This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

However, this rapid growth brings significant regulatory challenges, primarily in balancing the need for innovation with the imperative of consumerprotection. Consumerprotection is not just a regulatory requirement : it is a fundamental right that must be safeguarded amidst advancing technology.

Participating policyholders are protected by restrictions on profit allocation to shareholders. Regarding employees, while MAS doesn’t regulate employment decisions, it expects fair treatment and compliance with employment laws.

The Consumer Financial Protection Bureau is looking into how it can apply existing privacy and consumerprotectionslaws to emerging digital payments offered through Big Tech, as well as stablecoins and other cryptocurrencies.

“This massive surge in mobile wallets demonstrates a clear shift towards digital payment solutions, reflecting the evolving preferences of consumers for faster and more secure payment options. Australians have always been at the forefront of adopting new digital technologies, and these latest figures show that banking is no exception.

The Consumer Financial Protection Bureau (CFPB), the consumerprotection agency in the US, has hit Equifax with a $15million fine, after it found that the nationwide consumer reporting agency failed to conduct proper investigations of consumer disputes.

Divergence from common law jurisdictions According to the TPA response, the Bills approach could set the UK apart from other major common law jurisdictions, including Singapore and Australia. Both countries have opted to integrate digital assets into existing property law frameworks instead of creating separate categories.

In parallel with growing market adoption of surcharging, more states have considered and enacted surcharging legislation, often with the stated goal of standardizing surcharging and ensuring consumerprotection. In 2024 alone, more than a dozen state legislatures introduced bills related to surcharging and consumer fees generally.

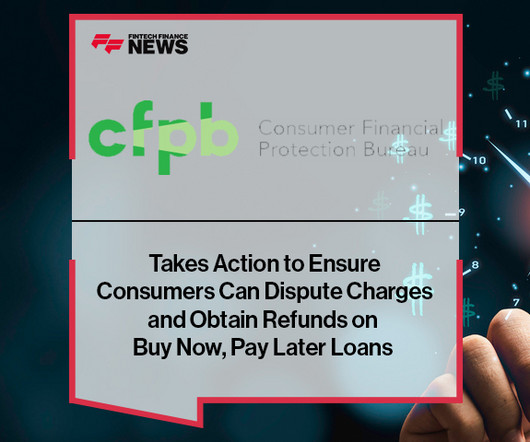

A report this month from the organization outlines a litany of complaints about buy now-pay later, such as hidden fees, and suggests the industry is trying to evade consumerprotectionlaws.

Axios reported the investigation is examining Apple’s possible use of deceptive trade practices that may have broken consumerprotectionlaws. Paxton may sue Apple for violating the state’s deceptive trade practices law in connection, Axios reported. It also reserves the ‘tap and go’ functionality of iPhones to Apple Pay.

The FCA’s proposed safeguarding reforms for payments and e-money firms, aiming to enhance consumerprotection and operational compliance. The reforms ensure robust safeguarding practices, bolster consumer trust, and address risks like fund shortfalls during insolvency. Why is it important? What’s next?

It highlights the need for a strategic, proportionate approach to safeguarding that aligns with broader regulatory and consumerprotection goals. Nonetheless, in practice, the interaction of segregation requirements and insolvency law is often a key focus of insolvencies. Why is it important? What’s next?

The court said the Dash buttons, which are small, Wi-Fi-connected devices that reorder items like laundry detergent and coffee, breaks consumerprotection legislation because it doesn’t give consumers enough information about the product or its price. There should be unambiguous wording, such as ‘order and pay.’”.

Curve , the ultimate digital wallet, has become the first to offer section 75 protection on purchases made through its Wallet. This is a step change in consumerprotection, allowing users to make payments without worrying about losing money if a product is faulty or if theres a problem with the purchase.

As global online shopping grows rapidly, consumers expect seamless payment experiences. Key regulations include: GDPR (General Data Protection Regulation) : For merchants targeting Europe, GDPR compliance is mandatory, emphasizing data privacy and protection.

In the UK, consumers and businesses make around 1,500 transactions every second. The PSR (Payment Service Regulation) complements the Payment Service Directive, leading to directly applicable law in all EU states. The payments ecosystem in the UK and EU is in constant flux, driven by regulatory guidance and technological advances.

Hasan Fawzi, OJK’s Chief Executive for Financial Sector Technology Innovation and Crypto Assets, emphasised the sandbox’s importance in preventing fraudulent schemes and enhancing consumerprotection. Products or business models failing to pass sandbox approval will be deemed illegal.

Australia will introduce new legislation to amend the Credit Act, requiring Buy Now, Pay Later (BNPL) providers to hold an Australian credit license and comply with existing credit laws regulated by the Australian Securities and Investments Commission (ASIC). The new laws aim to balance consumerprotection with innovation and competition.

The agreement, issued last week, addresses “shortcomings” in Discover Bank’s compliance management system for consumerprotectionlaws, the company said.

It underscores the need for payment firms to balance AI innovation with robust privacy and regulatory compliance to protect sensitive consumer data. Payment data is inherently vulnerable because its compromise can have significant financial and personal consequences for consumers. Why is it important? What’s next?

In the world of digital payments, fraud is an ever-present threat that continues to evolve, creating serious risks for both businesses and consumers. This can be attributed to the increasing sophistication of fraud detection tools, improved authentication measures, and greater consumer awareness of phishing scams.

“Whether a shopper swipes a credit card or uses Buy Now, Pay Later, they are entitled to important consumerprotections under longstanding laws and regulations,” CFPB Director Rohit Chopra said.

Section 75 is a law that applies exclusively to credit cards, ensuring providers share responsibility with merchants for purchases ranging from 100 to 30,000. Debit card users have historically not had this level of protection, leaving them vulnerable in cases of faulty goods.

It would instead offer payment companies a national servicing platform to replace the regime of state regulations such firms would be subject to under existing laws. Commercial companies accessing a payments charter would avoid oversight and regulations that protect the financial system and consumers,” the bank industry leaders wrote.

The Consumer Financial Protection Bureau (CFPB) has issued an interpretive rule that confirms that Buy Now, Pay Later lenders are credit card providers. Accordingly, Buy Now, Pay Later lenders must provide consumers some key legal protections and rights that apply to conventional credit cards.

OJK acknowledges the valuable input from these stakeholders and is refining the LPBBTI industry regulations as part of its mandate under Law Number 4 of 2023 concerning the Development and Strengthening of the Financial Sector (UU P2SK).

BNPL (Buy Now, Pay Later) burst onto the scene as a game-changer, transforming how consumers shop and pay over time. What started as a consumer-friendly alternative to traditional credit is becoming a more concrete financing solution in the digital payments ecosystem, particularly in emerging markets like BNPL regulation in Asia.

The Consumer Financial Protection Bureau has once again made it clear that new AI- and machine learning-based technologies are held to the same consumerprotection regulations as established technologies.

South Korea In June 2023, South Korea enacted the Virtual Asset User Protection Act, marking its inaugural comprehensive digital asset law. The Act is notably focused on consumerprotection, imposing stringent penalties for market misconduct and manipulation. This development followed the 2022 collapse of Terra.

Hasan Fawzi Hasan Fawzi, the Chief Executive of the Supervision of Financial Sector Technology Innovation, Digital Financial Assets, and Crypto Assets at OJK, highlighted the initiative’s role in enhancing consumerprotection and education.

These products and services are safe, highly secure, and promote financial inclusion by allowing consumers and small businesses including lowandmoderate income consumers who have historically not had full access to the financial system to conduct their everyday financial transactions.

The Consumer Financial Protection Bureau (CFPB), a US government agency responsible for protectingconsumers in the financial sector, has ruled that buy now, pay later (BNPL) lenders must treat consumers as credit card providers do, ensuring they receive the same key protections. Are consumersprotected?

regulators acknowledge that although there is a market and demand for open banking, the current regulatory structure prioritizes consumerprotection.”. Merchants are central to this plan, as are banks, for their deep knowledge of consumers. Don’t let the lack of hard law in the U.S. One need only look to the U.K.

The Indonesian Financial Services Authority (OJK) is closely monitoring Investree , a fintech peer-to-peer lending platform, following public reports of potential operational and consumerprotection violations.

Two years after a consumerprotectionlaw changed how banks and other companies handle customer information, a new proposal aims for more sweeping reforms.

As more jurisdictions refine regulations and expand open finance frameworks, the focus will shift to interoperability, consumer trust, and cross-industry data integration. Ultimately, this convergence fosters a more inclusive and efficient financial ecosystem, benefiting consumers and businesses alike. What’s next?

The rule changes provide stronger consumerprotection but also raise concerns about industry costs and potential fraud exploitation. Collaboration between regulators, law enforcement, and the counter-fraud community is needed to ensure the effectiveness of the reimbursement scheme and to mitigate emerging fraud risks.

While convenient for businesses and some consumers, this model raises questions about transparency and consent, which well explore next. Canada, the UK, the EU) have their own frameworks, often with similar consumerprotection aims. Make Cancellation Easy Avoid creating complex or time-consuming cancellation processes.

The small nation is making a big push in support of FinTech innovation by reforming its payment laws. Singapore is preparing for a FinTech revolution. “It would also give MAS the flexibility to address emerging risks, such as cybersecurity, interoperability, technology and money laundering and terrorism financing. .

Licensees, exchanges, and other market participants should prepare to comply with the listing, disclosure, capital, and other requirements that the new law imposes. Market participants should therefore evaluate their path to compliance with the law as enacted, but should also expect further refinements from the DFPI in the coming 18 months.

The regulation outlines the framework for PKA operations, including institutional requirements, governance, data security, and consumerprotection. This is expected to benefit individuals and small businesses with limited traditional credit histories.

3 types of refund and cancellation policies For businesses, clear refund and cancellation policies can lead to greater consumer trust and fewer disputes. Legal advice: Legal experts can help clarify terms, avoid vague language that may lead to misunderstandings, and ensure that the policy aligns with applicable refund and return laws.

A spokeswoman from the European Commission told Reuters that national authorities are responsible for enforcing the EU’s rules pertaining to data and consumerprotection. “The problem is always the lack of transparency and the notion of consent,” Tarabella explained.

While the payment industry and financial institutions are uniquely positioned to tackle financial crime, current regulations don’t go far enough to fully eliminate the risk of illicit financial flows – and consumers are starting to take notice.

Striking the Balance Between ID Management and Data Protection In the digital age, where data drives everything from marketing strategies to AI algorithms, a growing number of citizens are worried about the protection of their personal data. Fines for non-compliance can range from $2,500 to $7,500 per violation.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content