This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If you run a business, youre aware of the basic fees for accepting credit card payments. depending on the credit card. increase in fees can mean thousands of dollars lost each year for a business making steady credit card sales. Assessment Fees What It Is: Charged by the card networks (Visa, Mastercard, etc.)

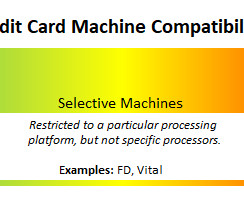

Some credit card machine companies also provide merchant accounts, while others are solely equipment manufacturers. This article is specifically about credit card machine companies, not the machines themselves. Well take a look at why that matters and give a rundown of the major equipment providers in the United States.

If ever there was a time to kill the check, that time would be now. The remaining tens of millions, those who do not have direct deposit payment information on file with the IRS … will have to wait for the proverbial (paper) check in the mail. There also is Mastercard Send for push payments as an alternative to ACH.

To that end, Visa announced Tuesday (April 2) that it has introduced Card Payouts, an app designed help mid- to large-sized businesses manage cash flow — and speed payments to gig economy workers, to boot. The app is built to support card capture, tokenization and card-on-file transactions, Visa said on Tuesday.

Thats why 92% of consumers and 82% of companies reportedly made the switch to electronic payments, like Electronic Funds Transfers (EFT) and Automated Clearing House (ACH). Checks can bounce, and cash can get lost. EFT and ACH offer more security and convenience than cash and checks, but they also come with limitations.

As Laura Valdespino , director of compliance solutions at ADP , told PYMNTS in a recent interview, using digital channels, and specifically, pay cards, can actually improve the employees’ pay experience over paper-based methods that have been in place for decades. As Valdespino said, “The employees don’t want to wait for the check.

The COVID-19 pandemic has produced one ray of sunshine amid otherwise devastatingly dark clouds: Consumer credit scores have improved in recent months to the point of hitting a new record high, the Wall Street Journal reported Sunday (Oct. For many years, consumers have been credited with driving about two-thirds of U.S.

This shiftis not merely a matter of convenience; it is emblematic of an increasingly complex convergence between state-of-the-art technology, consumer desires for seamlessness, and the regions particular socio-economic landscape. In 2023, credit card payments comprised 52.2% of all cashless transactions in Japan.

While paper checks are increasingly passing into the realm of consumers’ memory, there are certain niches where they have managed to hold on, even as the rest of the world tries rather adamantly to move on. We’ve known for more than 10 years that there are issues with mailing checks, which is why we’ve seen over 4.5

Between the explosion of the digital economy driven by the pressures of the pandemic and the radical realignment of consumer preferences that has happened as a result, the year 2020 has seen digital payments accelerate at something approaching warp speed. It’s a consumer choice, [offering] everything and anything they want,” Turner said. “We

As consumers, most of us have looked at last month’s credit card statement and experienced the panic of not recognizing a charge. But credit card chargebacks also occur for a variety of other reasons and they’re not always honest. What Are Credit Card Chargebacks?

Checks, despite their near extinction in consumer payments, remain alive and well when it comes to businesses paying each other. The check – for its many, many flaws – does address all three of those aspects. The check – for its many, many flaws – does address all three of those aspects. But that isn’t all it needs to do.

In an effort to kill the check — where B2B payments are anything but efficient — might virtual cards be the answer? As ePayables have emerged as an option in the commercial realm, Yarbrough noted that a virtual card can solve problems for both buyers and suppliers. The Friction Points Hindering Adoption.

consumers don’t exactly love the paper check — roughly 38 percent report that they’ve stopped using them entirely, and that shoots up to almost 50 percent when talking about millennials. Consumers [want] electronic access to their funds that is easily accessible and frictionless.”.

It was developed to provide an alternative to the current transaction models, including checks. It takes consumer data to make PIX work. He said existing instruments will have to live together to allow consumers to decide what works best for them. Real-time payments continue to gain traction around the world.

A partnership between Featurespace and OrboGraph will help banks and other financial services companies defend themselves against check fraud. Many consumers, especially younger consumers, have abandoned paper checks. Many consumers, especially younger consumers, have abandoned paper checks.

Consumers love the opportunity to get paid instantly when they can. But with innovation comes risk — and anything that consumers use will always attract fraudsters looking to steal a cut of the action. . There is nothing Venmo can do to stop a consumer from willingly sending their money to a crook,” Edwards said. .

And there’s the paper check — a 1.0 Checks have a long and frequently complained about history of being both slow and costly — a friction-filled paper-based payments method. It may be a three week end-to-end process, but every enterprise is set up to pay by check – and every consumer knows how to cash one.

One of the biggest trends in fintech today is the rise of digital banking products like mobile checking accounts and new debit cards. From Square to Paypal, a host of fintechs are creating products that let consumers spend money directly out of digital accounts using a physical card. get the 86-page fintech report.

The proposed credit card interest rate cap legislation , courtesy of Democratic presidential hopeful Senator Bernie Sanders and Rep. Alexandria Ocasio-Cortez is in serious need of an almost half-century-old refresher course in the unintended consequences of price caps on the American consumer. Here’s why. A 46-Year-Old History Lesson.

Consumer Payments Study. While this year’s findings highlight the strides the industry and consumers have made towards digital payments, they also underscore how existing behaviors and patterns remain very much intact. Consumers still love their cash. That’s the key takeaway from the sixth year of TSYS’ U.S. Cash Holds Steady.

But it will take a mindset shift on the part of merchants and consumers — and a return of foot traffic to the stores, of course. As Platko said, the data show that consumers are willing to try something different when it comes to payments, chiefly to avoid touching things. As Webster noted, consumers like their cards.

These efforts include TCH’s efforts to connect financial institutions’ (FIs’) core banking systems to the company’s Real-Time Payments (RTP) network, along with what card networks and FinTechs are doing to enable real-time push payments to receiver bank accounts. Real time is getting ever closer to prime time.

Consumer engagement has become a very different ballgame for financial institutions (FIs) in the past several months, as the physical branches that were the cornerstone of making connections with customers closed down. More generally, financial institutions are now in the position of having the highest [level of U.S.

Businesses of all sizes are doing their best to stay on top of changing payment trends and consumer expectations as the pandemic continues to impact how money is moved. Using digital push payments can also help add security to B2B transactions, thanks to the cybersecurity measures that can be grafted into these processes.

Dubai First , the consumer services platform under First Abu Dhabi Bank (FAB), has become the first issuer in the region to leverage Mastercard Token Connect to push customers’ tokenized card details from its mobile app to Click to Pay and digital wallets.

You’ve likely noticed that acquirers are actively pushing back on allowing merchants to offer a negative option, upsell, or cross-sell on payment pages. This is where an additional offer on the payment page has a pre-checked cross-sale. There’s been a lot of talk about changes to cross-sales and checkout pages.

In an interview with PYMNTS, Scott Young , VP of Innovation at PSCU , noted that in the changing consumer environment, digital and mobile banking are “table stakes,” but credit unions (CUs) must be conscious of how member payment preferences are evolving. Stepping Up On Credit . More Comfort Online .

Live briefing: Consumer Banks in The Digital Age. Learn about the playbooks of today’s top banks as they digitally re-position their consumer products. This trend towards digitization is already starting to play out as fintechs circumvent banking licenses by partnering with issuing banks to offer checking account-like products.

While new regulations will help push the market in the right direction, it is already in banks’ hands to make Open Banking work and allow their customers to share their financial data and tap into the benefits that Open Banking creates, says Stacey Wilkinson, API Growth Manager at NatWest. That’s going to be quite hard to shift,” says Wright.

Apple has added a new one-click payment option to its online store for users of the Apple Card , according to a 9to5Mac report. That means users can use ApplePay to check out more easily. Those using the card can now check out by just clicking the option for the Apple Card when buying something through the Apple online store.

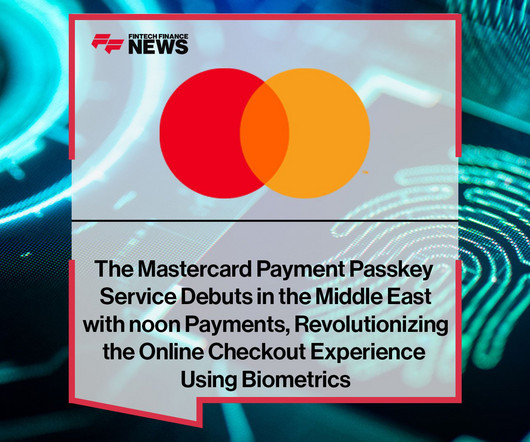

The Mastercard Payment Passkey Service streamlines e-commerce and revolutionizes the consumer journey. The Mastercard Payment Passkey Service streamlines e-commerce and revolutionizes the consumer journey. They offer consumers the peace of mind that they will not lose or inadvertently share their password or OTP.

Government agencies fall among the cohort of institutions that need to disburse funds with more speed than usual, but they’re tasked with sending stimulus checks and business loans to the financially vulnerable, making the stakes higher for those who fail to quickly respond to these pandemic-driven changes.

Delivering funds smoothly to employees in different nations is therefore essential, and it may require firms to migrate from paper checks to digital tools, especially those that suit the needs of employees who do not have bank accounts. Around The World Of Smarter Payments.

There have also been shifts in how customers pay for goods and services, with s ocial distancing policies making contactless transactions essential and pushingconsumers toward payment methods such as bank transfers and digital wallets. Each company’s risk management approach must therefore be tailored to its specific business needs.

The payments ecosystem now prizes quickness above all things in a time of cash flow shortages, where each paper check takes an eternity — assuming it arrives at all. Clearly, paper checks aren’t cutting it anymore. To paraphrase the movie “Top Gun” … “We feel the need … the need for speed.” We’ve evolved.

Morgan have recently announced a partnership aimed at facilitating the transition from checks to digital payments for major banks in the United States. This collaboration has resulted in the launch of Codat’s new Supplier Enablement API product, designed to increase virtual card usage, with J.P. Stephen Markwell, J.P.

Consumers go on a lot of different types of digital journeys in a day — they might shop online, do some banking, move funds between accounts, do some light online browsing. The context is important, because of course the services offered to the consumer vary by use case,” Schulte noted. Tapping Into Personalization. The problem?

For many AP teams, the paper check has presented immediate challenges with staff no longer able to step into the office to print and send checks (and no one on the accounts receivable end to accept them). Visa Enables Commercial Push Payments For KyckGlobal. Just which payment rail they will migrate to, however, remains unclear.

The digital shift brought on by the coronavirus has caused treasury banks to reprioritize their support of digital payments as consumers and merchants increasingly demand fast, easy and secure ways to get their money. The Value Proposition.

In a nutshell: Companies (and even consumers) “hire” goods or services to get where they want to go, to make progress, to satisfy goals. The great digital shift is upending B2B payments , pushing them away from the age-old reliance paper checks toward digital options. Beyond The Safety Factor . Size-Agnostic Ripple Effect .

And even if it doesn’t quite make it over the trillion-dollar milestone, consumer spending will certainly get within striking distance – which attests to the fact that in the U.S. During the Black Friday and Cyber Monday shopping events and beyond, consumers were increasingly turning to buy now, pay later (BNPL) solutions in the U.S.

Real-time payments are currently among the hottest trends and topics in the payments industry — a source of significant investment and regulatory attention, as financial institutions and other players strive to meet consumer demand for faster money movement. Common forms of pull payments, meanwhile, include debit cards and paper checks.

The great digital shift is transforming credit cards into money management tools. Consumers want cards, and they want them quickly, and they want those cards [delivered] in a digital way," said Turner. The company said that through the expansion of its Digital-First Card Program, which was announced last Wednesday (Sept.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content