with accounting systems. Setting up and monitoring processes within the platform can be time-consuming and challenging, despite its user-friendly interface. Cons of Brex: Some users find it confusing to transfer funds between the credit card and bank side. Sources: [link] [link] 7.

Goldman Sachs is being investigated for gender discrimination related to the algorithms it uses when deciding on creditlimits for the new Apple Card. As soon as this became a PR issue, they immediately bumped up her creditlimit without asking for any additional documentation,” he said, according to Bloomberg. “My

The problem, Petal co-founder and CEO Jason Gross told Karen Webster, is that it leaves around half of all Americans with only a few options: a credit card with expensive strings or no credit at all. Petal wants to change the math on how consumers gain access to credit – and turn the tables on how creditworthiness is assessed.

On May 10, the Consumer Financial Protection Bureau (CFPB) issued a Request for Information (RFI) seeking to learn more about the small business lending market. The CFPB was created to regulate those engaged in offering or providing consumer financial products or services.

Elsewhere, consumer confidence hit an 11-month high as the end of lockdown loomed alongside clear progress following the roll-out of the nation’s mass vaccination programme. As a result, the true level of financial stress on industry, commerce and consumers is still unclear. But is the optimism masking the true picture? Phased Changes.

These digital banks are revolutionising how financial services are delivered to consumers and businesses alike, leveraging technology for convenience, innovation, and accessibility. Consumer demand for more convenient, cost-effective banking solutions has driven this shift towards digital banking.

What is a credit card hold? A credit card hold is when a portion of your creditlimit is reserved for a potential transaction. Credit card holds are enforced by merchants, payment processors, credit card networks, and card-issuing banks. If this hold is lifted, it will free up your creditlimit again.

Credit utilization ratio The credit utilization ratio measures how much of a companys or individuals available credit is being used. Its commonly used in both business and personal finance to assesscredit health and risk. A lower ratio generally indicates better credit health and a stronger ability to repay debts.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content