This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Customers of DBS and POSB experienced difficulties accessing mobilebanking services on Monday (2 June). Reports indicated slowness when users attempted to log into the DBS digibank mobile app. In an update issued at 4:01pm, DBS Bank acknowledged the issue and said it was working to restore services.

This Friday, March 28, 2025, marks the end of an era for DBS Bank as Piyush Gupta steps down after an extraordinary 16-year tenure as Chief Executive Officer. During his tenure, he turned DBS from a traditional lender into a globally recognised powerhouse of digital banking. His leadership has been nothing short of transformative.

Data protection is a top priority in banking and payment systems, where sensitive information such as cardholder details and personal data are frequently exchanged. Ideal for secure communications, such as internet banking or email encryption. Example algorithm: RSA (Rivest-Shamir-Adleman).

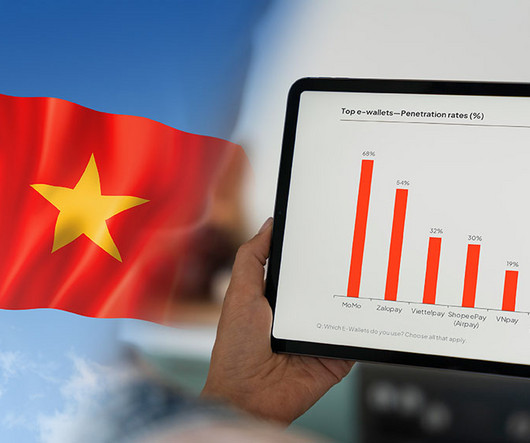

Vietnam’s digital finance landscape is undergoing a notable shift as new players emerge, established ones fade, and traditional banks rise to prominence, a new report by Decision Lab shows. However, by Q4 2023, Moca had slipped out of the top rankings, replaced by mobile apps from traditional banks.

per cent Central Bank of Armenia (CBA) Armenia’s growth has been driven in part by its young, tech-savvy population. Through its regulatory sandbox, the Central Bank of Armenia (CBA) has attracted $90million in investments, propelling the country to 34th place in the Global Fintech Index 2023. per cent holding a credit card.

Are digital first banks in Asia poised to lead a disruptive charge against well-entrenched, established commercial banks? In the traditional banking sphere globally, but especially true in Asia, there is a considerable proportion of unbanked and underbanked populations who lack complete or any access to banking services.

The plastic card, by necessity, is giving way to digital cards, and mobile apps are bringing card-not-present transactions, increasingly, to mobile devices. She noted that mobile app use is up double-digit percentages as of April, when the pandemic shifted so much of everyday life online.

Confronted by shifting factors such as tech advancements, generative AI, high interest rates, increased institutional oversight, and evolving customer expectations — the best banks must adapt their business and operating models in 2024, including in Asia. CHINA #1 China Merchants Bank China Merchants Bank Co.,

The Australian Securities and Investments Commission (ASIC), the country’s financial regulator, has filed documents against HSBC Bank Australia as it alleges the bank failed to adequately protect customers from being scammed out of millions of dollars. “All banks need to pull their weight in the fight against scams.

The travel and expense management space has earned a place as a top adopter of mobile solutions for the enterprise. But new data says other aspects of corporate finance are quickly joining the mobile solution bandwagon.

Tap to Everything There are six billion mobile devices in the world providing consumers with a versatile NFC enabled device primed to be ‘tapped’ At the end of 2023, Visa’s tap-to-pay penetration reached 65 per cent globally, up two times the penetration we saw in 2019, cementing tap as one of the best commerce experiences today.

Last week, wireless carrier T-Mobile announced it would throw its hat into the mobilebanking arena with the national rollout of T-Mobile MONEY. The mobile app offers low or no-fee checking-like services, out-of-network ATM usage fees and the ability to earn 4 percent APY on balances of up to $3,000. In fact, 72.4

As the financial services space focuses on digitizing offerings for their small business customers, much of these efforts are targeting onlinebanking portals accessed via desktop. One of the biggest impacts of mobile-based services will be the shift from weekly or monthly processes to operating in real time. .

Make that leather wallet a mobile one, wielded on smartphones. As we noted in this space earlier in the summer, using apps to bank is markedly being embraced by the younger generation. As spotlighted in the Digital Banking Tracker , the global digital banking market is slated to grow by 16 percent, compounded annually.

To roll out an alternative international money transfer offering called Co-opRemit, the Co-operative Bank of Kenya has teamed with international payment provider Thunes , according to an announcement. “We Co-operative Bank of Kenya works with 8.8 Co-operative Bank of Kenya works with 8.8

In today’s top news in digital-first banking, FIS is working with Quontic Bank on the Bitcoin Rewards Checking Account, while Aeldra has chosen i2c Inc. to power its digital private banking offerings. FIS Powers Launch Of Quontic Bank’s Bitcoin Rewards Account. Aeldra Taps i2c To Enable Global Banking Services.

He brings over 30 years experience in financial services with senior roles across global banking, private equity and accounting. He also joins the board of Quantum as director of fintech and banking, helping with its plan to list on the London Stock Exchange in 2026. Radford previously held the CEO role at Revolut UK from 2020 to 2023.

This week’s reveal: prior to March 2020, I had never used the mobile deposit feature of the banking app on my phone. Second, after I figured out how to use mobile deposit the first time, I asked myself, “Why did I ever go to the bank? Mobile deposits are so easy!”. Mobile deposits are so easy!”.

Quality Engineering is transforming digital banking, enabling seamless innovation, operational continuity, and future-proofing in a rapidly evolving landscape. The global banking industry is currently undergoing widespread change from a regulatory and technology perspective. These large-scale projects are inherently risky.

Banks are not just competing for customer engagement and retention — they are also vying for funding and resources as they overhaul their infrastructure and banking tools. The latest Digital Banking Tracker examines how legacy institutions stay competitive with challenger banks. Competition Can Lead to Innovation.

In today’s top digital-first banking news, German neobank N26 has hired a new chief financial officer (CFO) as it eyes a future initial public offering (IPO), while FinTech app Goalsetter has raised $3.9 The mobilebanking program also allows for peer-to-peer (P2P) transactions and money transfers. million in a seed round.

Not a mobile payment, Venmo or Zelle, PayPal or Cashbot was in sight. Seeing the flutter of sawbucks gave me a flashback to one of my first payments memories, from the early 1980s, when the Connecticut Bank and Trust Co. Mobile Payments Proliferate. It’s no secret that consumers are moving quickly to embrace mobile payments.

Traditionally, consumers stuck with familiar banks, but there’s now a growing trend of current account switching. The service was introduced as part of a government initiative to increase competition in the banking sector, aiming to reduce the inertia that had kept 75% of account holders with the same bank for years.

Payments giant Mastercard has launched its new ‘Open Banking for Account Opening’ programme for select US debit and prepaid products, hoping to streamline and secure account opening. In a recent study, Insider Intelligence found that Gen Z mobilebanking adoption continues to rise by 12.4 million in 2020 to 47.8

Today Mastercard announced the Open Banking for Account Opening program, providing a foundational set of open banking products as a core benefit to Mastercard consumer and small business debit issuers as well as consumer prepaid issuers in the U.S. year over year, from 20.7 million in 2020 to hit 47.8 million by 2026.

Traditional banking products, including checking, credit, and savings accounts, are under threat from a new crop of digital-first startups. Many of these startups are launching products without a bank charter and targeting a very specific customer base. DOWNLOAD THE 61-PAGE consumer banking REPORT. savings accounts.

Everyone knows that digital and mobile services are key to success in the 2020s — not only in terms of more revenue, but also larger transformations. It’s not that banks don’t want to go more digital and mobile, he said. But such shifts must happen, lest those banks get left behind. Gen Z is growing up.

It’s not fair, said FI.SPAN CEO and Co-Founder Lisa Shields, that Bill.com and AvidXchange get to have all the business payments fun — and there’s no reason why banks shouldn’t get to participate. Banks don’t ask for APIs, said Shields. It becomes a technological project for both the bank and for the customer.

trillion in total assets, JPMorgan Chase is the largest bank in the US. Its retail bank, Chase, spans 61 million American households. Led by Chairman and CEO Jamie Dimon, the bank is undergoing a transformation, moving away from offline legacy systems and into the digital age. Live briefing: Consumer Banks in The Digital Age.

The Fed''s latest mobilebanking/payments usage numbers ( full text ) were bouncing around the fintech blogosphere last week. Note: The online survey was fielded in December of each year. The only sour note was the flatline of mobilebanking usage among smartphone owners. Why has smartphone mobilebanking stalled?

Netbank – US$344 million (Series A, Philippines) Filipino banking-as-a-service (BaaS) provider Netbank secured the largest funding round in Southeast Asia (excluding Singapore) last year, raising in May 2023 a US$344 million Series A funding round, data from KPMG and Pitchbook show. Soft Space – US$31.5

Accounts combining high-interest rates, no fees, and advanced online solutions are available. Equipped with knowledge of the accounts and a thorough assessment of the internal requirements, getting set up is as simple as visiting a branch or going online.

Specifically, who knows what dangers — for banks, at least — lurk in shadow banking, as FinTechs emerge to nibble at market share? In the United States, there’s a bit of concentration here, as 29 percent of shadow banking is tied to the country, at $15 trillion in assets. Who knows what dangers lurk in the shadows?

New research from Economist Impact supported by Temenos finds that European banks are fighting back against competition from platform players, neobanks and payment providers. European banks are also migrating core banking systems to public cloud and SaaS in greater numbers than their counterparts in other regions.

New players on the digital banking scene are hoping to change the game by looking to industries that are categorically unlike banks for inspiration. Over the past few years, dozens of so-called digital-only “challenger” banks have emerged on the financial scene, ready to compete with larger more traditional banks.

A new report from FIS finds small businesses continue to feel fed-up with their big banks, despite a rebound in large bank loan approval rates for SME borrowers. The research, published last week, found that there are more aspects to small business banking than borrowing money that are frustrating SME customers.

In today’s top payments news, the People’s Bank of China has filed more than 80 patents as it attempts to adopt a digital currency, and Fiserv introduced Scan to Pay, a new way for diners to pay their checks with Apple Pay. The People’s Bank of China (PBOC) has filed over 80 patents as it attempts to take the renmibi to the digital stage.

The ongoing migration to mobile provides financial institutions a chance to reboot their approach to delivering information digitally. Digital banking v1.0 desktop onlinebanking) was primarily about porting paper-based statements into an online format. Digital banking v2.0 It’s a good long-term move.

Without the local branch to visit, financial institution (FI) customers were suddenly thrust into the world of digital and onlinebanking. As it has in so many other ways, the pandemic continues to force entities like banks and CUs to entirely rethink their product and service strategy. ” The Next Generation Of Onboarding.

Netbank – US$344 million (Series A, Philippines) Filipino banking-as-a-service (BaaS) provider Netbank secured the largest funding round in Southeast Asia (excluding Singapore) last year, raising in May 2023 a US$344 million Series A funding round, data from KPMG and Pitchbook show. Soft Space – US$31.5

8) the launch of Credit Sense, a solution that enables financial institutions to integrate credit scores into digital banking. According to Fiserv, with Credit Sense a person’s credit score can be displayed within the online or mobilebanking user interface alongside their account information.

Consumers demand easy, digital banking, but this pressure for banks to deliver is also coming from corporate clients. Take mobilebanking, which has propelled the introduction of mobile-only banks to meet demand for better services on smaller screens.

With more consumers moving to mobile transactions over visits to branches, some banks are considering closing brick-and-mortar locations to reduce operational costs. The price of real estate is prompting even the largest players in the banking world to scale back their branch operations. Can banks have it both ways?

If Amazon can get you lower-debt payments or give you a bank account, you’ll buy more stuff on Amazon.”. Based on our findings, it’s hard to claim that Amazon is building the next-generation bank. In aggregate, these product development and investment decisions reveal that Amazon isn’t building a traditional bank that serves everyone.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content