This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For many small business owners, creditcard processing fees may seem like a hefty price to pay for providing convenience to customers. Even if you consider them to be a cost of doing business, creditcard fees can quickly eat away at your already slim profit margins. Let’s get started.

As consumers, most of us have looked at last month’s creditcard statement and experienced the panic of not recognizing a charge. But creditcard chargebacks also occur for a variety of other reasons and they’re not always honest. What Are CreditCard Chargebacks?

Accepting creditcard payments at your business is a surefire way of increasing customer satisfaction and retention. Over 80% of American adults owned at least one creditcard in 2023. Also, creditcards contributed to 27% of the spending at point-of-sale (POS) systems worldwide. Don’t believe it?

Since managing creditcard transactions can be complex, understanding how their settlements work is essential to maintaining financial health as consumer spending rises. Creditcard settlements involve various processes and parties that ensure transactions are accurately recorded and funds are transferred.

Singapore’s government has clarified that the Shared Responsibility Framework will not apply to creditcard fraud cases, citing existing robust protections for consumers. This clarification came in response to a parliamentary question on the prevalence of creditcard fraud in the country. million each year.

While major cardissuers such as Chase and Wells Fargo roll out NFC-enabled credit and debit cards incrementally, Bank of America is taking much more aggressive approach.

Are you struggling with resource constraints caused by soaring creditcard processing costs? Creditcard surcharging can help offset these expenses, but it can be tricky. TL;DR Creditcard surcharging involves adding a fee to transactions with creditcard payments, offsetting processing costs.

Marqeta , the global card issuing platform, debuted its new Tokenization-as-a-Service (TaaS) product, which allows cardissuers to access its tokenization technology, the Oakland, California-based company announced on Tuesday (Sept. It is used to instantly provision cards into a mobile wallet.

Safety-minded consumers the world over can now be seen tapping contactless cards, scanning QR codes or utilizing voice ordering technologies to make purchases without potentially putting themselves or others at risk of contracting the virus. The Beyond The Card: Toward The Cardless And Contactless Future report, a PYMNTS and i2c Inc.

As consumers have been hit hard by the economic effects of the COVID-19 pandemic, cardissuers have seen a sharp impact to their business. In the immediate aftermath of the pandemic that pushed workers into indefinite furloughs and unemployment, creditcard transaction volumes plunged by 30 percent.

The proposed creditcard interest rate cap legislation , courtesy of Democratic presidential hopeful Senator Bernie Sanders and Rep. Let’s hop into the time travel machine this Monday morning and go back to the year 1973. Here’s why. and other countries) over political differences. Gas station operators followed the government’s rules.

But despite the COVID pandemic having effected massive changes in the ways consumers transact, creditcard fraud is still a “thing,” and a big, ever-changing thing at that. Exactly how big creditcard fraud is depends on where you look. Creditcard fraud was the FTC’s second most-reported fraud type in 2019.

In an era defined by digital transactions and cashless payments, the process of paying for goods and services is more convenient, and increasingly reliant on creditcard transactions. However, as the popularity of creditcards and digital wallet payments continues to surge, the costs associated with accepting them also do.

As the UK’s Financial Conduct Authority proposes that issuers reduce or waive interest rate charges for persistent creditcard debt, it raises the question: Just how much creditcard debt do Britons carry? Veteran (5+ years on book) has the highest % of unused credit on accounts which are spending.

In a press release , ICBA Bancard said the partnership with MK Decision streamlines its creditcard application process to make it easier for customers when shopping and applying for cards. Our mission — to stimulate local borrowing and local lending — is well aligned with ICBA Bancard and its community bank clients.

The Electronic Payments Coalition (EPC) released a new explainer document highlighting why retailers and their trade associations have historically pushed for greater usage of creditcards. Despite a recent campaign from some of the loudest voices in retail, creditcards have increasingly become the preferred option of commerce.

According to creditcardissuers, about 24 percent of recurring transactions from creditcards are falsely declined , which adds up to about $300 billion in lost sales in the U.S. It then uses the data to “optimize creditcard recovery,” ultimately pushing the transactions through. ”

In today’s competitive landscape, implementing a card product can be a powerful addition for businesses looking to enhance customer loyalty, streamline expenses, or broaden their financial offerings. Designing and launching a debit or creditcard product requires navigating a complex web of stakeholders and intricate processes.

If your company accepts creditcard payments ( which it should ), chances are, you’re going to be affected by Visa’s interchange rates. cards currently in use. So it’s virtually impossible for a business to not accept Visa cards. TL;DR Interchange rates are the fees charged by creditcard networks.

Visa , the creditcardissuer, announced Thursday (May 4) that it will help its financial institution partners create customized digital card management services for their customers. These capabilities will be available for issuing partners to provide to their cardholders through their online and mobile banking channels.

It is therefore imperative that banks, credit unions and other financial institutions (FIs) modernize their payments infrastructures for a quicker, cheaper payments experience. It cannot be overstated how integral non-cash payments are to the global economy, with the United States processing more than 174.2 consumer purchases made with cash.

What reports indicate so far is that the eCommerce giant is developing technology that will allow consumers to link their card data/Amazon Pay mobile wallet to their palm print alongside payment terminals that will be able to scan that palm print and allow them to make purchases without ever having to pull out a card or phone.

For many consumers, perks are a key driver of their creditcard choice, whether it’s airline miles, cash-back or points that can be redeemed for a variety of items. These perks have been an advantage for creditcards, but could that erode as, say, Alipay offers integrated loyalty programs?

Customers are also looking for options like digital and card-not-present (CNP) transactions that allow them to make eCommerce purchases as smoothly and seamlessly as possible. . These safety and convenience considerations are pushing more consumers to use — and more merchants to enable — contactless and CNP payments. percent of U.S.

Farnsworth, in a Variety interview, noted that the firm continues to have a $300 million equity line of credit, which is more than enough to keep the firm afloat while it hits reset. CreditCard’s Profit Squeeze. The balances on creditcards have grown at a fast pace — up 7 percent year over year in the early part of 2017.

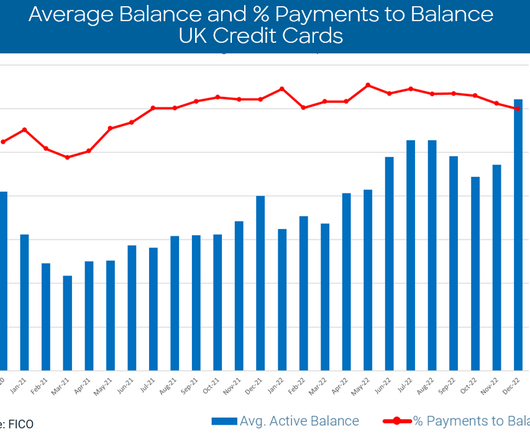

But this year’s rise seems to also have been driven by inflation, pushing the amount of average creditcard spend in the UK to the highest level since our UK Risk Benchmarking records began in 2006. This rise occurred in a month when UK retail sales volumes were widely reported as being down relative to past years.

Using creditcards (aka spending the bank’s money instead of your own) seemed so cool — until it suddenly wasn’t nearly as cool anymore. consumers to shift as much as $100 billion in annual spending from credit to debit cards.”. This trend is significant — one financial services company expects U.S. My Money, My Way.

don’t rely on swiping or chip card readers. cards use chip-and-signature and chip-and-PIN methods. Cardissuers have been slow to release contactless cards due to limited acceptance at the point of sale. JPMorgan Chase will roll out new Visa-branded contactless EMV cards this year. However, the U.S.

ATM cards, Febreze and the FICO score were all around for a while languishing in relative obscurity until something happened to push them into mass consciousness. until a little over five years ago, when digital innovators and startups began developing the form as an alternative to store cards or consumers.

European Card Fraud in 2021: Winners, Losers and Scams. The United Kingdom and the Nordic region continue to lead Europe in terms of digital transformation and fraud loss reduction - but non-card scams are rising fast. Only four countries of the 18 we studied improved their card fraud performance in 2021. Darcy Sullivan.

This means that for online purchases we’re more likely to see authentication requests, and to meet the requirements this authentication must come from two different categories from the below: For card transactions, the onus to manage this authentication doesn’t lie with the merchant, the merchant acquirer or the card scheme.

Since the first plastic creditcard was issued by American Express in 1959 , payment tech progress has been growing exponentially. EMV chip card technology had a good two decades or so, beginning in the mid-’90s. Most modern card readers and payment terminals are NFC-equipped.

According to a study by Aite Group , most student loan tuition payments are made via electronic check (ACH), followed by debit cards, which are favored by millennials and Gen Yers everywhere. In Q3 2019, creditcardissuer JCB International Co., The writing is on the whiteboard: School’s out for paper payments.

Long before American Express was a creditcardissuer and a closed loop payments network, it was in the business of moving mail (and other things) quickly from one coast to the other. And it’s that push toward forward evolution that leads to this week’s big news — American Express has acquired InAuth, Inc.

Payments provider Elan Financial Services announced that along with Ondot Systems , the leading provider of mobile-based card services, they have enhanced the My Mobile Money app so that it now offers two-way fraud alerts for Elan processed debit cards.

If the new FCA persistent debt rules come into effect, the way issuers communicate with customers will determine how successful they are and could affect customer risk and retention. From July 2018 issuers will need to prompt their cardholders if their expenditure surpasses pre-defined thresholds. Options for Contacting Customers.

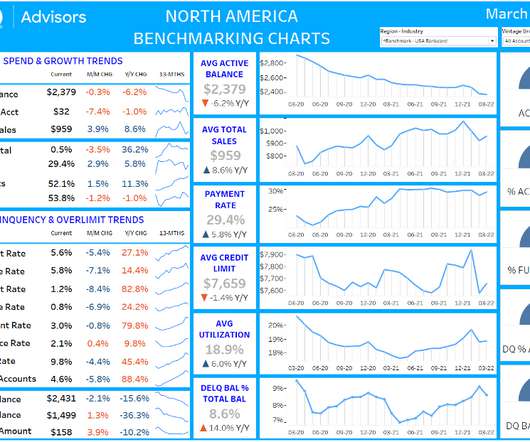

The following creditcard performance figures represent a national sample of approximately 130 million accounts that comprise FICO® Advisors’ Risk Benchmarking solution. Unemployment rate is typically a key factor used in creditcard loss forecasting models due to its high correlation with delinquency and loss.

The creditcard companies have been cutting off their noses to spite their faces, it seems. But the creditcard companies are now crying foul as they begin to see the negative effects of aggressive loyalty strategies on their bottom lines. The big issue with that is everybody’s trying to push their rewards programs.”.

While the anticipation for Amazon’s plunge into banking gets louder each year, it’s important to first understand Amazon’s existing strategy in financial services — what Amazon has launched and built, where the company is investing, and what recent products tell us about Amazon’s future ambitions. Amazon Payments.

American Express is introducing a suite of new commercial card products targeted at startups and entrepreneurs in a move that is aimed at competing with industry newcomers like Brex, Bloomberg reports said on Thursday (Oct. “It’s a new data source and a new lens on underwriting,” Marrs told the publication.

FICO monitors the UK credit market using data reported by the UK’s leading creditcardissuers through its FICO® Benchmark Reporting Service. Our UK Credit Report for August 2020 provides a clear picture of the ongoing impact of COVID-19 on consumer finances. Spend on UK cards continues to increase.

Friendly fraud has been on the rise for years, with customers contacting their banks to falsely assert that their creditcards have been used online for unauthorized purchases. Undeserved chargebacks are no trivial issue, either, as the number of such false claims rose 41 percent between 2016 and 2018. Why Customers Go Bad.

As businesses and consumers become more comfortable using creditcards online, the proportion of US commerce that takes place online has steadily increased over the last 20 years. Virtual card issuance. Business lending and corporate cards. Supporting merchant partner growth. Growing the internet economy.

The big challenge for credit providers right now is understanding the true level of financial difficulty consumers are facing because of the support being provided by furlough and payment holidays. Cash usage on cards has also increased month on month. Spend on UK Cards Increases Marginally. Average spend is now only 2.9

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content