This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

It provides access to game credits, gift codes, and vouchers using familiar local payment methods such as mobile carrier billing and e-wallets. billion digital asset, Web3 WeLab 1 billion digital banking, lending Micro Connect 1.7 Coda Valuation: $2.5 Airwallex Valuation : $5.5 Company Valuation ($) Segment HashKey Group 1.3

Think about how easy it is to order a ride on Grab, book a hotel on Agoda, or pay for groceries on Shopee without even needing to pull out your creditcard or open a banking app. The region has become a hotbed for embedded finance, thanks to its mobile-first economy and digitally savvy population.

The pandemic has exposed the pain points of all verticals when it comes to payments, and especially when it comes to transacting in person, in a tactile environment, with cash, and where banking conduits are limited. Banks have been inching into the space; cash still remains a hallmark. Looking Toward Underserved Markets .

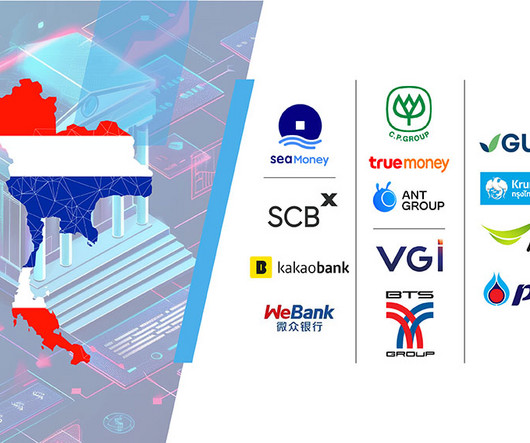

Thailand is moving closer to welcoming its first virtual banks, with the Bank of Thailand (BOT) currently accepting applications for the virtual banking license. With the deadline looming on the 19th of September 2024, speculations are rife for Thailand’s virtual banking license applicants.

As businesses and consumers become more comfortable using creditcardsonline, the proportion of US commerce that takes place online has steadily increased over the last 20 years. Stripe really did come about because we were really appalled by how hard it was to charge for things online.” — John Collison.

India’s remarkable BNPL growth has been driven by its low creditcard penetration and limited access to formal credit, coupled with a booming e-commerce market that has been fueling demand for BNPL services. in 2019 to an estimated 5.8% in 2023, according to GlobalData.

Traditional banking products, including checking, credit, and savings accounts, are under threat from a new crop of digital-first startups. Many of these startups are launching products without a bank charter and targeting a very specific customer base. DOWNLOAD THE 61-PAGE consumer banking REPORT. savings accounts.

Cash Usage Decline : The World Bank reported that cash usage in advanced economies declined by nearly 50% during the pandemic, with consumers opting for digital and contactless payment methods instead. Consumers quickly embraced mobile wallets and tap-to-pay cards, driven by the desire to minimize physical contact during transactions.

At the forefront of payment industry, particularly in creditcards, are two giants: Visa and Mastercard. Bank of America launched the BankAmericard in 1958, widely considered the first creditcard available to consumers, which eventually evolved into Visa. UnionPay has 32% of the global creditcard market.

Banks offer credit limits to borrowers that would seem punitively low in much of the Western world, so there is a pent-up demand for online alternatives. The opportunity is also gigantic, Cheng told Webster, given that the country has some 800 million working adults, with less than half of them in possession of a creditcard.

India-based Paytm Payments Bank not only wants to become the world’s largest digital bank , but also to evolve into a financial services company providing a slew of services like wealth management and trading. 28), Paytm founder Vijay Shekhar Sharma said the company is aiming to have 500 million bank accounts.

In 2022, the country was home to 993 active fintech companies, representing about 25% of all fintech ventures operating across the ASEAN region, data from a 2022 report by the United Overseas Bank (UOB), PwC Singapore and the Singapore Fintech Association (SFA) reveal. billion to US$15 billion during the period. in July 2023.

Privacy.com’s service allows users to create virtual, disposable payment card numbers for no cost. Its intended use is to combat the widespread fraud and scams going on in relation to digital payments, and can let users cut off some companies from their bank accounts.

Lenders are looking for new ways to connect with the estimated 3 billion people worldwide who fall outside the credit mainstream. These “credit invisibles” don’t have creditcards, bank accounts or credit history — so how can a lender assess their risk? those with a credit history.

Clearly, the opportunity of consumer choice has led to more volume, and perhaps even volume that is tied to more margin-favorable debit (and not credit) products. Moreover, Schulman noted, One Touch has so far made a lot of headway against the sort of blessing/curse nature of mobile for merchants. Even analysts agree.

To overcome that, Grab, along with Mastercard, will issue virtual and physical prepaid cards directly from the Grab app. Customers can add cash to the card to spend at any merchant, online and offline, where Mastercard is accepted around the world.

Nicky Senyard, CEO and founder of Fintel Connect “Developing countries are actually great places for new ideas because they often don’t have traditional banks. This shift has led to a bunch of great advancements in mobilebanking and money apps, making it possible for financial services to reach even the most remote areas.

The following post will define fintech, discuss the types of companies involved, and comment on how this new industry fundamentally changes the face of banking, investment, and doing business. This has come to mean everything from banking and insurance to investments. .” But what is fintech? What Does Fintech Mean?

So with no further ado, here are the Best of Show winners for FinovateSpring 2015, in alphabetical order: Alpha Payments Cloud , for AlphaHub , its omni-channel solution access platform that helps banks, merchants, MSPs, and ISOs gain access to any solution provider in the world.

Akulaku – US$2 billion Indonesia’s most valuable fintech startup is Akulaku, an onlinebanking and digital finance platform valued at US$2 billion. Founded in 2016, Akulaku provides digital banking, financing, investment and insurance brokerage services, targeting financial underserved demographics.

When we were thinking about entering retailer financing, there was a huge underserved population of merchants and consumers, because there were many many merchants that didn’t have access to financing programs. Once the customer is approved for credit, the merchant processes it just like any other creditcard payment from Visa.

The cohort of college students and those five years or so out from graduation is roughly 30 million people — all of whom are falling into the short credit history/limited work history hole that is locking them out of access. However, that, as happened in banking, is breaking down.

These companies are making it easier to make a budget, invest, and buy stocks, as well as to get loans and creditcards. How Level Money designed itself specifically for a mobile-first experience. How Credit Karma built a $500M business by helping people. They have a deep antipathy to traditional financial institutions.

Quickbooks Online QuickBooks Online tends to be the “go-to” name in AP automation across a wide field of BILL competitors, mostly by virtue of its size and overall brand penetration across a range of finance and accounting functions. This tier allows up to ten users. 4 ERP Integrations 4 4.5 4 User Experience 4.5

Today’s consumers are much less tolerant of not being able to access a card or mobile-backed payment when they want one, and the expectation of carrying cash is becoming increasingly foreign. Banks can be reluctant to take on small players, generally preferring to work with larger, more stable and secure enterprises.

May 2015 demo : Alpha Payments Cloud showed AlphaHub , its omni-channel solution access platform that helps banks, merchants, MSPs, and ISOs gain access to any solution provider in the world. October 2015: Partnered with Macquarie Business Banking. December 2015: Offered quick login on mobile. HQ: Singapore. Founded: 2012.

This includes digital platforms, software, and applications that offer financial services such as mobilebanking, peer-to-peer (P2P) payments , online lending, and investment management. Key features of the fintech experience include mobile-first interfaces, 24/7 accessibility, and tech-driven personalized services.

In the wake of the outbreak, everything from doctors appointments to schooling to workouts went online. As more people have worked, learned, banked, exercised, relaxed, and even sought medical care from home during Covid-19, they have gotten a crash course in just how much can be accomplished at home. Online courses & content.

However, there are many startups in the CB Insights database who are targeting underserved populations, providing healthcare, financial, or energy services tailored to these consumers’ specific needs. Consumers with poor or no credit can apply for and receive small short-term loans. Endless mobile. Select Investors: N/A.

The rise of technology has given rise to online networks, which of course has given rise to individuals sharing all manner of information, from selfies to more serious fodder. Within the digital community across B2B, said Williams, such data shared most effectively, vis real-time processes, is “underserved.” And when is it needed?

Commercial Banking: How JP Morgan’s chatbot saves the company 360,000 hours a year. Customer journey: Using chat to get people from online to brick-and-mortar. At the most rudimentary end of the spectrum, there are the bots that banks use to prompt callers through a phone tree, telling them to say “yes,” “no,” “check my balance,” etc.

The digital banking landscape in Singapore has undergone a rapid transformation, with four players gaining approval from the Monetary Authority of Singapore (MAS). Last Updated: 11 February 2025 What Are Digital Banks? Consumer demand for more convenient, cost-effective banking solutions has driven this shift towards digital banking.

With a vast infrastructure, Moneris services hundreds of thousands of businesses across Canada, offering everything from point-of-sale (POS) terminals to e-commerce integration, with strong banking relationships and deep compliance capabilities. It supports all common integrations for web, mobile, and in-person transactions.

Imagine a world where you never have to step into a physical bank again. With the rapid rise of digital banking, millions are now managing their finances seamlessly from their smartphones. But with so many options available, which digital banks are truly leading the charge in 2025? What is a Digital Bank?

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content